In breaking news, the Saskatchewan government announced its successful court injunction to stop the Canada Revenue Agency from collecting the federal carbon tax in the province. This came as a joy for the Saskatchewan residents, amid all the tax burden they were carrying these years.

Court Halts Federal Collection Amidst Heated Constitutional Dispute

Releases from Global News stated that Bronwyn Eyre, the Satkatchewan provincial justice minister, and attorney general declared just a day before that,

“The court ruled in our favor, blocking the federal government from unconstitutionally garnishing money, pending the full hearing and determination of the continuation of the injunction by the Federal Court.”

She further argued that garnishing a provincial bank account violates Section 126 of Canada’s constitution. The issue is pressed for a full court hearing. Dustin Duncan, the minister of Saskatchewan’s Crown Corporations said that the application was successful. He said,

“The court has ruled in our favor and has blocked the federal government from – in our view – unconstitutionally garnishing money from the province of Saskatchewan. The injunction will be in effect pending a full hearing.”

He expressed hope that they would be in court this week to argue the merits of the successive steps. He was also confident of winning.

In defense, Minister of National Revenue Marie-Claude Bibeau said that the Canada Revenue Agency is actively collecting taxes as required by law. She emphasized their strong commitment to following the law. Bibeau pointed out that Saskatchewan did not comply, even though the Supreme Court of Canada said the carbon tax was okay. She affirmed that their goal is to treat everyone fairly and equally and to encourage environmental responsibility across Canada.

However, the legal tussle ended with Saskatchewan winning the battle against the federal carbon tax. Following this, the provincial government announced its successful court injunction to stop the Canada Revenue Agency (CRA) from collecting the federal carbon tax within the province.

In April, the CRA announced plans to audit Saskatchewan for not paying the carbon levies. Prime Minister Justin Trudeau defended the exemption for home heating oil users, citing its higher cost compared to natural gas. He wished Premier Moe “good luck” for this stance on CRA. Trudeau has further ruled out extending similar exemptions to other fuel users.

Saskatchewan Faced Increased Energy Costs in 2023

Last year, came heavy on Saskatchewan residents and businesses. They saw increases in their power and energy bills, as well as at the gas pumps. In 2022, the federal government approved Saskatchewan’s output-based performance standards (OBPS) for industrial emitters. This saved the industry an estimated $3.7 billion in federal carbon taxes by 2030 compared to federal carbon pricing.

As reported by top media agencies, the federal carbon tax also increased from $50 to $65 per tonne, with plans to reach $170 per tonne by 2030. In April 2023 the federal fuel charge raised gasoline costs to $0.14/litre. This carbon pricing system raised their bills.

SaskPower president & CEO Rupen Pandya remarked in a news release on December 9, 2023,

“We are striving to achieve these goals while keeping rates as low as possible while complying with a federal regulatory framework that requires us to collect additional carbon tax revenue.”

Thus, we can see that all the turmoil began a year back… It escalated when Scott Moe, premier of Saskatchewan opposed the federal decision to exempt home heating oil from the carbon tax in Atlantic Canada. He downrightly called it unfair. He demanded a similar exemption for natural gas in Saskatchewan, but Ottawa refused. That time Bronwyn Eyre also warned that the federal government has threatened to remove these rebates, impose fines, or even press charges against Saskatchewan officials. Consequently, residents continued to receive carbon rebate checks.

Significantly, the independent rate review panel in Saskatchewan suggested that the provincial government should postpone planned increases in rates for 2023-2024 and 2024-2025. They recommended keeping SaskEnergy’s 31% increase in gas prices from August and an 8% rise in delivery fees for the year. The provincial government is currently reviewing the panel’s report carefully. The carbon tax scenario, however, transformed this year and for the betterment of the Canadian province.

source: Government of Saskatchewan (www.saskatchewan.ca)

source: Government of Saskatchewan (www.saskatchewan.ca)

Saskatchewan Families Enjoy Relief from Carbon Tax in 2024

Starting January 1, 2024, SaskEnergy and SaskPower removed the federal carbon tax from home heating. This decision can save ~98% of Saskatchewan families who were previously excluded from the federal exemption on home heating oil.

Dustin Duncan once again expressed himself by saying,

“We ensured fairness by removing the federal carbon tax on natural gas and electric heat, similar to what the federal government did for heating oil in Atlantic Canada,” said Crown Investments Corporation Minister. By extending this relief, we helped Saskatchewan families afford to heat their homes this winter.”

The removal of the carbon tax from SaskEnergy bills saved the average family about $400 in 2024. Heating accounted for ~60% of power consumption in winter for electric heat users. So SaskPower reduced the carbon tax rate on bills by 60%. This reduction lowered power bills by an average of $21 monthly for around 30,000 customers.

In January, customers still saw a federal carbon tax charge for natural gas or electricity used in December. However, bills for usage from January 1, 2024, onward showed the tax as both a charge and a reversal credit, effectively making it zero. This was a huge win for Saskatchewan, paving the way for carbon tax revocation.

The post Saskatchewan Achieves Legal Win Over Canada’s Federal Carbon Tax appeared first on Carbon Credits.

Africa’s carbon markets are growing fast. Governments, companies, and global institutions are paying more attention to the continent’s carbon credit potential. Estimates from a renewable energy company’s research arm, Axina Group, show Africa’s carbon market could reach $100 billion by 2030 and grow even more over time.

This growth depends on strong policies and good market systems. Countries that control how carbon credits are made, verified, and sold—called sovereign carbon markets—can capture more value. This also helps them reach climate goals.

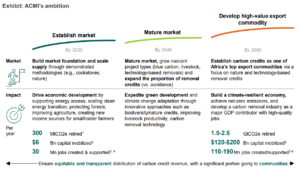

The Africa Carbon Markets Initiative (ACMI) sets a clear roadmap. It aims to produce 300 million carbon credits per year by 2030, growing to 1.5 billion credits per year by 2050. This could make Africa one of the world’s largest carbon credit producers.

Global organizations, including the World Bank, support this view. They point to Africa’s natural resources and improving policies as key reasons for growth.

Africa’s Green Gold: Forests, Wetlands, and Carbon Sinks

Africa has huge natural carbon sinks. These include tropical forests, wetlands, and grasslands. They absorb carbon dioxide from the air, which forms the basis for carbon credits.

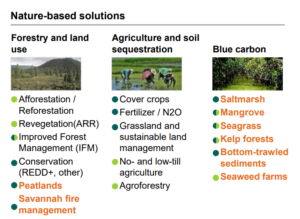

Tropical forests alone absorb 1.1–1.5 billion tonnes of CO₂ each year. Millions of hectares of land can also be restored. Projects like reforestation and improved land use create carbon credits. They also improve soil, water, and biodiversity, and provide jobs for local communities.

Nature-based solutions are expected to play a big role. Globally, they could deliver up to one-third of the emissions reductions needed by 2030. Africa has a large share of this opportunity. But today, the continent still produces a small part of global carbon credits, indicating there is room for strong growth.

Several companies and platforms are shaping Africa’s carbon market by developing projects and linking them to buyers. For example, Africa Carbon Partners develops large nature‑based projects that protect forests and generate verified credits across West and Central Africa.

Moreover, ZeroCarbon Africa connects smallholder farmers to global carbon markets with real‑time tracking and fair pricing. Meanwhile, Climera uses blockchain technology to increase transparency in carbon credit issuance and tracking.

Other regional platforms like SB Power Africa and PanAfricaCarbon offer project development and trading services. In addition, global certification bodies like Verra support many African projects by certifying carbon credits under established standards.

From Voluntary Markets to Sovereign Systems

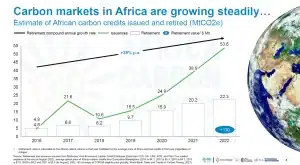

Most African carbon projects now operate in voluntary carbon markets (VCMs). Companies buy credits to offset emissions they cannot eliminate. But Africa accounts for only 9–11% of retired carbon credits in recent years.

Sovereign carbon market systems can change this, with governments taking a central role. They set rules, approve projects, and manage sales. This improves transparency and ensures projects meet national climate goals, also called Nationally Determined Contributions (NDCs) under the Paris Agreement.

Countries such as Kenya, Nigeria, and Gabon are already building national carbon strategies. These strategies aim to capture more value locally. Projects often include rules that share revenue with governments and communities. This can fund local services, climate projects, and economic development.

The AFRICA RISING 2026 report by Axina Group projects specific national revenue from carbon-related assets using sovereign systems. For example:

- Ghana could generate $1.8 billion annually by 2030

- Nigeria could capture over $400 million annually

- Tanzania could reach over $120 million annually

- Mozambique and Uganda also show potential for substantial carbon-linked revenue

These figures illustrate how sovereign systems can keep capital on the continent while encouraging local reinvestment and community benefits.

$100B Carbon Opportunity and Millions of Jobs

Carbon markets are expanding worldwide. The global carbon market reached about $949 billion in 2023. Voluntary carbon markets alone could grow to $10–40 billion by 2030. Carbon removal markets could reach $100 billion per year by 2030–2035, driven by industries like technology, finance, and aviation.

Africa’s projected $100 billion market by 2030 would make it one of the fastest-growing regions. High-quality carbon credits are in demand as companies try to reach net-zero emissions.

Carbon markets can also create many jobs. The ACMI estimates 30 million jobs by 2030, rising to over 110 million by 2050. Jobs include forest restoration, renewable energy projects, land management, and monitoring.

More notably, carbon finance can attract private investment. Many African countries have funding gaps for climate projects. Carbon markets offer a way to bring in private capital.

Revenue from carbon credits can also support communities. At $50 per tonne, nature-based projects could generate $15 billion annually. At $100 per tonne, this could rise to $57 billion. These projects create millions of jobs while helping the environment.

By integrating sovereign systems, individual countries can capture larger shares of these revenues. The AFRICA RISING 2026 report highlights that, with proper frameworks, countries like Ghana, Nigeria, and Tanzania could earn hundreds of millions to billions annually from carbon assets. This shows the economic value of combining policy, technology, and natural resources.

How Africa Could Lead Globally

Africa has a unique advantage. It has large carbon sinks and relatively low historical emissions compared to developed regions. This means it can grow carbon projects while still meeting climate targets.

If ACMI and country-level strategies succeed, Africa could become a major global supplier of carbon credits. Companies worldwide will need these credits to meet net-zero goals.

Nature-based carbon projects also deliver co-benefits. They improve soil, water, and biodiversity. They support rural livelihoods and local economies. This makes carbon markets a climate and development tool at the same time.

Trust, Fairness, and the Rules of the Game

However, challenges remain. Market integrity is key: Buyers need to trust that credits represent real, permanent emissions reductions.

There are concerns about fairness. Critics warn of “carbon colonialism,” where wealthy countries benefit more than local communities. Policies must ensure communities get a fair share of revenue.

Also, policy gaps exist. Many countries lack clear rules for carbon markets, which can scare investors. Infrastructure and technical tools, such as land management systems and data monitoring, are still developing. Carbon prices vary depending on project type and quality, adding uncertainty.

To succeed, African governments need strong laws, clear policies, and transparent systems. Partnerships with international organizations can build technical expertise. Monitoring, reporting, and verification (MRV) systems are crucial to ensure credibility.

A Defining Decade Ahead for Africa’s Carbon Markets

Africa’s carbon market is at a turning point. The next ten years will shape how the sector grows and how much it benefits the economy and climate.

If plans succeed, Africa could produce hundreds of millions of carbon credits annually. This would support global climate goals, attract investment, create jobs, and drive sustainable development.

The market’s size depends on policy, pricing, and execution, but demand for carbon credits is rising. Africa has the natural resources to meet that demand. With the right systems, the continent can turn its carbon potential into a long-term economic and climate advantage.

The post Africa’s $100B Carbon Opportunity: How Sovereign Markets Could Lead the World appeared first on Carbon Credits.

The U.S. biofuel industry stepped into 2026 with strong policy backing and rising demand. However, global events quickly changed the tone. A sharp escalation in the US–Israel–Iran conflict in late February sent shockwaves through energy markets. Oil prices jumped, supply chains tightened, and uncertainty spread across fuel markets.

At the same time, the U.S. Environmental Protection Agency (EPA) introduced its most ambitious biofuel policy yet under the Renewable Fuel Standard (RFS). This created a powerful but complicated mix—long-term policy certainty collided with short-term geopolitical chaos.

As a result, the U.S. biofuel sector now faces a defining moment. Growth looks strong on paper, but rising costs and market volatility are testing how sustainable that growth really is.

EPA Administrator Lee Zeldin said:

“President Trump promised a Golden Age of American agriculture. Once again, his administration is delivering. Overall, ‘Set 2’ creates a larger, more stable, and more reliable domestic market for U.S. crops, strengthening farm income and rural economies.

For 20 years, this program has diversified our nation’s energy supply and advanced American energy independence. EPA is proud to deliver on this mission and to do so at historic levels.”

EPA’s RFS ‘Set 2’ Rule Changes the Game

Amid this volatility, U.S. policy took a decisive turn. On March 26, 2026, the EPA finalized the Renewable Fuel Standard (RFS) “Set 2” rule, setting new blending targets for 2026 and 2027.

- The new requirements are the highest in the program’s history. The EPA set total renewable volume obligations at 26.81 billion RINs for 2026 and 27.02 billion RINs for 2027.

These targets reflect a major increase compared to previous years and signal a strong push toward domestic biofuel production.

- The policy focuses heavily on expanding the use of biomass-based diesel, including biodiesel and renewable diesel. This includes a 70 percent reallocation of small refinery exemptions granted for 2023–2025

- At the same time, ethanol blending levels remain stable at 15 billion gallons annually, providing consistency for corn producers.

Additionally, the rule puts back 70% of the biofuel volumes that small refineries didn’t have to blend from 2023 to 2025. This effectively increases the burden on refiners while ensuring that biofuel demand remains strong.

Policy Pivot Favors U.S. Biofuel Producers

Beyond volume targets, the EPA introduced structural changes. The agency removed renewable electricity from the RFS program, narrowing its focus to liquid and gaseous fuels. It also introduced measures to limit the role of foreign feedstocks in the future.

Starting in 2028, imported biofuels will receive a lower compliance value compared to domestic products. In addition, incentives such as the 45Z tax credit are designed to favor U.S.-based production.

The broader goal is clear. The policy aims to strengthen energy independence, support farmers, and reduce reliance on foreign oil. Estimates suggest that these measures could cut oil imports by hundreds of thousands of barrels per day over the next two years.

At the same time, the EPA expects significant economic benefits. The rule could generate billions of dollars for rural economies and create thousands of new jobs across agriculture and manufacturing sectors.

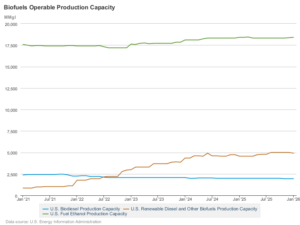

The U.S. Energy Information Administration (EIA) recently published updated data on the country’s biofuel production capacity, shown below.

Demand Surges but Supply Faces Pressure

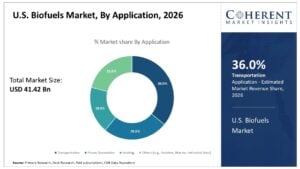

While policy is driving demand higher, supply conditions remain tight. The U.S. biofuel market is projected to exceed $41 billion in 2026, supported by transportation demand and decarbonization goals.

Ethanol continues to dominate the market, especially through E10 fuel blends. However, advanced biofuels such as renewable diesel and SAF are growing faster due to stronger policy incentives and rising interest in low-carbon fuels.

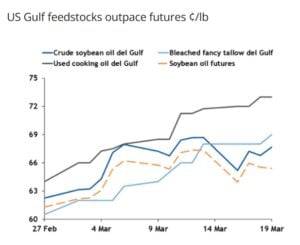

Despite this growth, feedstock availability is becoming a major concern. Domestic sources such as soybean oil, used cooking oil, and tallow are under pressure. Prices have risen sharply due to limited supply and increased competition from both the fuel and food industries.

At the same time, import restrictions have reduced access to cheaper global feedstocks. Tariffs and lower compliance values for foreign inputs are shifting the market toward domestic sourcing. While this supports local producers, it also reduces flexibility during supply shortages.

New processing capacity is helping to ease some of the pressure. Agribusiness companies are expanding oilseed crushing operations, and renewable diesel plants are increasing output. However, these efforts may take time to fully balance supply and demand.

War-Driven Oil Shock Makes Biofuels More Valuable

The U.S. biofuel market is gaining momentum as rising oil prices and global conflict reshape energy choices. The ongoing U.S.-Israel-Iran war has disrupted key oil infrastructure and shipping lanes near the Strait of Hormuz, sending crude prices sharply higher.

As conventional fuels become more expensive, alternatives like ethanol, renewable diesel, and sustainable aviation fuel (SAF) are increasingly attractive, driving demand across the sector. This surge has pushed feedstock costs to multi-year highs, with soybean oil, used cooking oil, and animal fats climbing steadily.

At the same time, renewable fuel credits, or RINs, have reached levels not seen in years, boosting margins for biofuel producers but raising compliance costs for refiners. Reports from Argus Media show that U.S. renewable diesel feedstocks hit their highest prices in over two years this month, highlighting the market’s sensitivity to war-driven disruptions.

While industry groups argue that strong domestic production stabilizes supply and reduces reliance on imported oil, refiners warn that these rising costs could eventually reach consumers, especially in regions with less competition. The combination of strong demand, tight supply, and geopolitical risk is redefining U.S. biofuel market dynamics.

Opportunities for Farmers, Challenges for Refiners

The current landscape is creating both opportunities and challenges.

Biofuel producers and farmers are seeing strong benefits. Higher demand for crops like corn and soybeans is supporting agricultural incomes. Investment in renewable fuel projects is also increasing, driven by policy certainty and market growth.

However, refiners and fuel distributors are facing tighter margins. The cost of compliance, combined with volatile feedstock prices, is making operations more difficult. Smaller players may struggle to compete in this environment.

Consumers could also feel the impact through higher fuel prices, especially if cost pressures continue. To manage these risks, many companies are turning to hedging strategies. Storage, long-term contracts, and flexible sourcing are becoming essential tools in navigating market uncertainty.

Supporting this announcement, U.S. Secretary of Agriculture Brooke L. Rollins, said:

“Today’s announcement is truly historic for our nation’s farmers and energy producers. These numbers represent the highest levels of biofuels ever required to be blended into our fuel supply. With President Trump and Administrator Zeldin’s leadership, these historically high volumes are expected to create a $3 to $4 billion dollar increase in net farm income. The Renewable Fuel Standard Set 2 Rule will create a $31 billion dollar value for American corn and soybean oil for biofuel production in 2026, which is $2 billion more than in 2025. Our farmers are stepping up to grow American energy dominance.”

Strong Growth, But Uncertain Path

Looking ahead, the U.S. biofuel market is expected to grow steadily, with projections showing annual growth of up to 10% through the next decade. Strong EPA mandates and supportive policies will continue to drive demand.

However, the path forward is far from stable.

The mismatch between long-term policy goals and short-term geopolitical disruptions will remain a key challenge. Events like the ongoing Middle East conflict can quickly shift market dynamics, creating sudden price swings and supply risks.

The rest of 2026 will depend on several key factors, including potential EPA waivers, movements in RIN markets, and developments in global energy supply. In the end, the success of U.S. biofuels will depend on balance. Policy support provides a strong foundation, but flexibility will be critical in managing real-world challenges.

Despite the industry growing fast, the question remains—can it handle the pressure of both policy ambition and global uncertainty at the same time?

The post U.S. Biofuel Market 2026: Can EPA Policies Offset War-Driven Volatility? appeared first on Carbon Credits.

Carbon Footprint

TotalEnergies and Masdar’s $2.2 Billion Deal Signals a Big Push into Asia’s Renewable Energy Boom

Asia is entering a new energy era. Electricity demand is rising fast, and global energy giants are moving quickly to secure their position. A major $2.2 billion joint venture between TotalEnergies and Masdar reflects this shift. The deal is not just about building renewable assets. It is about capturing one of the biggest growth stories in global energy.

The simple reality is: Asia will drive most of the world’s electricity demand in the coming decade.

TotalEnergies and Masdar: A Power Partnership Built for Scale

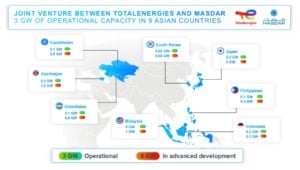

The new joint venture brings together the strengths of both companies under a single platform. It creates a 50:50 partnership that will manage onshore renewable energy assets across nine countries. These include Indonesia, Japan, South Korea, and several fast-growing markets in Southeast Asia and Central Asia.

The platform already holds 3 gigawatts (GW) of operational capacity. On top of that, it has a pipeline of 6 GW expected to come online by 2030. This combination gives the venture a strong starting point and a clear growth path.

More importantly, the focus goes beyond just building solar or wind farms. The joint venture plans to integrate solar, wind, and battery storage systems. This approach supports grid stability and ensures a reliable energy supply. As renewable energy expands, such integration becomes essential.

This is not a small regional project. It is a large, coordinated effort designed to meet rising demand while supporting cleaner energy systems.

His Excellency Dr Sultan Al Jaber, UAE Minister of Industry and Advanced Technology and Chairman of Masdar, noted:

“The UAE has established itself as a global energy leader by delivering at scale, investing with conviction, and building partnerships that endure. Masdar epitomizes that approach. We are proud to have pioneered renewable energy deployment in Central Asia and the Caucasus, and we have an expanding portfolio in some of the most attractive growth markets in Asia-Pacific. Asia will be the main driver of global electricity demand growth this decade, and this collaboration with TotalEnergies will accelerate our progress across the continent, unlocking new opportunities to deliver the competitive, reliable energy solutions that our partners and customers need.”

- READ MORE:

- TotalEnergies and Google’s 1 GW Solar Deal Signals a New Phase in the Data Center Energy Race

- TotalEnergies and AllianzGI Team Up on $580M Battery Storage Push in Germany

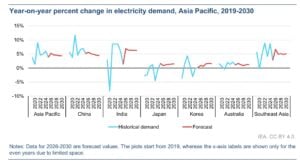

Asia’s Electricity Boom Is Reshaping Markets: Wood Mackenzie’s Analysis

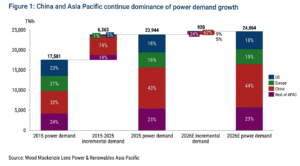

Asia has become the engine of global electricity demand. Over the past decade, the region accounted for nearly all new power demand compared to the United States and Europe.

In 2025, the scale reached a historic milestone. As per Wood Mac’s Asia Pacific Power & Renewables: What to look for in 2026 report, China alone generated over 10,000 terawatt-hours (TWh) of electricity. That was more than the combined output of the U.S. and Europe. At the same time, the rest of Asia continued to produce more electricity than either region year after year.

This growth is not random. It is driven by three powerful forces: rapid industrial expansion, urban population growth, and rising digital infrastructure.

Data centers are now a major driver. As artificial intelligence and cloud computing expand, electricity demand is rising sharply. Countries like Japan, China, and those in Southeast Asia are seeing new demand from this sector alone.

- For example, Japan could add up to 66 TWh of demand from data centers by 2034. China may need an extra 668 TWh by 2030. Southeast Asia will also see steady increases as digital services grow.

Even short-term slowdowns have not changed the bigger picture. In early 2025, trade tensions and tariffs slowed demand growth. China’s power demand growth dropped to 2.5% in the first quarter. India and Southeast Asia also saw weaker numbers.

However, the slowdown did not last long. By the third quarter, demand rebounded strongly. China recorded over 6% growth again. India and Southeast Asia also recovered, supported by industrial output and extreme heat driving cooling needs.

This resilience shows that Asia’s demand growth is not fragile. It is deeply rooted in economic and technological change.

Clean Energy Expansion Keeps Pace

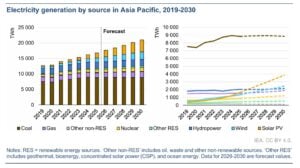

As demand rises, clean energy is expanding quickly across Asia. IEA predicts that by 2030, 56% of the world’s electricity use will be in the Asia Pacific, up from 53% in 2025.

In 2025 alone, the region added nearly 500 GW of wind and solar capacity. This shows strong momentum toward decarbonization.

Governments are also playing a key role. Many countries are introducing policies that allow renewable energy to reach consumers directly. These steps make clean power more accessible and encourage further investment.

However, challenges remain. Supply chain bottlenecks and trade barriers continue to create uncertainty. Equipment shortages, especially for gas turbines, could slow down parts of the energy transition. At the same time, global political shifts are affecting trade flows and investment decisions.

Despite these issues, the overall direction is clear. Clean energy is growing, and it is becoming central to Asia’s power systems.

Strategic Moves in a Competitive Market

The partnership between TotalEnergies and Masdar reflects a deeper strategy. Both companies are positioning themselves for long-term growth in high-demand markets.

For TotalEnergies, the deal supports its Integrated Power strategy. This approach combines renewable generation with flexible energy solutions and market access. It helps the company manage supply and demand more effectively.

For Masdar, the partnership strengthens its presence across Asia. It also brings the advantage of working with a global energy major. This combination improves its ability to scale projects and enter new markets.

Leadership also highlights the importance of this collaboration. Dr. Sultan Al Jaber, Chairman of Masdar, emphasized that Asia will drive global electricity demand growth. He also pointed out that partnerships like this will help deliver reliable and competitive energy solutions.

The choice of Abu Dhabi as the control hub adds another layer of significance. It shows how the UAE is expanding its role in global energy markets, especially in clean energy investments.

The Road Ahead: Demand, Data, and Decarbonization

Looking forward, Asia will remain the dominant force in global electricity demand. By 2026, the region is expected to account for about 85% of new power demand worldwide. This is a massive share, especially as the U.S. and Europe also increase their demand due to AI and data centers.

China will continue to lead in absolute terms. However, India and Southeast Asia will play equally important roles as growth engines. Together, they will shape the region’s energy future.

At the same time, the energy transition will face key questions:

- Can renewable energy keep up with rising demand?

- Will supply chain issues slow progress?

- How will countries balance growth with sustainability?

The answers will define the next phase of Asia’s energy story.

Thus, the $2.2 billion joint venture is a signal of where the energy world is heading. Companies are not just building power plants. They are building platforms that combine scale, technology, and market access.

Asia offers the biggest opportunity, but it also demands smart execution. Projects must be large, reliable, and integrated. They must support both growth and sustainability.

And this is why partnerships like the one between TotalEnergies and Masdar matter. They bring together capital, expertise, and long-term vision.

The post TotalEnergies and Masdar’s $2.2 Billion Deal Signals a Big Push into Asia’s Renewable Energy Boom appeared first on Carbon Credits.

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Renewable Energy6 months ago

Renewable Energy6 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits