For the past two decades, low-level cloud cover has been declining, increasing the amount of sunlight absorbed by Earth and amplifying global warming.

As global temperatures have reached record highs in recent years, there has been concern that the decline in cloudiness may be enhancing warming more than previously expected.

In a new study, published in Atmospheric Chemistry and Physics Letters, we investigate how the decline in global cloudiness affects the Earth’s “energy imbalance” – the difference between absorbed solar energy and heat radiated into space that results in global warming.

This imbalance has more than doubled over the past 20 years, as greenhouse gases have trapped more heat in the atmosphere.

We find that, since 2003, the decrease of cloudiness has been responsible for half of the increase of Earth’s energy imbalance.

Analysing the drivers of global changes to cloud cover, we find that the decrease in cloudiness over the past two decades has been primarily driven by humans, rather than being caused by natural variations in Earth’s climate.

Taken together, our findings mean that scientists can even more confidently attribute recent warming to human activities.

Low-level clouds and warming

Low-level clouds are those that have a base below 6,500 feet (2,000 metres) above Earth and include stratus, stratocumulus and cumulus. They are typically found over large areas of the global ocean, where there is a large moisture supply from evaporation.

These clouds have a powerful impact on the Earth’s climate because they reflect a substantial fraction of incoming sunlight back into space.

By acting as the Earth’s “sunscreen”, they keep the climate cooler than it would otherwise be.

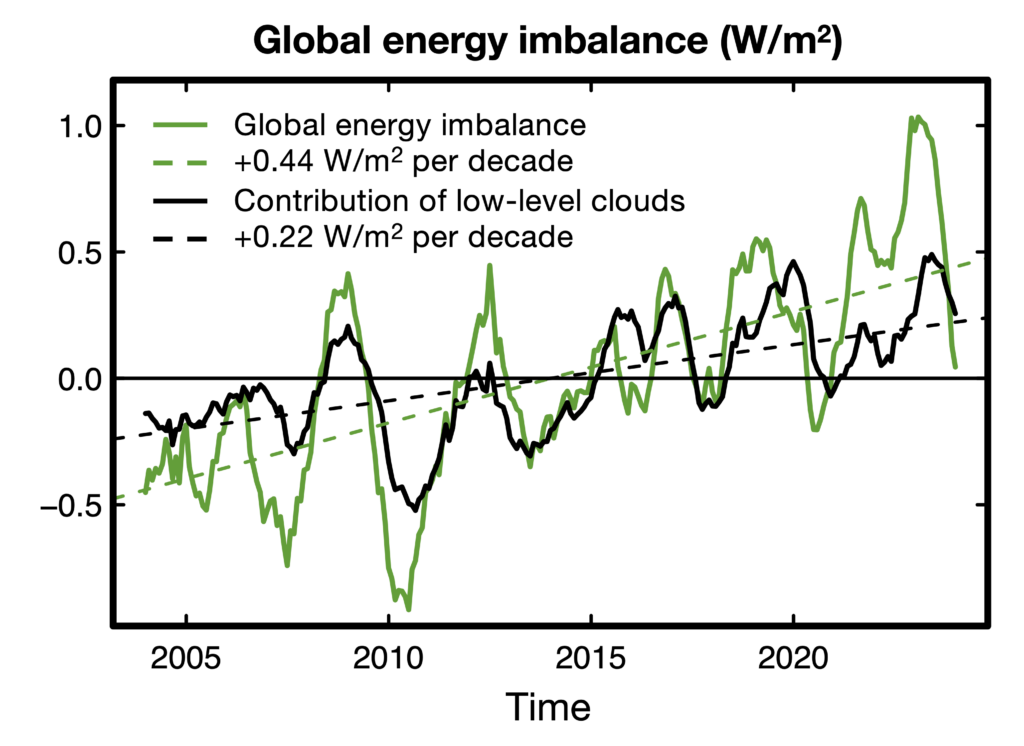

Satellite observations reveal a global decline in these low-level clouds since the turn of the millennium. This is shown in the chart below, where the black line represents the average percentage of the Earth covered by low-level clouds and the dashed line the downward trend.

Our research shows that the decline in cloudiness over the past 20 years has played a major role in increasing the Earth’s energy imbalance and, therefore, warming.

The Earth’s energy imbalance is the difference between the amount of energy arriving at the Earth from the sun and what is reflected and radiated back to space.

Rising greenhouse gas emissions from human activity are upsetting this balance by trapping more energy in the atmosphere, leading to warming.

A less cloudy atmosphere also helps supercharge the energy imbalance, because it means more sunlight reaches the Earth.

In our research, we use a simple model to assess how changes in low-level clouds between July 2003 and June 2024 contributed to the Earth’s energy imbalance.

We find that, averaged globally, changes in low-level cloudiness caused an extra 0.22 watts per metre squared (W/m2) per decade of absorbed sunlight. This amounts to exactly half of the concurrent increase in Earth’s energy imbalance over the same time period.

This is shown in the chart below, where the green line represents the increase in the Earth’s energy imbalance over 2003-24 and the black line shows the contribution of low-level clouds to that trend.

Why is cloudiness changing?

Scientists have attributed declining cloud cover in the 21st century to three main causes.

The first is a decrease in human-caused aerosol emissions over recent decades. Aerosols – tiny, light‑scattering particles produced mainly by burning fossil fuels – influence the formation of clouds, by acting as “seeds” for cloud droplets to form.

In recent years, aerosol emissions have been reduced due to efforts to clean up air pollution, such as cleaner shipping fuel regulations. Cleaner air has resulted in a decline in cloudiness.

Second, increasing concentration of greenhouse gases in the atmosphere has led to a warmer and drier atmosphere, which also helps to dissipate clouds.

Although a warmer atmosphere generally holds more water vapour in absolute terms, what matters for clouds is the “relative humidity” of the air, which has been declining in many places. This is a measure of how “saturated” the air is, or how much water vapour the air contains compared to the maximum it could hold.

Finally, cloud cover decreases have also been linked to ocean surface warming, which affects atmospheric humidity and, thus, cloudiness. Reduced cloudiness leads to more sunlight being absorbed at the ocean surface – and more warming. This amplifying loop is known as a “cloud feedback”.

However, the exact strength of these three effects on cloud cover is still unclear.

In fact, cloud feedbacks are among the main uncertainties in climate model projections of global warming.

Attributing low-cloud cover changes

In the next step of our study, we explore how the three human-caused factors mentioned above – aerosols, greenhouse gases and cloud feedback – contributed to recent low-level cloud changes.

We also look at the extent to which cloud changes could be explained by natural climate variability, which causes substantial year-to-year fluctuations in cloudiness and energy imbalance.

To do this, we use a statistical technique known as “cloud-controlling factor analysis”.

This analysis involves calculating the sensitivity of clouds to their “controlling factors”, including meteorological variables, such as temperature, humidity and winds, as well as aerosol concentrations.

To calculate how each factor contributed to the bigger picture of declining cloud cover, we combine sensitivity calculations with observed trends in meteorology and aerosol emissions.

This analysis allows us to attribute trends in cloud cover to known physical drivers: either natural climate variability, or human activities linked to aerosols, greenhouse gases and cloud feedback.

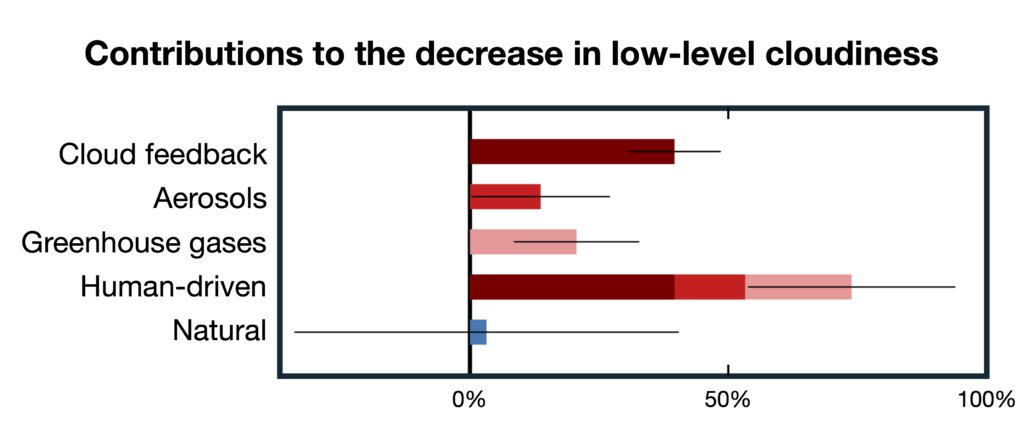

Our research finds that about 40% of the low-level cloud decrease since 2003 was driven by warming of the ocean surface – in other words, the cloud feedback process. This is followed by the effects of greenhouse gases (21%) and aerosols (14%).

Natural climate variability accounts for just 3% of the low-level cloud trend.

(The remaining 23% of the trend cannot be explained by our statistical method. This could be due to the limitations of cloud, temperature, humidity and aerosol concentration observations.)

The chart below shows how human-driven factors – the sum of aerosol effects (red), greenhouse gas emissions (pink) and cloud feedback (burgundy) – were responsible for almost three quarters of the decrease in low-level cloudiness over 2003-24. Natural climate variability (blue), on the other hand, played a minor role.

Thus, our analysis indicates that, at global scales, the observed cloud decrease is primarily driven by humans, rather than being caused by natural variations in Earth’s climate.

And, since low-level clouds contribute to half of the energy imbalance increase over the same period, it follows that a significant part of recent rises in energy imbalance can also be attributed to humans.

Clouds in climate models

So, should we be concerned that this cloudiness decrease means the Earth could see more warming than already anticipated?

To answer this, we looked at whether the climate models used by scientists to project future global warming accurately simulate recent declines in low-cloud cover.

While the models produce a wide range of outcomes, we found that, on average, the simulated changes in low-level cloudiness changes are in close agreement with real-world trends.

This is reassuring, as it means the effects of low-cloud cover are already accounted for in existing warming projections.

However, questions still remain around what is driving recent increases to the Earth’s energy imbalance, which have outpaced projections made by climate models.

Our findings rule out declines in low-level clouds as the reason that climate models have been underestimating the Earth’s energy imbalance, and, as a result, warming. But it is still possible that models are underrepresenting future global warming to some extent.

Low-level clouds are just one of several drivers of changes in energy imbalance. Future work will therefore need to assess other observed and simulated drivers of energy imbalance changes: for example, the impact of upper-level clouds, or changes in water vapour or sea ice.

Finally, it is important to stress that, while our findings are reassuring, they should certainly not make us complacent about the current global warming trend. The impacts of climate change are serious enough as they are – even if there is no evidence of a missing amplifying feedback in our projections.

The post Guest post: How declining cloudiness is accelerating global warming appeared first on Carbon Brief.

Guest post: How declining cloudiness is accelerating global warming

A Dutch startup thinks it has the answer to two of Europe’s biggest energy transition conundrums – long-duration storage batteries that are free from critical minerals and powered by rust.

In a pilot project in February, Amsterdam-based Ore Energy supplied four days of uninterrupted power to a research facility operated by France’s EDF electricity utility using a battery made of little more than iron pellets, water and air. That followed a grid installation in the Netherlands last year.

“These are the first instances of grid-connected iron-air batteries in Europe,” Yakup Koç, Ore Energy’s chief operating officer, told Climate Home News. “With these deployments, we’ve proven that the technology really works.”

Using abundant, cheap materials that can be sourced locally across Europe, iron-air batteries store and release electricity through a simple, chemical process: rusting and de-rusting.

“Rusting refers to discharging, and de-rusting refers to charging,” Koç said. “When discharging, air is drawn in and reacts with the iron, forming rust and releasing electricity in the process. To recharge, the oxygen is removed, and the rust reverts to iron, ready to go again.”

Energy transition’s “missing link”

Batteries able to store solar and wind power over longer periods of time than conventional lithium-ion batteries are often described as the “missing link” in the energy transition.

Technology such as Ore Energy’s could hold particular appeal for Europe as it strives to reduce its exposure to volatile critical mineral supply chains and boost its production of batteries for power storage and electric vehicles (EVs) instead of relying so heavily on imports from China.

“There are no critical raw materials in our batteries … which means we are truly independent of supply chain issues in that sense,” Koç said.

It also makes them cheaper than established batteries, which mostly use either lithium iron phosphate (LFP) or lithium nickel cobalt manganese oxide (NMC) chemistries.

“Critical raw materials are expensive,” Koç adds. “Because we’re using abundant resources, our cost price can be as much as 10 times lower than lithium.”

-

Battery passport plan aims to clean up the industry powering clean energy

Some of the world’s largest battery makers are piloting a scheme led by the Global Battery Alliance to reward manufacturers that meet social and environmental standards -

South African rare earths project aims to rival Chinese with low-cost model

The EU-backed Zandkopsdrift project plans to offset the high cost of rare earths production with another mineral in hot demand for use in batteries -

Self-taught mechanics give second life to Jordan’s glut of spent EV batteries

As EV sales boom in Jordan, a lack of formal infrastructure for dealing with end-of-life batteries is leading to some innovative solutions

Europe sprints for storage capacity

Wind and solar make up the fastest-growing energy sources globally, but bridging inherent supply fluctuations requires batteries capable of storing energy for far longer than currently possible with a typical lithium-ion battery.

Demand for battery energy storage systems has surged and it currently accounts for 15% of global battery demand, according to the International Energy Agency (IEA).

Multi-day storage capabilities will become increasingly important as renewable integration booms, said Zeenat Hameed, principal analyst for energy storage at Wood Mackenzie.

“Under net-zero scenarios, the average duration of newly installed storage assets may need to increase from around 2.5 hours today to roughly 20 hours to manage multi-day variability in wind and solar generation,” she told Climate Home News.

Europe added a record 27.1 GWh of new batteries in 2025, bringing total capacity to 77.3 GWh, according to a recent report by industry group SolarPower Europe, adding that capacity must increase 10-fold by 2030 to meet its needs.

With about 90% of battery-storage applications relying on Chinese lithium batteries, steps to diversify suppliers are also seen as vital to shore up energy security.

Innovation that can help reduce or diversify battery mineral supplies and demand – for example, technologies that do not require critical minerals – could play a key role in shoring up energy security, the IEA says.

Uncomplicated alternative?

This is where iron-air comes in.

Koç said Ore’s system can be configured to store energy anywhere between 24 and 100 hours, and is capable of being reused over a lifespan of as much as 20 years.

Each battery storage unit ships in standard 40-foot containers, a similar size as lithium-ion systems, and can be connected and operational within days of arriving on site.

Ore Energy is not the only company in the race to bring iron-air to the market.

US-based Form Energy, which has also developed an iron-air battery system, has partnered with Xcel Energy on a 10-megawatt (MW) iron-air system in Minnesota at a retiring coal plant. They have also announced plans to provide a 300-MW iron-air system to power a new Google data centre.

-

To break its coal habit, China should look to California’s progress on batteries

Big strides on battery storage are helping the state and other parts of the US cut their reliance on “peakers” – fossil fuel power plants that crank up at times of high demand -

China maximises battery recycling to shore up critical mineral supplies

Beijing is bracing for a tsunami of spent EV batteries by taking steps to boost recycling – a strategy that could also cut its reliance on imports of clean energy minerals -

Cobalt and nickel-free electric car batteries boom in “good news” for rainforests

Lithium iron phosphate batteries do not contain cobalt and nickel, which are mostly found in rainforest nations like the DR Congo and Indonesia

Beyond iron-air, a broader range of long-duration energy storage (LDES) technologies is taking shape. US-based Noon Energy is developing a carbon-oxygen battery based on solid-oxide fuel cell technology which it says avoids “scarce metals and minerals” and targets storage durations of 100 hours and above, while E-Zinc’s zinc-air systems are another player in the ultra-long-duration bracket.

Mahika Sri Krishna from the LDES Council, a global organisation focused on accelerating long duration energy storage solutions, told Climate Home News a mix of different technologies would be necessary to support grid reliability as renewables gain ground.

“Medium-duration storage solutions can help manage daily variability in renewable generation, while very long-duration systems may help address less frequent but more challenging reliability events,” said Sri Krishna, a senior manager for research and analysis at the group.

Last longer, scale up faster

Iron-air faces numerous challenges to scale-up and challenge established battery technologies, however, energy experts say.

Demand for multi-day storage is not yet high enough to drive commercialisation, Hameed said, estimating that lithium-ion is expected to retain about 85% of the global storage market through 2034 as economies of scale and manufacturing innovations reduce its costs.

While iron-air’s raw materials are cheap, the overall system cost still needs to prove itself at scale, Hameed added.

At Ore Energy, the next step is moving from single- to multi-container configurations, building what Koç describes as an “energy reservoir” that can be deployed across different use cases.

The scale-up itself, he said, is less the challenge than gaining industry acceptance by building a commercial track record.

“It’s not only about customers seeing the data and knowing it works,” he said. “The whole ecosystem around a new technology has to be brought along.”

When that happens, the technology could have transformative effects on Europe’s energy transition, he said.

“Europe will not decarbonise its power system on renewables alone,” Koç said. “Without long-duration storage, Europe risks replacing dependence on fossil fuels with dependence on overbuilding, curtailment and backup generation.”

The post Dutch startup’s rust-powered batteries could help crack Europe’s energy storage gap appeared first on Climate Home News.

Dutch startup’s rust-powered batteries could help crack Europe’s energy storage gap

The state is one of a handful where cancer diagnoses are on the rise.

Iowa is among a few states where cancer diagnoses are on the rise. A new analysis from the Harkin Institute for Public Policy & Citizen Engagement and the Iowa Environmental Council says that environmental exposures are partially to blame.

Iowa’s Cancer Crisis Linked to Pesticides, PFAS, Fertilizer and Radon, Report Says

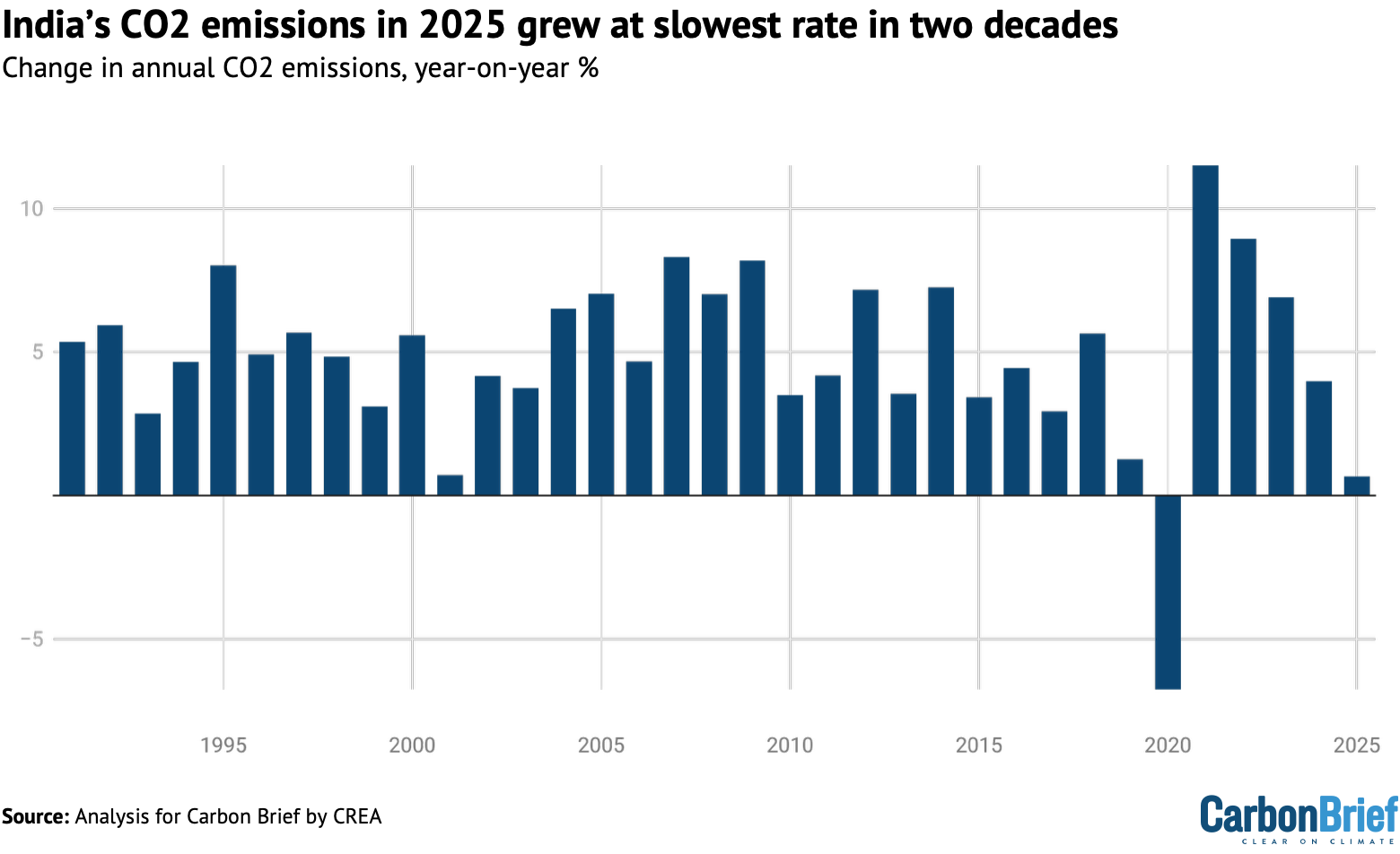

India’s carbon dioxide (CO2) emissions grew by 0.5% in the second half of 2025 and by just 0.7% in the year as a whole, the slowest rate in more than two decades.

This is a sharp slowdown from the growth of 4-11% in the preceding four years and marks the lowest rate of increase since 2001, excluding the impact of Covid in 2020.

This is the second in a new series of half-yearly analysis on India’s CO2 emissions from fossil fuels and cement, based on official data for fuel use, industrial production and power output.

Other key findings for 2025 as a whole include:

- Emissions in the power sector fell by 3.8% as record clean-energy growth combined with weak electricity demand.

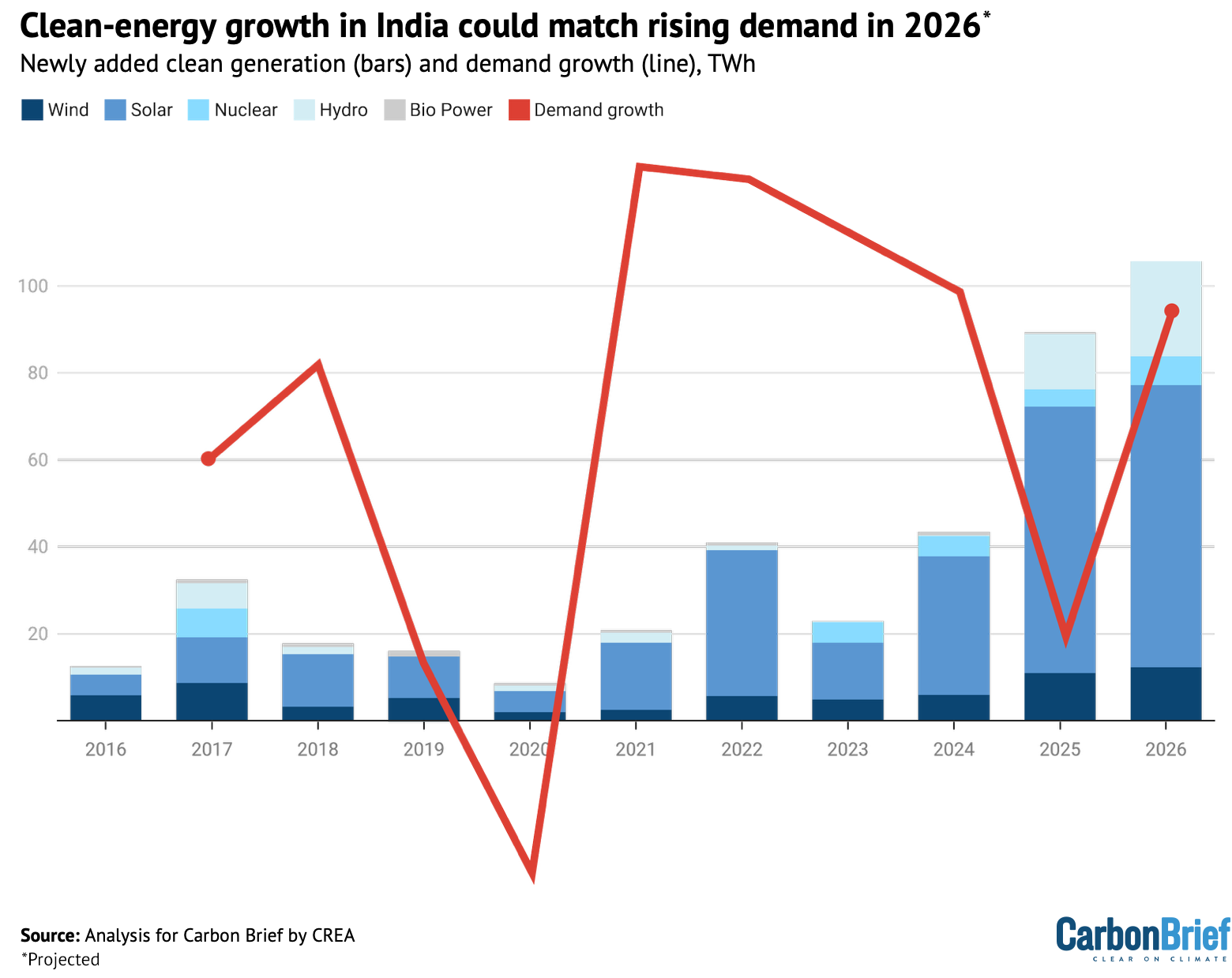

- New clean-energy capacity in 2025 will add a record 90 terawatt hours (TWh) of electricity output each year, double the previous record set in 2024.

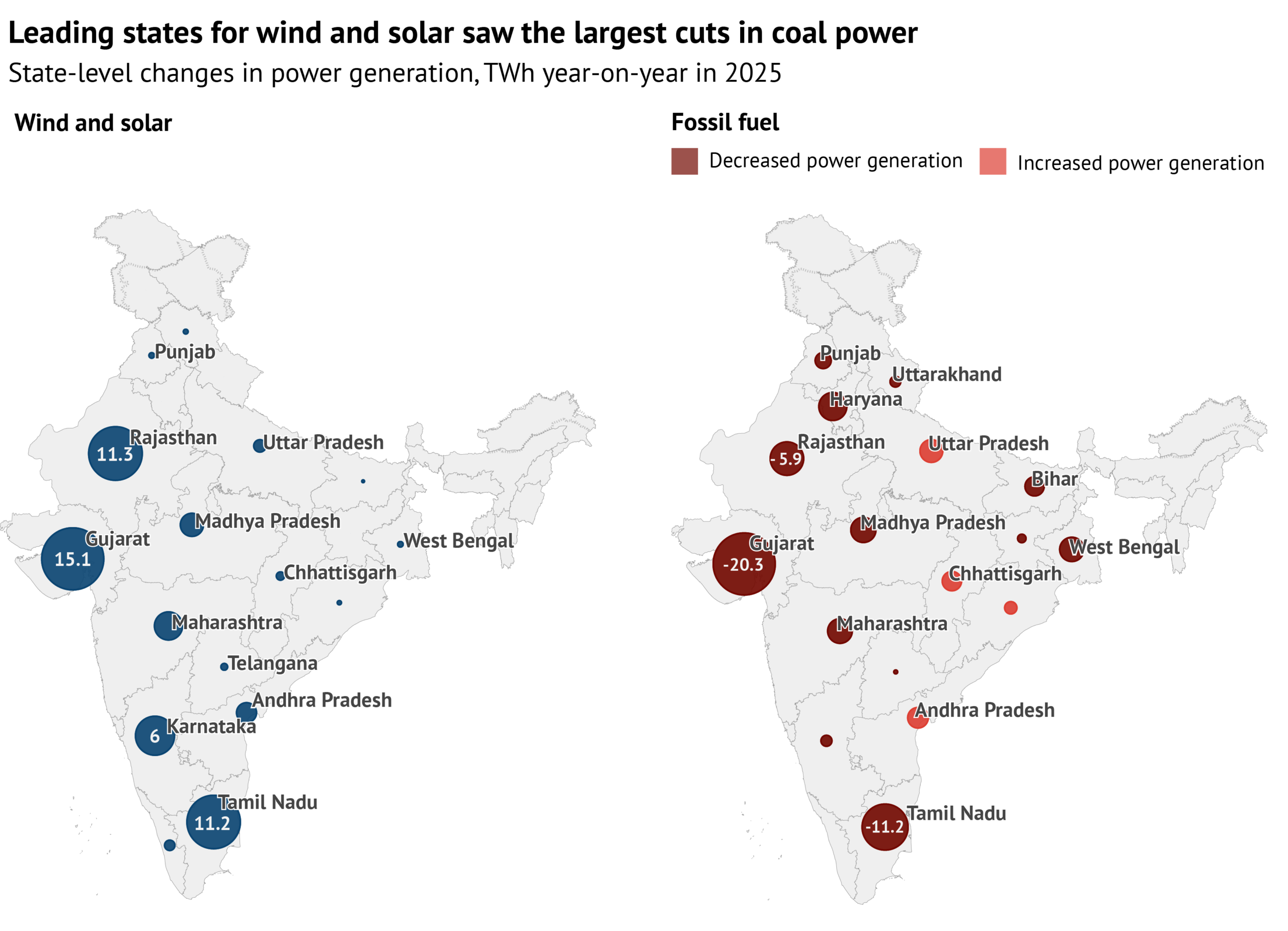

- The largest reductions in coal power were in the states leading on wind and solar.

- Oil demand grew by 0.4% and gas fell by 4%, far behind recent growth rates.

- Steel production surged by 8% and cement by 10%.

- In total, CO2 emissions went up slightly year-on-year, as increases from steel and cement outweighed the falls in gas demand and coal power.

- Consumption of imported coal at power plants fell by 20%, while gas imports fell by 6% and net oil imports were flat year-on-year, reducing India’s vulnerability to the impacts of the Iran war.

The analysis shows that India’s power sector is poised for a potential inflection point, where clean-energy additions can meet or exceed the growth in electricity demand.

If clean energy matches expectations, allowing this inflection point to take place, then coal-fired power output and the associated CO2 emissions would see sustained falls.

In addition, oil demand is falling in the petrochemical industry and is expected to slow down in the steel and cement sectors.

Despite these trends, which could signal a lasting slowdown in emissions, India is planning major expansions in its capacity for coal power, petrochemicals and coal-based steel.

The country’s Paris Agreement targets for 2035, which were published yesterday, did not reflect the potential for slower emissions increases or continued clean-energy growth.

The path of India’s CO2 emissions over the coming years depends on how it resolves these apparent contradictions regarding its future demand for fossil fuels.

Slowest growth since 2001

India’s CO2 emissions have been growing rapidly for decades, with annual increases averaging 4.9% per year since 1990 and 4-11% during 2021-24.

However, the recent pace of growth has been slowing down, as shown in the figure below. The 0.7% rise in 2025 was the slowest since 2001, excluding the impact of Covid in 2020.

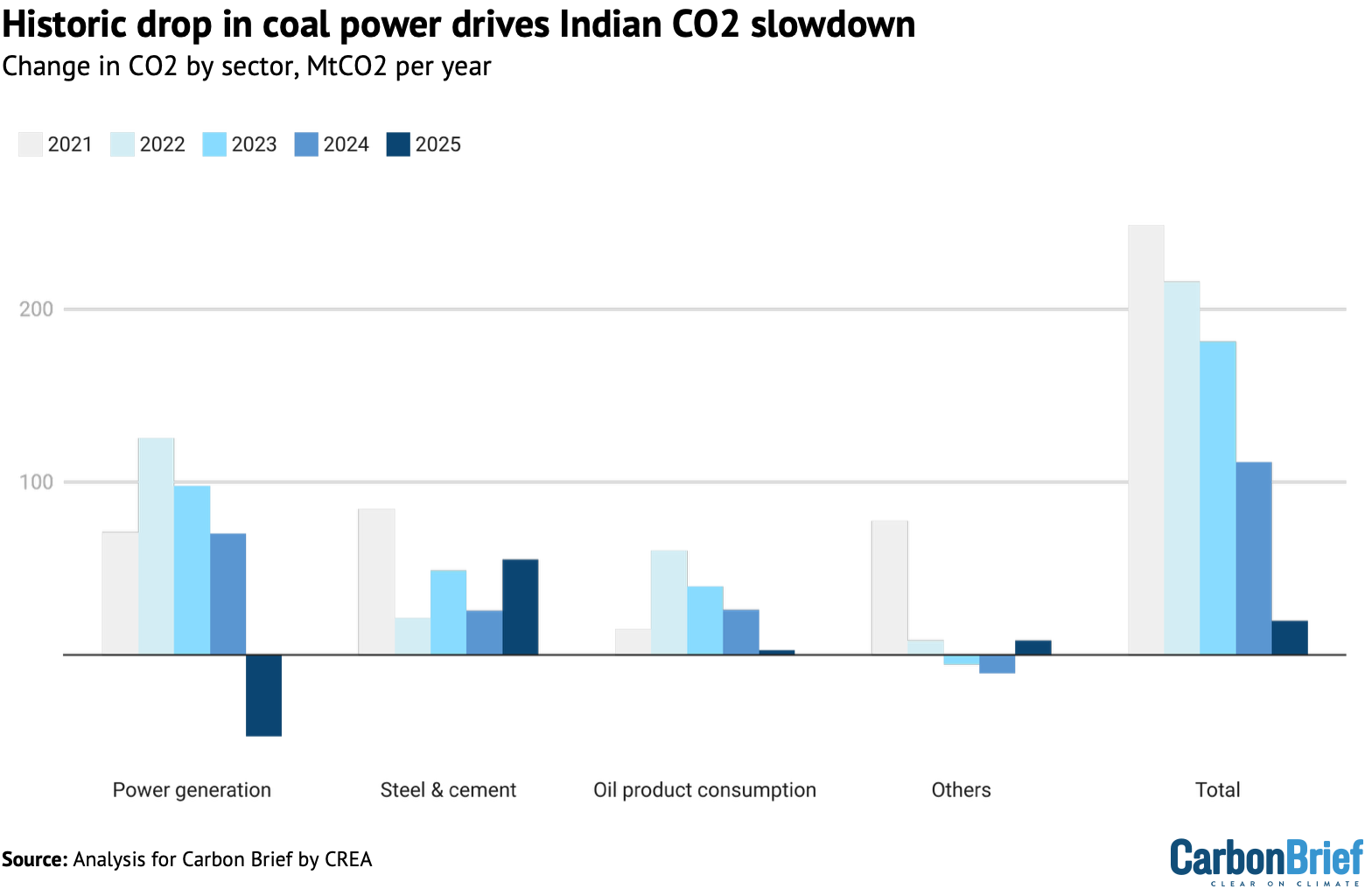

Beneath the overall rise of just 0.7% in 2025, there were divergent trends in India’s key emitting sectors, with some seeing rapid rises in CO2 and others in historic decline.

This is shown in the figure below, which compares year-on-year changes in emissions during the first and second half of 2025 with the average for 2021-23.

Specifically, emissions fell by 3.8% year-on-year in the power sector, after the first drop in coal-power generation – outside Covid – since 1973. Oil products were more or less flat.

The small increase in 2025 overall was the result of strong growth from steel and cement.

The fall in power-sector emissions is particularly notable, given it was the largest driver of emissions increases in 2021-2023, responsible for half of the total growth.

Across the sectors, the reductions and weak growth in fossil-fuel consumption eased India’s vulnerability to the recent price and supply disruptions taking place in the wake of the attacks on Iran by the US and Israel, as well as Iran’s subsequent retaliation.

Notably, India’s fossil-fuel imports were disproportionately affected by falling demand overall. For example, consumption of imported coal at power plants fell by 20% in 2025.

(Coal imports continued to fall in early 2026. However, the government is reported to be considering the use of an emergency clause that “would force coal power plants that run on imported coal to maximise output ahead of the summer season”, due to the impact of the Iran war on gas supplies.)

According to data from consultancy Kpler, gas imports fell 6% and net oil imports were flat, for the first time since the Covid-induced drop in 2020. The only rise in imports was of coal for steelmaking, which were up by 11% year-on-year in 2025.

Record clean-power growth

There were two key reasons why emissions fell in India’s power sector in 2025.

First, the country added 38 gigawatts (GW) of solar, 6.3GW of wind, 4.0GW of hydropower and 0.6GW of nuclear power in 2025.

The annual electricity generation from this new capacity, calculated based on the average capacity utilisation of each technology, amounts to 90 terawatt hours (TWh). This is twice as much as the clean generation added in 2024, which in itself was a record.

Power generation from solar grew by 30TWh and from wind by 20TWh in 2025, exceeding the 18TWh increase in total output. Hydropower also performed strongly due to high rainfall and capacity additions, with generation growing 21TWh.

Second, growth in total power demand slowed down from 7.4% in 2019-23 to 1% in 2025, which obviously played a major role in the fall in power-sector emissions.

The slow growth was due to both weather – with milder temperatures after 2024 heatwaves reducing the demand for air conditioning – and a more sustained slowdown in demand that had already started in late 2023 and was initially masked by the heatwaves. This slowdown in electricity demand is related to slower growth in industrial output and GDP.

Notably, the increase in clean-power generation from newly added capacity in 2025 was sufficient to cover demand growth of up to 5%. This means that power-sector emissions growth would have slowed down sharply, even if demand had not been flagging.

State-level analysis, shown in the figure below, emphasises the role of clean-energy growth in reducing fossil-powered generation.

The largest reductions in coal-fired power generation took place in Gujarat, Tamil Nadu and Rajasthan, the three states that also led the buildout of new solar and wind power.

Power demand is expected to pick up again, with Indian credit-rating agency ICRA projecting growth of 5.0-5.5% in the financial year starting in April 2026.

However, expected clean-energy additions should cover this level of growth.

BloombergNEF projects a 6% year-on-year increase in installed solar capacity in 2026. The government expects wind power capacity to reach 63GW by March 2027, a 10GW increase compared with the end of 2025, indicating a further acceleration of capacity additions compared with the 6GW added in 2025.

Indian utilities are also targeting the completion of construction on 6.8GW of new hydropower capacity, excluding pumped storage, and 1GW of nuclear capacity in 2026.

These capacity additions would deliver additional annual generation of more than 100TWh, enough to cover demand growth of up to 5.8%.

This means that India’s power sector could reach an inflection point this year, where clean-energy growth matches the expected average rise in demand, as shown below.

Over the next five years, ICRA forecasts annual average demand growth of 6.0 to 6.5%.

Yet India is also targeting 500GW non-fossil power generation capacity by the financial year 2029-2030. If achieved, this target would increase non-fossil power generation by enough to cover electricity demand growth of 6.6%, without needing to increase fossil-fuel generation, based on the Central Electricity Authority’s projected power generation.

If the actual growth rate for power demand is lower than this and if the non-fossil capacity target is still reached, then fossil-power generation – and the associated CO2 emissions – would fall in absolute terms from 2025 to financial year 2029-2030.

Battery energy storage is also increasingly affordable and will reduce the need for thermal power capacity in the system.

Oil slows on falling industrial demand

For oil demand, which slowed from 3.9% growth in 2024 to 0.4% in 2025, the key drivers came in the petrochemical and cement industry, where demand fell.

Specifically, demand fell for naphtha, petcoke and other oil products. Naphtha is used as chemical industry feedstock, while petcoke is used mainly in cement production.

Part of the fall in demand was due to an increase in India’s imports of plastics and precursors, which rose by 7% in volume terms, while exports fell.

The increase in imports came almost entirely from China, where the petrochemical industry is expanding, leading to complaints in India of price dumping. Mirroring the shift of plastics production to China, India began exporting large volumes of naphtha to the country.

India’s imports of nitrogen fertilisers also increased sharply, with most of the increase coming from China and Russia, while domestic production fell by 6% in April-September. Fertiliser production is the second-most important use of naphtha.

Petcoke use in cement production fell slightly, by 1%, even as cement production surged, as producers shifted to using more domestic coal in response to rising petcoke prices.

In the transport sector, petrol and diesel growth moderated in 2025, as the slow rebound to the pre-Covid trend in demand had finally played out. In addition, mobility was reduced in 2025 due to heavy monsoon rains in June to August.

Meanwhile, compressed natural gas (CNG) and electric vehicles also cut into the markets for passenger cars and light commercial vehicles, eating into petrol and diesel demand, respectively. EV sales grew 16% in 2025 and made up 8% of auto sales, helped by a reduction in the goods and services tax (GST) on EVs from 12% to 5%.

GST reform also reduced diesel consumption in a more surprising way, by eliminating the need for manual inspection of cargoes and cutting long wait-times at interstate border posts.

Diesel demand growth was also moderated by a government scheme to replace diesel irrigation pumps, which consume 5% of all diesel in the country, with solar-powered models.

Air pollution rules also played a role in some cities, including the capital Delhi. There, regulations on diesel vehicles resulted in a 13% reduction in sales from a year earlier, continuing the trend observed over the past two years.

Experts attribute lower sales of diesel vehicles to changes in consumer behaviour, following the long-standing ban on diesel vehicles older than 10 years and petrol models of more than 15 years in the wider Delhi National Capital Region (NCR), as well as a Supreme Court order in August 2025 that stressed the need for vehicles to comply with newer emissions rules.

Finally, aviation fuel demand growth slowed from 10% in 2024 to 3% in 2025, as the return to the pre-Covid trend in rising traffic leveled off.

The most immediate effect of the oil and gas crisis caused by the blockade of the Strait of Hormuz has been on the supply of liquified petroleum gas (LPG), which in India is used almost solely as cooking fuel.

Shortages have affected households, restaurants and industries. LPG consumption had grown by 6% year-on-year in 2025, in line with the longer-term trend, but is responsible for only 3% India’s CO2 emissions.

The crisis has reportedly also prompted a shift to cooking with electricity, with the sales of induction stoves reportedly surging.

Steel and cement continue to surge

The overall rise in India’s emissions in 2025 was driven by strong growth in output for steel and cement, which went up by 8% and 10%, respectively. The two sectors were responsible for 21% of India’s total CO2 emissions from fossil fuels and industrial processes in 2025.

India’s steel sector is more polluting than elsewhere, with the CO2 per unit of production – its emissions intensity – being more than 20% higher than the global average.

Two-thirds of steel is used for construction. Strong steel demand in 2025 reflected growth in new housing construction in earlier years, as the market was rebounding from the mid-2010s crash and the Covid pandemic. However, new project launches and sales both declined in 2025.

Domestic steel output growth was attenuated in the first half of the year by increases in steel imports from China, Japan and South Korea. This resulted in the government enacting a temporary blanket tariff in April 2025 for 200 days to curb imports.

As a result, steel output growth accelerated from 6% in January to May to 10% in the rest of the year. In November 2025, when the earlier temporary tariff expired, the government imposed new tariffs on a more targeted list of countries.

It imposed a three-year step-down tariff – 12% in the first year, 11.5% in year two and 11% in year three – to curb imports from China, Vietnam and Nepal, as these countries were found to exceed the thresholds for imports for various steel products.

In spite of the tariffs, the industry is struggling with weak profitability. Output growth has “led to a situation of oversupply”, according to ICRA, resulting in falling profitability and capacity utilisation, particularly at smaller mills, which account for 41% of total steel production.

Delays in construction and infrastructure projects are also weighing down on India’s steel demand, leading to rising inventories and falling prices. This is likely to affect the demand for steel, cement and bitumen in 2026.

Meanwhile, government initiatives could encourage a shift in the type and emissions intensity of steel production. State-backed schemes – particularly programmes to build affordable urban and rural housing – are significant steel demand drivers.

The Ministry of Steel is working on mandates for “green steel” in public procurement as part of a broader Green Steel Mission aimed at decarbonising the sector.

The policy is expected to require government agencies and publicly funded projects to buy lower-emission steel, creating demand for greener production.

Power could be nearing an inflection point

The sharp slowdown in India’s overall CO2 emissions growth has now lasted 18 months, making it increasingly likely that it is not just a blip.

Electricity demand growth slowed down sharply in 2025, which could be taken to imply that the lower growth in CO2 last year was mainly down to fluctuations in power demand.

However, clean-energy growth in 2025 was large enough to have stabilised emissions in the power sector, even if demand growth had been at historical rates.

Now, power-sector emissions could be about to reach an inflection point, with clean-energy additions projected to overtake average rate of electricity demand growth in 2026, for the first time. This already happened in 2025 in Gujarat, Rajasthan and Tamil Nadu, the highly populated states leading solar and wind development.

If clean-energy growth rates continue and if demand growth stays at expected levels, then clean energy will cover all of the growth in electricity demand. This would mean that electricity generation from fossil fuels would level off or decline.

Given that the power sector was the largest driver of emissions increases in 2021-2023, peaking coal-fired power generation and emissions from the sector would have a major impact on India’s overall fossil-fuel consumption and emissions.

The other significant emitting sector where emissions have been falling in India is the petrochemical industry.

In contrast, the steel industry has continued to increase output, even though it is struggling with profitability and concerns about overcapacity, while demand for steel and cement is expected to cool down this year due to lower growth in construction volumes.

Despite these trends, the country is planning for a major expansion of all of these industries. The government plans to add 85GW of new coal-fired power capacity over the next seven years. The country is also targeting $1tn of investment in the petrochemical industry by 2040, a 50% increase in steel production capacity from 2025 to 2031 and a 25% increase in cement production capacity in the three years from 2026 to 2028.

The planned investment in steelmaking is overwhelmingly coal-based capacity. This will increase the sector’s reliance on metallurgical coal, which is almost entirely imported, as well as running against government ambitions to increase lower-carbon steelmaking.

India’s Cabinet approved new 2035 climate pledges for the country yesterday. The targets are a reduction in carbon intensity – the emissions per unit of GDP – of 47% from 2005 level by 2035 and a non-fossil energy share of 60% in power generation capacity.

The 60% target would already be achieved by 2030, under the Central Electricity Authority’s recent projections. The carbon-intensity target would allow the country’s CO2 emissions growth to accelerate in the next 10 years, compared with the preceding decade, even as the recent clean-energy growth suggests that a substantial slowdown is possible.

If GDP growth averages 7.8%, the rate needed to meet India’s 2047 economic goals, then CO2 emissions could increase at 6% per year from 2025 to 2035 while still meeting the carbon-intensity target, compared with less than 4% growth from 2015 to 2025.

India’s energy and emissions trajectory over the next 5-10 years will depend heavily on how these apparent contradictions are resolved. This is particularly true in the power sector, where clean energy and storage are already set to cover future growth.

About the data

This analysis is based on official monthly data for fuel consumption, industrial production and power generation from different ministries and government institutes.

Coal consumption in thermal power plants is taken from the monthly reports downloaded from the National Power Portal of the Ministry of Power. The data is compiled for the period January 2019 until June 2025. Power generation and capacity by technology and fuel on a monthly basis are sourced from the NITI data portal.

Coal use at steel and cement plants, as well as process emissions from cement production, are estimated using production indices from the index of eight core industries released monthly by the Office of Economic Adviser, assuming that changes in total fossil fuel use follow production volumes.

These production indices were used to scale fuel use by the sectors in 2022. To form a basis for using the indices, monthly coal consumption data for 2022 was constructed for the sectors using the annual total coal and petcoke consumption reported in IEA World Energy Balances and monthly production data in a paper by Robbie Andrew, on monthly CO2 emission accounting for India. Monthly petcoke consumption was available from the Petroleum Planning and Analysis Cell, and coal consumption by the cement industry was calculated by subtracting petcoke use from total fossil fuel use.

Annual cement process emissions up to 2024 were also taken from Robbie Andrew’s work and scaled using the production indices. This approach better approximated changes in energy use and emissions reported in the IEA World Energy Balances, than did the amounts of coal reported to have been dispatched to the sectors, showing that production volumes are the dominant driver of short-term changes in emissions.

For other sectors, including aluminium, auto, chemical and petrochemical, paper and plywood, pharmaceutical, graphite electrode, sugar, textile, mining, traders and others, coal consumption is estimated based on data on despatch of domestic and imported coal to end users from statistical reports and monthly reports by the Ministry of Coal, as consumption data is not available.

Coal consumption by “captive” coal power plants – those supplying power to industrial sites, not to the public electricity network – was calculated based on capacity changes from Global Energy Monitor, assuming constant utilisation, as utilisation has been very stable year-to-year, as calculated from Central Electricity Authority data.

The difference between coal consumption and dispatch is stock changes, which are estimated by assuming that the changes in the amount of coal stored at end user facilities mirror those at coal mines, with end user inventories excluding power, steel and cement assumed to be 70% of those at coal mines, based on comparisons between our data and the IEA World Energy Balances.

Stock changes at mines are estimated as the difference between production at and dispatch from coal mines, as reported by the Ministry of Coal.

Coal consumption is estimated in two ways, for sectors beyond power, steel and cement. Consumption of domestic coal in these other sectors is taken from the monthly reports by the Ministry of Coal. Their consumption of imported coal is estimated from the total imports of thermal coal reported by consultancy Kpler, by subtracting demand for imports at coal-power plants. The basis for this assumption is that steel and cement industries use little imported thermal coal, according to Ministry of Coal data.

Product-by-product consumption data for petroleum products, as well as gas use by sector, is from the Petroleum Planning and Analysis Cell of the Ministry of Petroleum and Natural Gas.

As the fuel dispatch and consumption data is reported as physical volumes – such as tonnes or litres – calorific values are taken from IEA’s World Energy Balance and CO2 emission factors from 2006 IPCC Guidelines for National Greenhouse Gas Inventories.

Calorific values are assigned separately to different fuel types, including domestic and imported coal, anthracite and coke, as well as to petrol, diesel and several other oil products.

The post Analysis: India’s CO2 emissions in 2025 grew at slowest rate in two decades appeared first on Carbon Brief.

Analysis: India’s CO2 emissions in 2025 grew at slowest rate in two decades

George Carlin Blended Comedy with Social Commentary

Trump Admin Pays TotalEnegries $1B to Scrap Wind Projects, Putting a Hold on America’s Clean Energy Plans

Guest post: How declining cloudiness is accelerating global warming

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Renewable Energy5 months ago

Renewable Energy5 months agoSending Progressive Philanthropist George Soros to Prison?