Nickel is a versatile metal critical for the clean energy revolution, especially in electric vehicle (EV) batteries. Its role in enhancing battery energy density and efficiency makes it indispensable for longer-range EVs.

As global demand for nickel surges, driven by electrification and renewable energy needs, it becomes a focal point for investors seeking growth opportunities.

With EV adoption accelerating, nickel demand is set to soar. According to Benchmark Mineral Intelligence, over 50% of nickel demand growth by 2030 will come from battery production, requiring an estimated 1.5 million metric tons annually.

The global shift toward high-energy-density batteries further cements nickel’s role. Additionally, global investment in nickel mining and refining infrastructure could surpass $66 billion by 2030, ensuring long-term supply stability.

For investors, the opportunity is immense. As automakers and governments prioritize EV adoption, demand for nickel could outpace supply, driving prices higher. Companies leading the charge in sustainable nickel production are well-positioned to capitalize on this growth, making them attractive investment options in 2025 and beyond.

However, investing in nickel stocks comes with its challenges. The mining industry is highly cyclical, with stock prices often fluctuating alongside nickel’s market value. Geopolitical events have further strained global nickel supplies and added volatility to the market. To mitigate risks, diversifying with a basket of nickel stocks could be a smart strategy.

With this in mind, here are four nickel companies to watch in 2025, known for their strategic importance and potential in the global nickel market:

Vale S.A.: A Nickel Powerhouse Driving the Energy Transition

Vale is a global leader in nickel production, playing a crucial role in enabling the transition to a low-carbon economy. With a US$38.52 billion market cap, the company accounts for 6%-7% of the global nickel supply. This makes the nickel company a critical supplier of electric vehicle (EV) batteries and renewable energy technologies.

In 2024, Vale produced 179,000 metric tons of nickel, with operations spanning Brazil, Canada, and Indonesia. The company has invested heavily in sustainable mining practices, including its flagship Voisey’s Bay and Sudbury operations in Canada.

Voisey’s Bay alone could add 45,000 metric tons of nickel annually once its underground expansion is completed in 2025.

- SEE MORE: Vale Base Metals Boosts Nickel: Completes Underground Mining of Voisey’s Bay Project in Canada

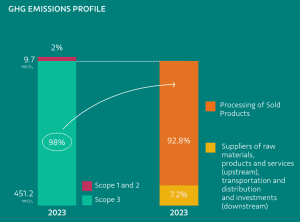

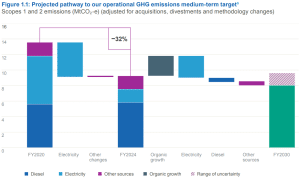

Vale is also at the forefront of decarbonization. Its revolutionary Onça Puma ferronickel operation in Brazil integrates energy efficiency measures that reduce CO₂ emissions. The chart below shows the nickel company’s GHG emissions profile.

In Indonesia, Vale partners with local entities to develop high-pressure acid leach (HPAL) facilities to meet the growing demand for high-grade Class 1 nickel.

With EV adoption expected to skyrocket, Vale is aggressively expanding its nickel refining capacity. The company has partnered with automakers, including Tesla, to secure long-term nickel supply agreements.

Vale’s low-carbon nickel production technology, certified for reducing greenhouse gas emissions by up to 90% compared to traditional methods, is a key selling point for environmentally conscious investors.

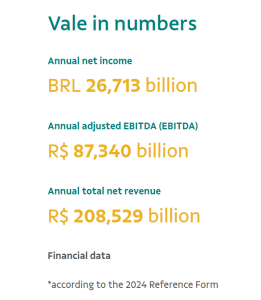

Here’s the company’s recent financial performance:

Looking ahead, Vale plans to invest over $3 billion to modernize its nickel operations and further reduce carbon emissions. With a clear focus on nickel’s role in EVs, renewable energy, and advanced technologies, the nickel miner continues to attract investors seeking exposure to the green energy revolution.

Norilsk Nickel: The World’s Largest Nickel Producer Driving Sustainability and Innovation

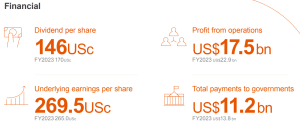

Norilsk Nickel or Nornickel, the world’s largest producer of refined nickel with a US$19.39 billion market cap, is a powerhouse in the global metals market. Headquartered in Russia, the company accounts for over 20% of global high-grade nickel production and operates key assets on the Taimyr and Kola Peninsulas.

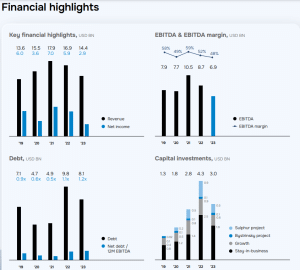

With its commitment to innovation and sustainability, Nornickel is central to the transition toward greener technologies like EVs. Below is the company’s most recent financial highlights:

In 2024 (9 months), Nornickel produced approximately 146,210 metric tons of nickel, maintaining its status as a reliable supplier for the EV battery industry. The company’s focus on sustainable mining practices includes its pioneering carbon-neutral nickel production program, launched to support global decarbonization goals.

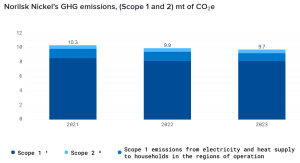

Nornickel has pledged to reduce its greenhouse gas emissions by 25% by 2030, making it an attractive choice for ESG-focused investors. The nickel company’s GHG emissions have decreased since 2021.

The key to Nornickel’s success is technological innovation. The company is advancing the use of artificial intelligence and automation across its operations, improving efficiency and minimizing environmental impact.

Notably, its Bystrinsky Mining and Processing Plant is recognized as one of the world’s most advanced facilities, producing nickel, copper, and other critical materials essential for EVs.

To ensure long-term supply stability, the mining giant is investing in exploration and modernization. The company plans to invest $8 billion by 2030 to upgrade its facilities and boost production of high-purity nickel, a key component of EV batteries. This includes expanding its Arctic operations, which hold vast untapped reserves of Class 1 nickel.

By securing long-term partnerships with global automakers and battery manufacturers, Nornickel is well-positioned to capitalize on the EV boom. Its commitment to sustainability, cutting-edge technologies, and robust supply chain solutions make it a top choice for investors looking to ride the wave of electrification.

BHP Group: A Global Leader in Sustainable Nickel Supply for EV Growth

BHP is one of the world’s largest mining companies and is diversifying its portfolio to include more nickel production. The company’s Nickel West operation, located in Western Australia, is a fully integrated business covering mining, smelting, and refining. This operation focuses on producing high-quality nickel products designed specifically for the EV battery supply chain.

The mining giant has invested around $3 billion since 2020 to develop a green nickel hub. However, as of mid-2024, BHP has paused its ambitions for this hub due to market challenges.

The company’s recent financial achievements are as follows, with a $126.29 billion market cap:

In 2024, BHP’s Nickel West produced over 80,000 metric tons of nickel, with 85% of this output directed toward EV battery manufacturers. The operation’s commitment to sustainability is evident in its low-carbon production processes, supported by investments in renewable energy.

For instance, BHP recently announced a 50% reduction in greenhouse gas emissions at Nickel West by 2030, aligning with its broader decarbonization goals.

BHP is also ramping up its exploration efforts to secure future nickel resources through various initiatives. This includes its West Musgrave Project which it integrates into its portfolio following the acquisition of OZ Minerals in May 2023. This project is in the early stages of execution and is expected to significantly contribute to BHP’s nickel production upon completion.

The company is investing billions over the next five years to expand its nickel production capacity and modernize its operations. This includes developing the Venus nickel deposit and upgrading the Kalgoorlie Nickel Smelter and Kwinana Refinery. These efforts are aimed at meeting the surging demand for high-grade Class 1 nickel, essential for lithium-ion batteries.

Partnerships play a significant role in BHP’s strategy. The company has secured long-term agreements with major automakers like Tesla and Toyota to supply sustainable nickel for EV batteries. These partnerships enhance its position as a key player in the global EV supply chain, offering investors a solid growth trajectory.

With its focus on operational excellence, environmental sustainability, and strategic partnerships, BHP is poised to remain a leader in the nickel market, driving the transition to a low-carbon future and delivering value for shareholders.

Alaska Energy Metals Corp.: A Rising Star in the Nickel Revolution

Alaska Energy Metals Corp. or AEMC is a standout junior nickel miner based in Alaska with approximately CAD$23.87 million market cap, focused on the development of high-grade nickel resources in a low-carbon environment. It’s strategically positioning itself to meet the surging demand for nickel in electric vehicle (EV) batteries and renewable energy markets.

The company’s flagship Nikolai Project, located in Southcentral Alaska, spans over 10,600 hectares of prospective land rich in nickel, copper, cobalt, and platinum group metals. Preliminary exploration results indicate a robust resource potential, with nickel grades rivaling some of the world’s top deposits.

AEMC is actively advancing exploration and development efforts, aiming to become a reliable source of Class 1 nickel, which is critical for high-energy-density batteries. The nickel junior has adopted a strong commitment to sustainability and environmental stewardship. The company plans to integrate renewable energy solutions into its operations to minimize its carbon footprint.

- RELATED: Alaska Energy Metals Cheers Trump’s Game-Changing Executive Order for Alaska’s Resource Future

Additionally, the rising nickel player is working closely with local communities and stakeholders to ensure responsible resource development that benefits the region economically and socially.

What sets AEMC apart is its strategic vision to fill the growing gap in the nickel supply chain, particularly in North America. By leveraging Alaska’s vast mineral wealth and a favorable regulatory environment, AEMC aims to become a key player in reducing reliance on foreign nickel imports.

As the EV market continues to grow—expected to exceed 50 million units annually by 2030, per Benchmark Mineral Intelligence—AEMC’s focus on sustainable nickel production positions it as an attractive opportunity for investors seeking exposure to the green metals revolution.

With its world-class resources, commitment to sustainability, and strategic location, AEMC could play a pivotal role in powering the next wave of electrification.

So, Why These Nickel Players?

Investing in top nickel companies provides a unique opportunity to participate in the energy transition. These firms are leading the way in supplying the critical metal essential for EV batteries and renewable energy technologies.

With demand and production forecasted to grow globally and massive infrastructure investments underway, the nickel market is primed for growth.

The top nickel companies highlighted—Vale, Norilsk Nickel, BHP, and Alaska Energy Metals Corp.—each bring distinct advantages, from vast reserves to sustainability-focused operations. These attributes position them as key players in meeting global nickel demand.

As EV adoption accelerates and nickel remains indispensable, these firms represent not just stability but growth potential, making them must-watch investments in the nickel boom.

- FURTHER READING: Nickel: The Metal Driving the Electric Vehicle Revolution

The post Top 4 Nickel Companies Driving Electrification and Clean Energy in 2025 appeared first on Carbon Credits.

Carbon Footprint

Climate Impact Partners Unveils High-Quality Carbon Credits from Sabah Rainforest in Malaysia

The voluntary carbon market is changing. Buyers are no longer focused only on large volumes of cheap credits. Instead, they want projects with strong science, long-term monitoring, and clear proof that carbon has truly been removed from the atmosphere. That shift is drawing more attention to high-integrity, nature-based projects.

One project now gaining that spotlight is the Sabah INFAPRO rainforest rehabilitation project in Malaysia. Climate Impact Partners announced that the project is now issuing verified carbon removal credits, opening access to one of the highest-quality nature-based removals currently available in the global market.

Restoring One of the World’s Richest Rainforest Ecosystems

The project is located in Sabah, Malaysia, on the island of Borneo. This region is home to tropical dipterocarp rainforest, one of the richest forest ecosystems on Earth. These forests store huge amounts of carbon and support extraordinary biodiversity. Some dipterocarp trees can grow up to 70 meters tall, creating habitat for orangutans, pygmy elephants, gibbons, sun bears, and the critically endangered Sumatran rhino.

However, the forest within the INFAPRO project area was not intact. In the 1980s, selective logging removed many of the most valuable tree species, especially large dipterocarps. That caused serious ecological damage. Once the key mother trees were gone, natural regeneration became much harder. Young seedlings also had to compete with dense vines and shrubs, which slowed the forest’s recovery.

To repair that damage, the INFAPRO project was launched in the Ulu-Segama forestry management unit in eastern Sabah.

- The project has restored more than 25,000 hectares of logged-over rainforest.

- It was developed by Face the Future in cooperation with Yayasan Sabah, while Climate Impact Partners has supported the project and helped bring its credits to market.

Why Sabah’s Carbon Removals are Attracting Attention

What makes Sabah INFAPRO different is not only the size of the restoration effort. It is also the way the project measured carbon gains.

Many forest carbon projects issue credits in annual vintages based on year-by-year growth estimates. Sabah INFAPRO followed a different path. It used a landscape-scale monitoring system and waited until the forest moved through its strongest natural growth period before issuing removal credits.

- This approach gives the credits more weight. Rather than relying mainly on short-term annual estimates, the project measured carbon sequestration over a longer period. That helps show that the forest delivered real, sustained, and measurable carbon removal.

The scientific backing is also unusually strong. Since 2007, the project has maintained nearly 400 permanent monitoring plots. These plots have allowed researchers, independent auditors, and technical specialists to observe the full growth cycle of dipterocarp forest recovery. The result is a large body of field data that supports carbon calculations and strengthens confidence in the credits.

In simple terms, buyers are not just being asked to trust a model. They are being shown years of direct forest monitoring across the project landscape.

Strong Ratings Support Market Confidence

Independent assessment has also lifted the project’s profile. BeZero awarded Sabah INFAPRO an A.pre overall rating and an AA score for permanence. That places the project among the highest-rated Improved Forest Management, or IFM, projects in the world.

The rating reflects several important strengths. First, the project has very low exposure to reversal risk. Second, it has a long and stable operating history. Third, its measured carbon gains align well with peer-reviewed ecological research and independent analysis.

These points matter in today’s market. Buyers have become more cautious after years of debate over the quality of some forest carbon credits. As a result, they now look more closely at durability, transparency, and third-party validation. Sabah INFAPRO’s rating helps answer those concerns and makes the project more attractive to companies looking for credible carbon removal.

The project is also registered with Verra’s Verified Carbon Standard under the name INFAPRO Rehabilitation of Logged-over Dipterocarp Forest in Sabah, Malaysia. That adds another level of market recognition and verification.

A Wider Model for Rainforest Recovery

Sabah INFAPRO also shows why high-quality nature-based projects are about more than carbon alone. The restoration effort supports broader ecological recovery in one of the world’s most important rainforest regions.

Climate Impact Partners said it has worked with project partners to restore degraded areas, run local training programs, carry out monthly forest patrols, and distribute seedlings to support rainforest recovery beyond the project boundary. These efforts help strengthen the wider landscape and expand the project’s environmental impact.

That broader value is becoming more important for buyers. Companies increasingly want projects that support biodiversity, ecosystem health, and local engagement, along with carbon removal. Sabah INFAPRO offers that mix, making it a stronger fit for the market’s shift toward higher-integrity credits.

The post Climate Impact Partners Unveils High-Quality Carbon Credits from Sabah Rainforest in Malaysia appeared first on Carbon Credits.

Bitcoin’s recent drop below $70,000 reflects more than short-term market pressure. It signals a deeper shift. The world’s largest cryptocurrency is becoming increasingly tied to global energy markets.

For years, Bitcoin has moved mainly on investor sentiment, adoption trends, and regulation. Today, another force is shaping its direction: the cost of energy.

As oil prices rise and electricity markets tighten, Bitcoin is starting to behave less like a tech asset and more like an energy-dependent system. This shift is changing how investors, analysts, and policymakers understand crypto.

A Global Power Consumer: Inside Bitcoin’s Energy Use

Bitcoin depends on mining, a process that uses powerful computers to verify transactions. These machines run continuously and consume large amounts of electricity.

Data from the U.S. Energy Information Administration shows Bitcoin mining used between 67 and 240 terawatt-hours (TWh) of electricity in 2023, with a midpoint estimate of about 120 TWh.

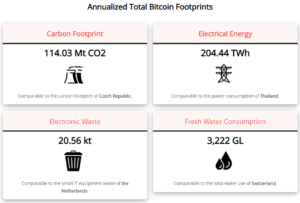

Other estimates place consumption closer to 170 TWh per year in 2025. This accounts for roughly 0.5% of global electricity demand. Recently, as of February 2026, estimates see Bitcoin’s energy use reaching over 200 TWh per year.

That level of energy use is significant. Global electricity demand reached about 27,400 TWh in 2023. Bitcoin’s share may seem small, but it is comparable to the power use of mid-sized countries.

The network also requires steady power. Estimates suggest it draws around 10 gigawatts continuously, similar to several large power plants operating at full capacity. This constant demand makes energy costs central to Bitcoin’s economics.

When Oil Rises, Bitcoin Falls

Bitcoin mining is highly sensitive to electricity prices. Energy is the highest operating cost for miners. When power becomes more expensive, profit margins shrink.

Recent market movements show this link clearly. As oil prices rise and inflation concerns persist, energy costs have increased. At the same time, Bitcoin prices have weakened, falling below the $70,000 level.

This is not a coincidence. Studies show a direct relationship between Bitcoin prices, mining activity, and electricity use. When Bitcoin prices rise, more miners join the network, increasing energy demand. When energy costs rise, less efficient miners may shut down, reducing activity and adding selling pressure.

This creates a feedback loop between crypto and energy markets. Bitcoin is no longer driven only by demand and speculation. It is now influenced by the same forces that affect oil, gas, and power prices.

Cleaner Energy Use Is Growing, but Fossil Fuels Still Matter

Bitcoin’s environmental impact depends on its energy mix. This mix is improving, but it remains uneven.

A 2025 study from the Cambridge Centre for Alternative Finance found that 52.4% of Bitcoin mining now uses sustainable energy. This includes both renewable sources (42.6%) and nuclear power (9.8%). The share has risen significantly from about 37.6% in 2022.

Despite this progress, fossil fuels still account for a large portion of mining energy. Natural gas alone makes up about 38.2%, while coal continues to contribute a smaller share.

This reliance on fossil fuels keeps emissions high. Current estimates suggest Bitcoin produces more than 114 million tons of carbon dioxide each year. That puts it in line with emissions from some industrial sectors.

The shift toward cleaner energy is real, but it is not complete. The pace of change will play a key role in how Bitcoin fits into global climate goals.

Bitcoin’s Climate Debate Intensifies

Bitcoin’s growing energy demand has placed it at the center of ESG discussions. Its impact is often measured through three key areas:

- Total electricity use, which rivals that of entire countries.

- Carbon emissions are estimated at over 100 million tons of CO₂ annually.

- Energy intensity, with a single transaction using large amounts of power.

At the same time, the industry is evolving. Mining companies are adopting more efficient hardware and exploring new energy sources. Some operations use excess renewable power or capture waste energy, such as flare gas from oil fields.

These efforts show progress, but they do not fully address the concerns. The gap between Bitcoin’s energy use and its environmental impact remains a key issue for investors and regulators.

- MUST READ: Bitcoin Price Hits All-Time High Above $126K: ETFs, Market Drivers, and the Future of Digital Gold

Bitcoin Is Becoming Part of the Energy System

Bitcoin mining is now closely integrated with the broader energy system. Operators often choose locations based on access to cheap or excess electricity. This includes areas with strong renewable generation or underused energy resources.

This integration creates both opportunities and challenges. On one hand, mining can support energy systems by using power that might otherwise go to waste. It can also provide flexible demand that helps stabilize grids.

On the other hand, it can increase pressure on local electricity supplies and extend the use of fossil fuels if cleaner options are not available.

In the United States, Bitcoin mining could account for up to 2.3% of total electricity demand in certain scenarios. This highlights how quickly the sector is scaling and how closely it is tied to national energy systems.

Energy Markets Are Now Key to Bitcoin’s Future

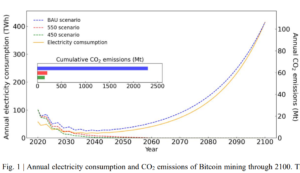

Looking ahead, the connection between Bitcoin and energy is expected to grow stronger. The network’s computing power, or hash rate, continues to reach new highs, which typically leads to higher energy use.

Electricity will remain the main cost for miners. This means Bitcoin will continue to respond to changes in energy prices and supply conditions. At the same time, governments are starting to pay closer attention to crypto’s environmental impact, which could shape future regulations.

Some forecasts suggest Bitcoin’s energy use could rise sharply if adoption increases, potentially reaching up to 400 TWh in extreme scenarios. However, cleaner energy systems could reduce the carbon impact over time.

Bitcoin is no longer just a financial asset. It is also a large-scale energy consumer and a growing part of the global power system.

As a result, understanding Bitcoin now requires a broader view. Energy prices, electricity markets, and carbon trends are becoming just as important as market demand and investor sentiment.

The message is clear. As energy markets move, Bitcoin is likely to move with them.

The post Bitcoin Falls as Energy Prices Rise: Why Crypto Is Now an Energy Market Story appeared first on Carbon Credits.

The post LEGO’s Virginia Factory Goes Big on Solar as Net-Zero Push Speeds Up appeared first on Carbon Credits.

-

Greenhouse Gases7 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Climate Change7 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Renewable Energy5 months ago

Renewable Energy5 months agoSending Progressive Philanthropist George Soros to Prison?