In 2024, hydrogen emerged as a climate-friendly alternative to fuel as well as electricity. Promising projects sparked to life on both the production and consumption fronts. Despite Trump’s pro-oil stance, analysts are optimistic about hydrogen’s future in this new year- 2025.

According to BNEF, clean H2 supply is projected to increase 30X and could reach 16.4 million metric tons annually by 2030. This surge is mostly attributed to supportive policies and a flourishing project pipeline.

As we step into 2025, several crucial moments await the low-carbon, clean hydrogen sector. They could be a mix of challenges and opportunities. Analysts also predict an increase in the fructification of significant projects and financial investment decisions this year.

Wood Mackenzie recently released a report identifying some crucial developments in the hydrogen sector for 2025 that one needs to scrutinize. Let’s study it here.

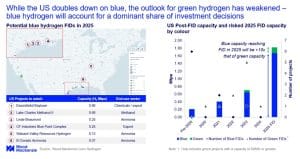

Blue Hydrogen to Dominate the U.S. Market in 2025

- In 2025, the U.S. hydrogen market will focus heavily on blue hydrogen, with over 1.5 million tons per annum (Mtpa) of capacity reaching the final investment decision (FID).

This marks a 10X increase compared to green hydrogen. The report revealed that at least three large-scale blue hydrogen projects are expected to mature this year. With this output, the U.S. has all the potential to become the world’s leading blue hydrogen producer.

Green Hydrogen to Face Strong Headwinds in 2025?

Conversely, green hydrogen projects are likely to face major challenges in 2025. FIDs for these projects are expected to fall short of expectations. This could be due to reduced government focus on clean energy under the Trump administration.

Green hydrogen could also face stiff competition for electricity resources from data centers. On top of that, lengthy delays in connecting projects to the grid can slow down the progress.

While some demand will come from companies working toward sustainability goals, short-term growth opportunities are expected to shrink. Many green hydrogen projects, especially those targeting transportation, and heavy industries like steel, and e-fuels, may be delayed or canceled altogether.

- MUST READ: Navigating the Green Hydrogen Hype: IRENA’s Take on the “Silver Bullet” vs. “Champagne” Strategies

Nonetheless, it will Shine Through the Storm…

If not in the U.S. green hydrogen will have its niche in emerging economies like South America, the Middle East, India, and China. Eventually, these economies can launch giga-scale projects in 2025. So how can these nations properly green hydrogen progress globally?

Well, these projects leverage cheap solar and wind power and government incentives that reduce costs and ensure financial viability. For instance, India’s Kakinada project utilizes existing ammonia infrastructure and enjoys government subsidies.

Meanwhile, Saudi Arabia’s Neom Helios project benefits from state-led support and a 30-year offtake agreement with Air Products. These factors add a bonus point to green hydrogen.

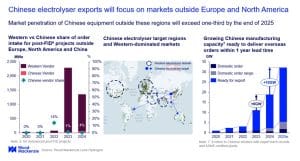

Emergence of Chinese Electrolyzers

Most importantly regions like Southeast Asia, the Middle East, and North Africa will benefit abundantly from low-cost renewable energy and affordable electrolyzers from Chinese manufacturers.

By 2025, China can supply at least one-third of orders outside North America and Europe. Competitive pricing, shorter delivery times, and strong manufacturing capacity give Chinese electrolyzers an edge. Moreover, China is also expanding its domestic manufacturing capacity and is most likely to add over 10 GW of capacity this year. This will further strengthen their global presence, especially in areas with fewer trade barriers.

However, entering Europe and North America is more challenging. Trade restrictions and regulatory hurdles, such as the European Union’s 25% content limit for Chinese-made electrolyzers, limit their opportunities. To overcome these challenges, some Chinese companies are localizing production through partnerships and technology licensing.

Green Hydrogen’s Stance in Europe and North America

While blue hydrogen dominates the U.S., green hydrogen is making headway in Europe and North America. The European Commission (EC) also launched a nearly €2 billion hydrogen auction as part of its broader €4.6 billion initiative to accelerate net-zero technologies. This marked a significant step in the EU’s push for renewable hydrogen.

In Germany, HydrogenPro partnered with J. Heinr. Kramer Group to develop green hydrogen projects ranging from 5 MW to 50 MW. They aim to advance green hydrogen projects in Germany, Austria, and the Benelux region. These projects will power industries and the grid, and fuel hydrogen-powered vehicles.

On October 30, 2024, Avina Clean Hydrogen announced its major green hydrogen project in Vernon, California, near the Port of Long Beach. The facility with a capacity of 4 metric tons of compressed green hydrogen daily can decarbonize heavy-duty transport and advance California’s clean energy goals.

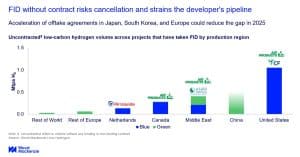

Uncontracted Hydrogen Supply to Persist in 2025

The Woodmack report emphasized another interesting scenario that would prevail in this year’s hydrogen economy. It says uncontracted low-carbon hydrogen capacity will remain a challenge due to difficulties in securing offtake agreements. This means out of the 5.5 Mtpa of low-carbon hydrogen projects that have reached FID, ~ 2.5 million tons of hydrogen remains without contracts.

The U.S. Treasury Simplifies Clean Hydrogen Tax Credit Rules

The U.S. Department of the Treasury and IRS released final rules for the section 45V Clean Hydrogen Production Tax Credit under the Inflation Reduction Act on January 3. These rules encourage clean hydrogen production from some nuclear power plants that are nearing retirement. The hydrogen will be used in fuel cells.

The new rules included some important changes and added flexibility for the clean hydrogen industry. These updates will propel projects ahead and ensure they comply with the emissions requirement laws to qualify for clean hydrogen.

Notably, they will also provide much-needed clarity, investment stability, and adaptability, especially for participants in the Department of Energy’s Regional Clean Hydrogen Hubs program.

The final rules clarify how hydrogen producers, using electricity from diverse sources, natural gas with carbon capture, renewable natural gas (RNG), or coal mine methane, can qualify for the tax credit.

Nuclear for Clean Hydrogen

As the fresh rules enable at-risk nuclear to produce clean hydrogen, it will subsequently boost nuclear energy demand in sectors like AI. S&P Global reported market optimism surged following the announcement, and energy companies saw significant gains.

For instance, Constellation Energy’s shares rose by 3.8%, closing at $251.74, while Vistra experienced a 7% jump, reaching $160.33. NextEra Energy and its renewable energy unit also saw increases of 1.2% and 3%, respectively. Plug Power recorded a 2.6% rise, closing at $2.39. These positive market movements were witnessed after Constellation announced a $1 billion contract to supply nuclear energy to 13 government agencies.

John Podesta, Senior Advisor to President Biden for International Climate Policy mentioned something very significant that sums up all for the U.S. green hydrogen future. He said,

“The extensive revisions we’ve made in this final rule provide the certainty that hydrogen producers need to keep their projects moving forward and make the United States a global leader in truly green hydrogen.”

The post Hydrogen in 2025: The Journey through Progress, Pitfalls, and Policy Shifts appeared first on Carbon Credits.

Carbon Footprint

Climate Impact Partners Unveils High-Quality Carbon Credits from Sabah Rainforest in Malaysia

The voluntary carbon market is changing. Buyers are no longer focused only on large volumes of cheap credits. Instead, they want projects with strong science, long-term monitoring, and clear proof that carbon has truly been removed from the atmosphere. That shift is drawing more attention to high-integrity, nature-based projects.

One project now gaining that spotlight is the Sabah INFAPRO rainforest rehabilitation project in Malaysia. Climate Impact Partners announced that the project is now issuing verified carbon removal credits, opening access to one of the highest-quality nature-based removals currently available in the global market.

Restoring One of the World’s Richest Rainforest Ecosystems

The project is located in Sabah, Malaysia, on the island of Borneo. This region is home to tropical dipterocarp rainforest, one of the richest forest ecosystems on Earth. These forests store huge amounts of carbon and support extraordinary biodiversity. Some dipterocarp trees can grow up to 70 meters tall, creating habitat for orangutans, pygmy elephants, gibbons, sun bears, and the critically endangered Sumatran rhino.

However, the forest within the INFAPRO project area was not intact. In the 1980s, selective logging removed many of the most valuable tree species, especially large dipterocarps. That caused serious ecological damage. Once the key mother trees were gone, natural regeneration became much harder. Young seedlings also had to compete with dense vines and shrubs, which slowed the forest’s recovery.

To repair that damage, the INFAPRO project was launched in the Ulu-Segama forestry management unit in eastern Sabah.

- The project has restored more than 25,000 hectares of logged-over rainforest.

- It was developed by Face the Future in cooperation with Yayasan Sabah, while Climate Impact Partners has supported the project and helped bring its credits to market.

Why Sabah’s Carbon Removals are Attracting Attention

What makes Sabah INFAPRO different is not only the size of the restoration effort. It is also the way the project measured carbon gains.

Many forest carbon projects issue credits in annual vintages based on year-by-year growth estimates. Sabah INFAPRO followed a different path. It used a landscape-scale monitoring system and waited until the forest moved through its strongest natural growth period before issuing removal credits.

- This approach gives the credits more weight. Rather than relying mainly on short-term annual estimates, the project measured carbon sequestration over a longer period. That helps show that the forest delivered real, sustained, and measurable carbon removal.

The scientific backing is also unusually strong. Since 2007, the project has maintained nearly 400 permanent monitoring plots. These plots have allowed researchers, independent auditors, and technical specialists to observe the full growth cycle of dipterocarp forest recovery. The result is a large body of field data that supports carbon calculations and strengthens confidence in the credits.

In simple terms, buyers are not just being asked to trust a model. They are being shown years of direct forest monitoring across the project landscape.

Strong Ratings Support Market Confidence

Independent assessment has also lifted the project’s profile. BeZero awarded Sabah INFAPRO an A.pre overall rating and an AA score for permanence. That places the project among the highest-rated Improved Forest Management, or IFM, projects in the world.

The rating reflects several important strengths. First, the project has very low exposure to reversal risk. Second, it has a long and stable operating history. Third, its measured carbon gains align well with peer-reviewed ecological research and independent analysis.

These points matter in today’s market. Buyers have become more cautious after years of debate over the quality of some forest carbon credits. As a result, they now look more closely at durability, transparency, and third-party validation. Sabah INFAPRO’s rating helps answer those concerns and makes the project more attractive to companies looking for credible carbon removal.

The project is also registered with Verra’s Verified Carbon Standard under the name INFAPRO Rehabilitation of Logged-over Dipterocarp Forest in Sabah, Malaysia. That adds another level of market recognition and verification.

A Wider Model for Rainforest Recovery

Sabah INFAPRO also shows why high-quality nature-based projects are about more than carbon alone. The restoration effort supports broader ecological recovery in one of the world’s most important rainforest regions.

Climate Impact Partners said it has worked with project partners to restore degraded areas, run local training programs, carry out monthly forest patrols, and distribute seedlings to support rainforest recovery beyond the project boundary. These efforts help strengthen the wider landscape and expand the project’s environmental impact.

That broader value is becoming more important for buyers. Companies increasingly want projects that support biodiversity, ecosystem health, and local engagement, along with carbon removal. Sabah INFAPRO offers that mix, making it a stronger fit for the market’s shift toward higher-integrity credits.

The post Climate Impact Partners Unveils High-Quality Carbon Credits from Sabah Rainforest in Malaysia appeared first on Carbon Credits.

Bitcoin’s recent drop below $70,000 reflects more than short-term market pressure. It signals a deeper shift. The world’s largest cryptocurrency is becoming increasingly tied to global energy markets.

For years, Bitcoin has moved mainly on investor sentiment, adoption trends, and regulation. Today, another force is shaping its direction: the cost of energy.

As oil prices rise and electricity markets tighten, Bitcoin is starting to behave less like a tech asset and more like an energy-dependent system. This shift is changing how investors, analysts, and policymakers understand crypto.

A Global Power Consumer: Inside Bitcoin’s Energy Use

Bitcoin depends on mining, a process that uses powerful computers to verify transactions. These machines run continuously and consume large amounts of electricity.

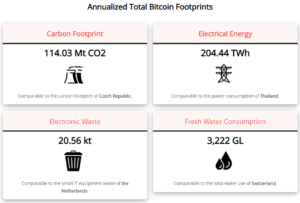

Data from the U.S. Energy Information Administration shows Bitcoin mining used between 67 and 240 terawatt-hours (TWh) of electricity in 2023, with a midpoint estimate of about 120 TWh.

Other estimates place consumption closer to 170 TWh per year in 2025. This accounts for roughly 0.5% of global electricity demand. Recently, as of February 2026, estimates see Bitcoin’s energy use reaching over 200 TWh per year.

That level of energy use is significant. Global electricity demand reached about 27,400 TWh in 2023. Bitcoin’s share may seem small, but it is comparable to the power use of mid-sized countries.

The network also requires steady power. Estimates suggest it draws around 10 gigawatts continuously, similar to several large power plants operating at full capacity. This constant demand makes energy costs central to Bitcoin’s economics.

When Oil Rises, Bitcoin Falls

Bitcoin mining is highly sensitive to electricity prices. Energy is the highest operating cost for miners. When power becomes more expensive, profit margins shrink.

Recent market movements show this link clearly. As oil prices rise and inflation concerns persist, energy costs have increased. At the same time, Bitcoin prices have weakened, falling below the $70,000 level.

This is not a coincidence. Studies show a direct relationship between Bitcoin prices, mining activity, and electricity use. When Bitcoin prices rise, more miners join the network, increasing energy demand. When energy costs rise, less efficient miners may shut down, reducing activity and adding selling pressure.

This creates a feedback loop between crypto and energy markets. Bitcoin is no longer driven only by demand and speculation. It is now influenced by the same forces that affect oil, gas, and power prices.

Cleaner Energy Use Is Growing, but Fossil Fuels Still Matter

Bitcoin’s environmental impact depends on its energy mix. This mix is improving, but it remains uneven.

A 2025 study from the Cambridge Centre for Alternative Finance found that 52.4% of Bitcoin mining now uses sustainable energy. This includes both renewable sources (42.6%) and nuclear power (9.8%). The share has risen significantly from about 37.6% in 2022.

Despite this progress, fossil fuels still account for a large portion of mining energy. Natural gas alone makes up about 38.2%, while coal continues to contribute a smaller share.

This reliance on fossil fuels keeps emissions high. Current estimates suggest Bitcoin produces more than 114 million tons of carbon dioxide each year. That puts it in line with emissions from some industrial sectors.

The shift toward cleaner energy is real, but it is not complete. The pace of change will play a key role in how Bitcoin fits into global climate goals.

Bitcoin’s Climate Debate Intensifies

Bitcoin’s growing energy demand has placed it at the center of ESG discussions. Its impact is often measured through three key areas:

- Total electricity use, which rivals that of entire countries.

- Carbon emissions are estimated at over 100 million tons of CO₂ annually.

- Energy intensity, with a single transaction using large amounts of power.

At the same time, the industry is evolving. Mining companies are adopting more efficient hardware and exploring new energy sources. Some operations use excess renewable power or capture waste energy, such as flare gas from oil fields.

These efforts show progress, but they do not fully address the concerns. The gap between Bitcoin’s energy use and its environmental impact remains a key issue for investors and regulators.

- MUST READ: Bitcoin Price Hits All-Time High Above $126K: ETFs, Market Drivers, and the Future of Digital Gold

Bitcoin Is Becoming Part of the Energy System

Bitcoin mining is now closely integrated with the broader energy system. Operators often choose locations based on access to cheap or excess electricity. This includes areas with strong renewable generation or underused energy resources.

This integration creates both opportunities and challenges. On one hand, mining can support energy systems by using power that might otherwise go to waste. It can also provide flexible demand that helps stabilize grids.

On the other hand, it can increase pressure on local electricity supplies and extend the use of fossil fuels if cleaner options are not available.

In the United States, Bitcoin mining could account for up to 2.3% of total electricity demand in certain scenarios. This highlights how quickly the sector is scaling and how closely it is tied to national energy systems.

Energy Markets Are Now Key to Bitcoin’s Future

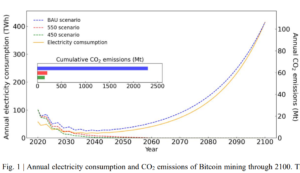

Looking ahead, the connection between Bitcoin and energy is expected to grow stronger. The network’s computing power, or hash rate, continues to reach new highs, which typically leads to higher energy use.

Electricity will remain the main cost for miners. This means Bitcoin will continue to respond to changes in energy prices and supply conditions. At the same time, governments are starting to pay closer attention to crypto’s environmental impact, which could shape future regulations.

Some forecasts suggest Bitcoin’s energy use could rise sharply if adoption increases, potentially reaching up to 400 TWh in extreme scenarios. However, cleaner energy systems could reduce the carbon impact over time.

Bitcoin is no longer just a financial asset. It is also a large-scale energy consumer and a growing part of the global power system.

As a result, understanding Bitcoin now requires a broader view. Energy prices, electricity markets, and carbon trends are becoming just as important as market demand and investor sentiment.

The message is clear. As energy markets move, Bitcoin is likely to move with them.

The post Bitcoin Falls as Energy Prices Rise: Why Crypto Is Now an Energy Market Story appeared first on Carbon Credits.

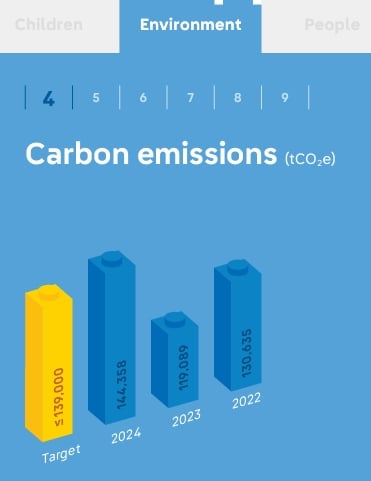

The post LEGO’s Virginia Factory Goes Big on Solar as Net-Zero Push Speeds Up appeared first on Carbon Credits.

-

Greenhouse Gases7 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Climate Change7 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Renewable Energy5 months ago

Renewable Energy5 months agoSending Progressive Philanthropist George Soros to Prison?