Ten years ago, switching from burning coal to gas was a key element of China’s policy to reduce severe air pollution.

However, while gas is seen in some countries as a “bridging” fuel to move away from coal use, rapid electrification, uncompetitiveness and supply concerns have suppressed its share in China’s energy mix.

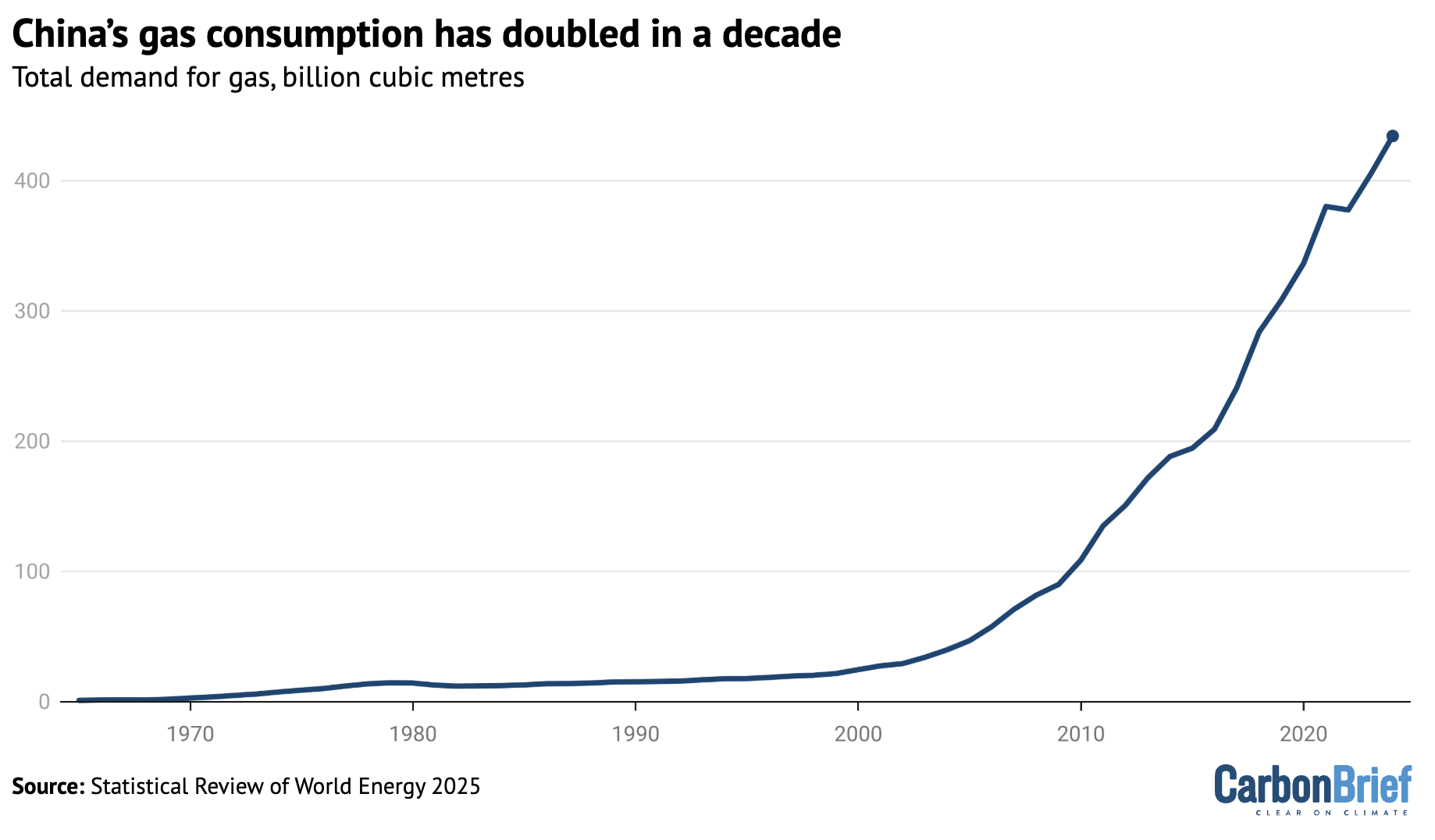

As such, while China’s gas demand has more than doubled over the past decade, the fuel is not currently playing a decisive role in the country’s strategy to tackle climate change.

Instead, renewables are now the leading replacement for coal demand in China, with growth in solar and wind generation largely keeping emissions growth from China’s power sector flat.

While gas could play a role in decarbonising some aspects of China’s energy demand – particularly in terms of meeting power demand peaks and fuelling heavy industry – multiple factors would need to change to make it a more attractive alternative.

Small, but impactful

The share of gas in China’s primary energy demand is small and has remained relatively unchanged at around 8-9% over the past five years.

It also comprises 7% of China’s carbon dioxide (CO2) emissions from fuel combustion, according to the International Energy Agency (IEA).

Gas combustion in China added 755m tonnes of CO2 (MtCO2) into the atmosphere in 2023 – double the total amount of CO2 emitted by the UK.

However, its emissions profile in China lags well behind that of coal, which represented 79% of China’s fuel-linked CO2 emissions and was responsible for almost 9bn tonnes of CO2 emissions in 2023, according to the same IEA data.

Gas consumption continues to grow in line with an overall uptick in total energy demand. Chinese gas demand, driven by industry use, grew by around 7-8% year-on-year in 2024, according to different estimates.

This rapid growth is, nevertheless, slightly below the 9% average annual rise in China’s gas demand over the past decade, during which consumption has more than doubled overall, as shown in the figure below.

The state-run oil and gas company China National Petroleum Corporation (CNPC) forecast in 2025 that demand growth for the year may slow further to just over 6%.

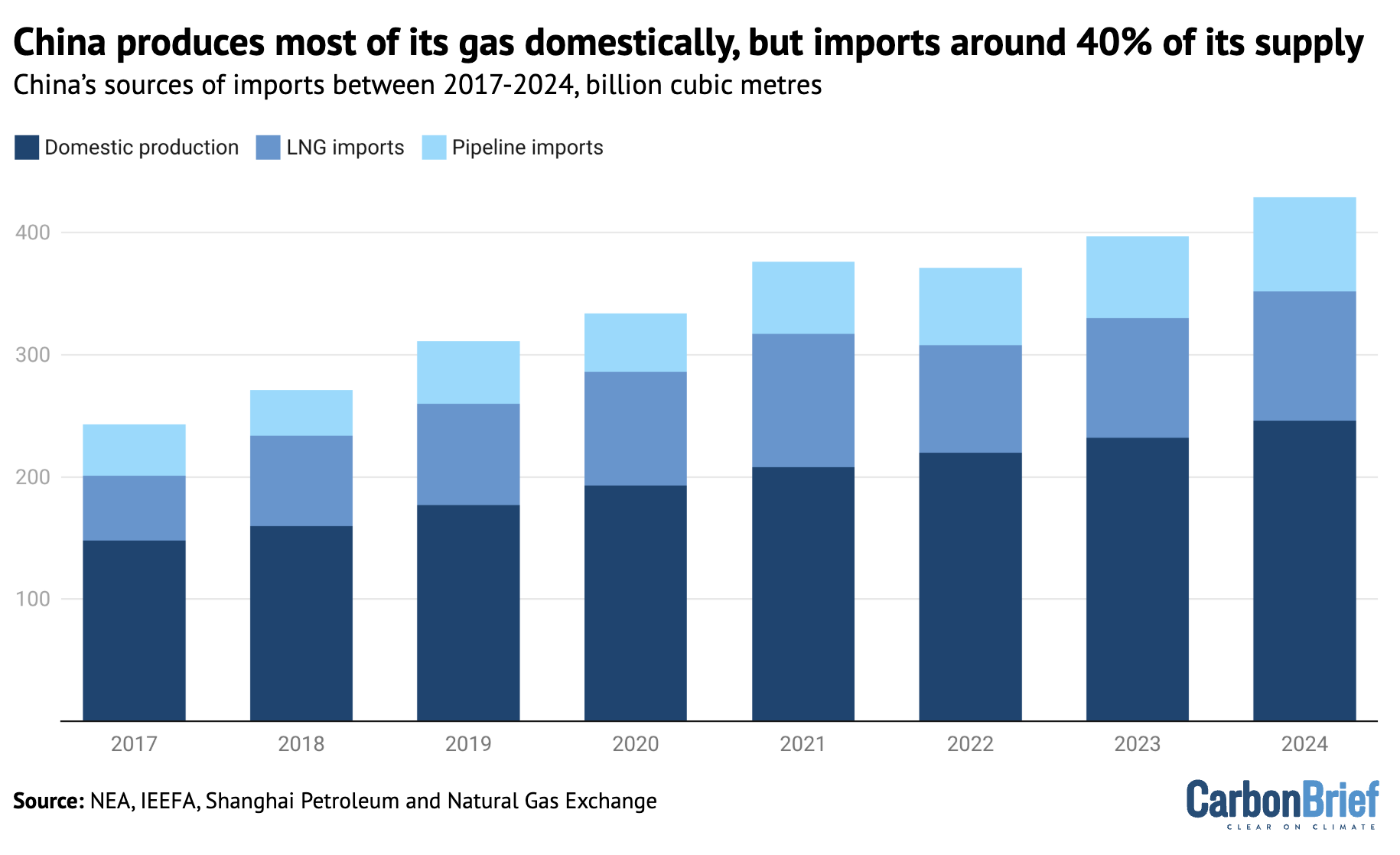

The majority of China’s gas demand in 2023 was met by domestic gas supply, according to the Institute for Energy Economics and Financial Analysis (IEEFA).

Most of this supply comes from conventional gas sources. But incremental Chinese domestic gas supply in recent years has come from harder-to-extract unconventional sources, including shale gas, which accounted for as much as 45% of gas production in 2024.

Despite China’s large recoverable shale-gas resources and subsidies to encourage production, geographical and technical limitations have capped production levels relative to the US, which is the world’s largest gas producer by far.

CNPC estimates Chinese gas output will grow by just 4% in 2025, compared with 6% growth in 2024. Nevertheless, output is still expected to exceed the 230bn cubic metre national target for 2025.

Liquified natural gas (LNG) is China’s second most-common source of gas, imported via giant super-cooled tankers from countries including Australia, Qatar, Malaysia and Russia.

This is followed by pipeline imports – which are seen as cheaper, but less reliable – from Russia and central Asia.

One particularly high-profile pipeline project is the Power of Siberia 2 pipeline project. However, Beijing has yet to explicitly agree to investing in or purchasing the gas delivered by the project. Disagreements around pricing and logistics have hindered progress.

Evolving role

Beijing initially aimed for gas to displace coal as part of a broader policy to tackle air pollution.

A three-year action plan from 2018-2020, dubbed the “blue-sky campaign”, helped to accelerate gas use in the industrial and residential sectors, as gas displaced consumption of “dispersed coal” (散煤)”– referring to improperly processed coal that emits more pollutants.

Meanwhile, several cities across northern and central China were also mandated to curtail coal usage and switch to gas instead. Many of these cities were based in provinces with a strong coal mining economy or higher winter heating demand.

China’s pollution levels saw “drastic improvement” as a result, according to a report by research institute the Centre for Research on Energy and Clean Air (CREA).

(In January 2026, there were widespread media reports of households choosing not to use gas heating despite freezing temperatures, as a result of high prices following the expiry of subsidies for gas use.)

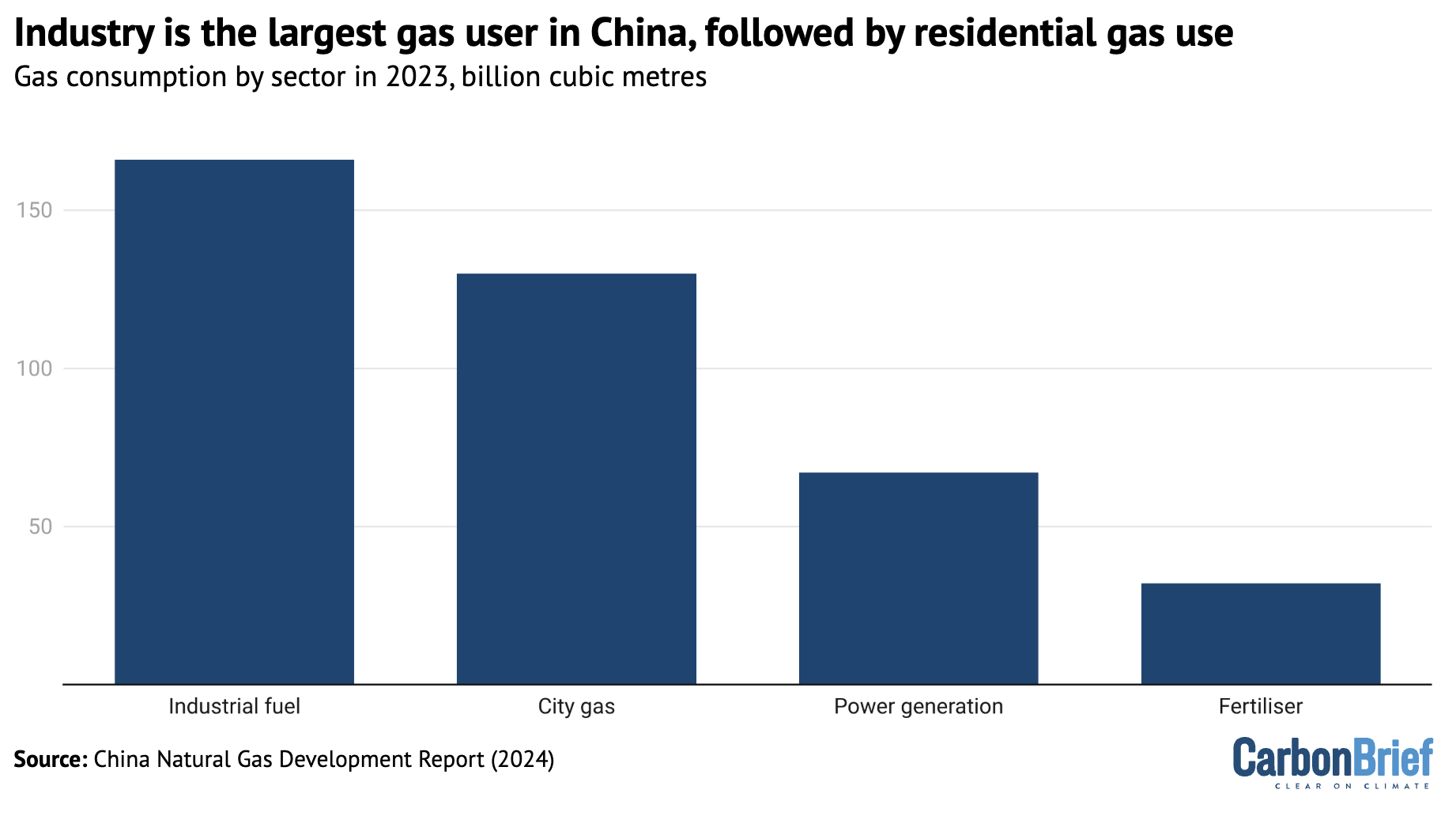

Industry remains the largest gas user in China, with “city gas” – gas delivered by pipeline to urban areas – trailing in second, as shown in the figure below. Power generation is a distant third.

Gas has never gained momentum in China’s power sector, with its share of power generation remaining at 4% while wind and solar power’s share has soared from 4% to 22% over the past decade, Yu Aiqun, a research analyst at the US-based thinktank Global Energy Monitor, tells Carbon Brief.

Yu adds that this stagnation is largely due to insufficient and unreliable gas supply, which drives up prices and makes gas less competitive compared to coal and renewables. She says:

“With the rapid expansion of renewables and ongoing geopolitical uncertainties, I don’t foresee a bright future for gas power.”

Average on-grid gas-fired power prices of 0.56-0.58 yuan per kilowatt hour (yuan/kWh) in China are far higher than that of around 0.3-0.4 yuan/kWh for coal power, according to some industry estimates. Recent auction prices for renewables are even cheaper than this.

Meanwhile, the share of renewables in China’s power capacity stood at 55% in 2024, compared with gas at around 4%.

Generation from wind and solar in particular has increased by more than 1,250 terawatt-hours (TWh) in China since 2015, while gas-fired generation has increased by just 140TWh, according to IEEFA.

As the share of coal has shrunk from 70% to 61% during this period, IEEFA suggests that renewables – rather than gas – are displacing coal’s share in the generation mix.

However, China’s gas capacity may still rise from approximately 150 gigawatts (GW) in 2025 to 200GW by 2030, Bloomberg reports.

A report by the National Energy Administration (NEA) on development of the sector notes that gas will continue to play a “critical role” in “peak shaving”, where gas turbines can be used for short periods to meet daily spikes in demand. As such, the NEA says gas will be an “important pillar” in China’s energy transition.

In 2024, a new policy on gas utilisation also “explicitly promoted” the use of gas peak-shaving power plants, according to industry outlet MySteel.

China’s current gas storage capacity is “insufficient”, according to CNPC, reducing its ability to meet peak-shaving demand. The country built 38 underground gas storage sites with peak-shaving capacity of 26.7bn cubic metres in 2024, but this accounts for just 6% of its annual gas demand.

Transport use

Gas is instead playing a bigger part in the displacement of diesel in the transport sector, due to the higher cost competitiveness of LNG as a fuel – particularly in the trucking sector.

CNPC expects that LNG displaced around 28-30m tonnes of diesel in the trucking sector in 2025, accounting for 15% of total diesel demand in China.

This is further aided by policy support from Beijing’s equipment trade-in programme, part of efforts to stimulate the economy.

However, gas is not necessarily a better option for heavy-duty, long-haul transportation, due to poorer fuel efficiency compared with electric vehicles (EVs).

In fact, “new-energy vehicles” (NEVs) – including hydrogen fuel-cell, pure-electric and hybrid-electric trucks – are displacing both LNG-fueled trucks and diesel heavy-duty vehicles (HDVs).

In the first half of 2025, battery-electric models accounted for 22% of all HDV sales, a year-on-year increase of 9%, while market share for LNG-fueled trucks fell from 30% in 2024 to 26%.

Gas can be cheaper than oil but is not competitive with EVs and – with the emergence of zero-emission fuels such as hydrogen and ammonia – gas may eventually lose even this niche market, says Yu.

Supply security

Chinese government officials frequently note that China is “rich in coal, poor in oil and short of gas” (“富煤贫油少气”). Concerns around import dependence have underpinned China’s focus on coal as a source of energy security.

However, Beijing increasingly sees electrification as a more strategic way to decarbonise its transport sector, according to some analysts.

“Overall, electrification is a clear energy security strategy to reduce exposure to global fossil fuel markets,” says Michal Meidan, head of the China energy research programme at the Oxford Institute for Energy Studies.

Chinese oil and gas production grew dramatically in the last few years under a seven-year action plan from 2019-25, as Beijing ordered its state oil firms to ramp up output to ensure energy security.

Despite this, gas import dependency still hovers at around 40% of demand. This, according to assessments in government documents, exposes the country to price shocks and geopolitical risks.

The graph below shows the share of domestically produced gas (dark blue), LNG imports (mid-blue) and pipeline imports (light blue), in China’s overall gas supply between 2017 and 2024.

“Gas use is unlikely to play a significant role in decarbonising the power system, but could be more significant in industrial decarbonisation,” Meidan tells Carbon Brief.

She estimates that if LNG prices fall to $6 per million British thermal units (btu), compared to an average of $11 in 2024-25, this could encourage fuel switching in the steel, chemical manufacturing, textiles, ceramics and food processing industries.

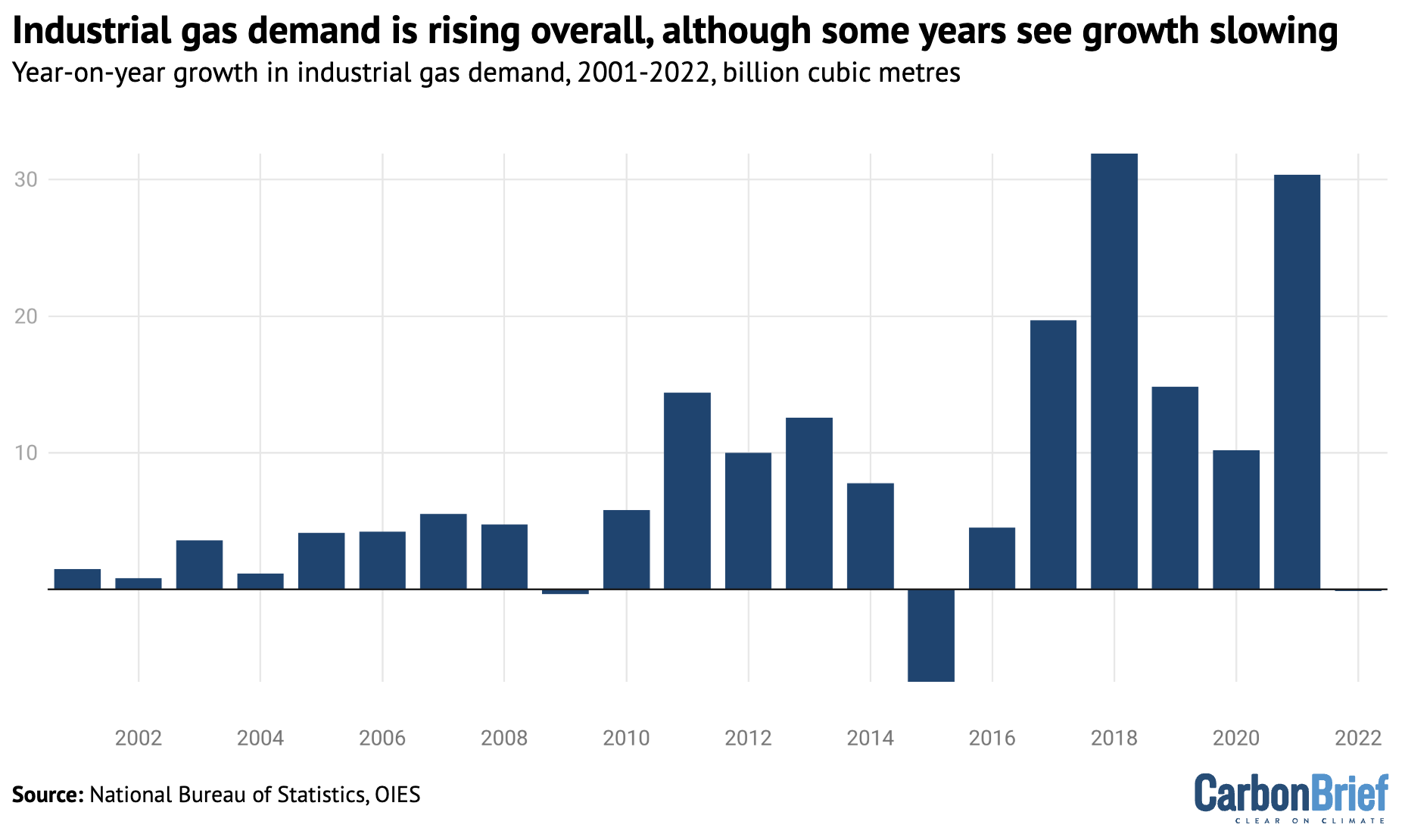

The chart below shows the year-on-year change in gas demand between 2001-2022.

Growth in gas demand has been decelerating in some industries in recent years, such as refining. But it also remains unclear if Beijing will adopt more aggressive policies favouring gas, Meidan adds.

A roadmap developed by the Energy Research Institute (ERI), a thinktank under the National Development and Reform Commission’s Academy of Macroeconomic Research, finds that gas only begins to play an equivalent or greater role in China’s energy mix than coal by 2050 at the earliest – 10 years ahead of China’s target for achieving carbon neutrality.

Both fossil fuels play a significantly smaller role than clean-energy sources at this point.

Wang Zhongying and Kaare Sandholt, both experts at the ERI, write in Carbon Brief:

“Gas does not play a significant role in the power sector in our scenarios, as solar and wind can provide cheaper electricity while existing coal power plants – together with scaled-up expansion of energy storage and demand-side response facilities – can provide sufficient flexibility and peak-load capacity.”

Ultimately, China’s push for gas will be contingent on its own development goals. Its next five-year plan, from 2026-2030, will build a framework for China’s shift to controlling absolute carbon emissions, rather than carbon intensity.

Recent recommendations by top Chinese policymakers on priorities for the next five-year plan did not explicitly mention gas. Instead, the government endorses “raising the level of electrification in end-use energy consumption” while also “promoting peaking of coal and oil consumption”.

The Chinese government feels that gas is “nice to have…if available and cost-competitive but is not the only avenue for China’s energy transition,” says Meidan.

The post Explainer: Why gas plays a minimal role in China’s climate strategy appeared first on Carbon Brief.

Explainer: Why gas plays a minimal role in China’s climate strategy

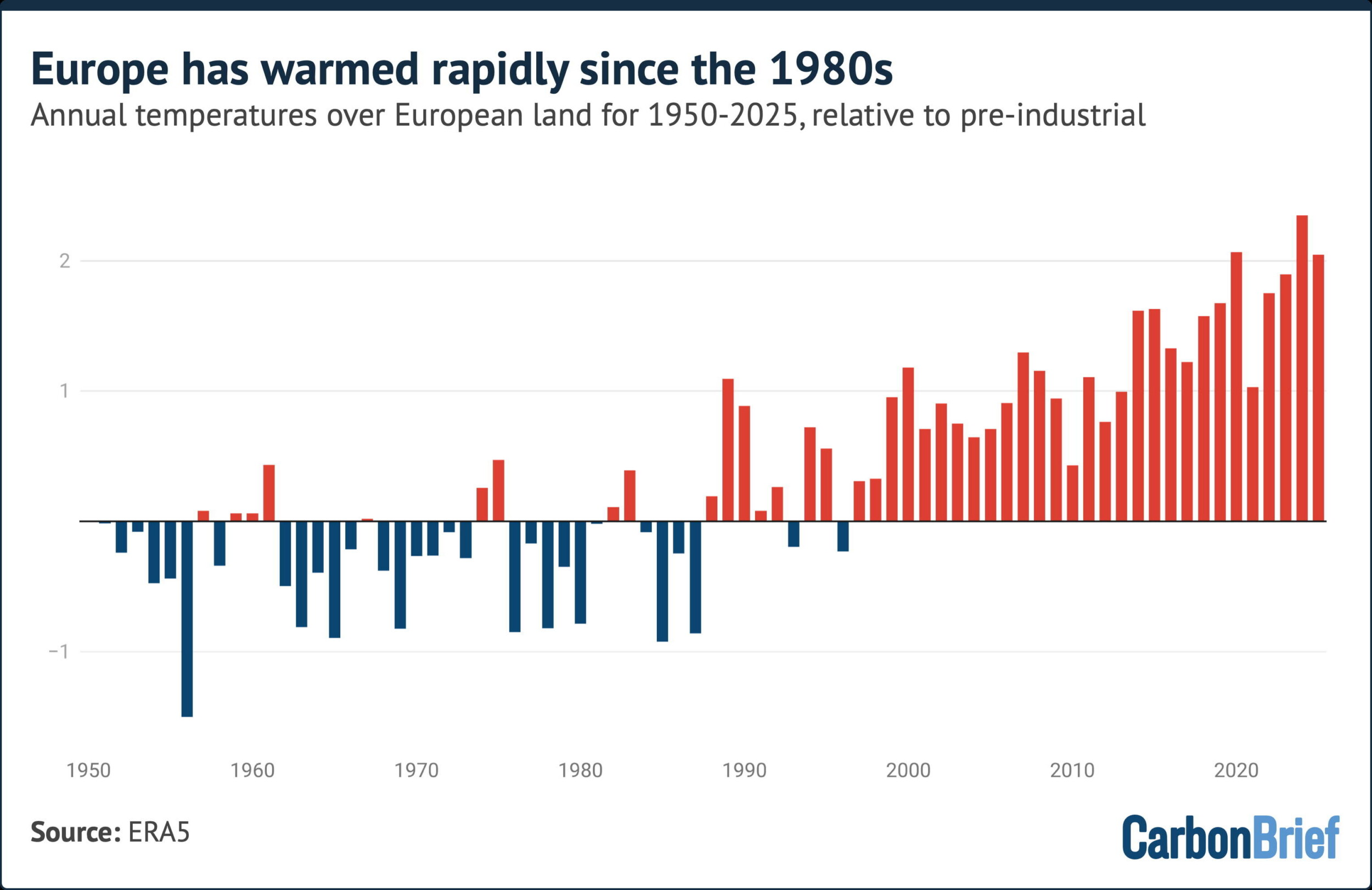

This summer has seen Europe suffer through a series of record-breaking heatwaves.

Amid widespread media coverage of the number of deaths and the influence of climate change, the UK’s Daily Telegraph reported on new research with the incorrect headline: “Heatwaves caused by fall in pollution.”

The article was shared on social media by Richard Tice – deputy leader of the hard-right, climate-sceptic Reform UK party – along with a number of prominent rightwing commentators.

Tice claimed that “net stupid zero is contributing to rising temperatures, not helping”, adding that “we have been gaslit and lied to”.

GB News followed up with its own article, incorrectly headlined: “Britain’s scorching heatwaves caused by falling pollution levels, researchers find.”

Scientists tell Carbon Brief that the framing of heatwaves being “caused” by declining air pollution is “wrong”.

While a drop in pollution has reduced the cooling impact it has had in the past, the scientists say, Europe’s summer heatwaves are primarily becoming more extreme “as a result of greenhouse-gas-induced warming”.

Another scientist adds that “any attempt” to link this research to net-zero policies is “simply wrong”.

Fast warming

The extensive reporting around Europe’s heatwaves in recent months has often mentioned that Europe is the world’s fastest-warming continent.

The new study in question aims to unpack why Europe’s summer temperatures are rising more quickly than other regions of the northern hemisphere’s mid and high latitudes.

The research – published in Geophysical Research Letters – explores the role of air pollution and, specifically, how it affects circulation patterns in the atmosphere.

(The study focuses on long-term trends in European summers and does not include the very recent heatwaves.)

Human-caused emissions of aerosols – tiny, light‑scattering particles produced mainly by burning fossil fuels – have long acted to “mask” global warming. This is largely because they absorb or reflect incoming sunlight and influence the formation and brightness of clouds.

To understand how the climate of Europe – or any region – is changing, scientists need to take into account a whole range of factors, says Prof Bjørn Samset, a research professor at Norway’s Center for International Climate Research (CICERO), who was not involved in the work.

This includes “greenhouse gases, aerosols, land-use change, natural variability and how they all interact”, he says, adding:

“The effects of air pollution on circulation, which is the topic here, has long been difficult to pin down.”

As European countries improved their air quality through the second half of the 20th century, the cooling effect of aerosols has gradually been removed.

This can boost heatwaves in two ways – directly, by letting more sunlight reach the land surface and, indirectly, by influencing the jet stream.

Using hundreds of simulations from nine climate models, the new study finds that a decline in aerosols is resulting in more frequent “quasi-stationary Rossby waves”.

Rossby waves are huge meanders in the jet stream. Occasionally, they become slow-moving – or “quasi-stationary” – which allows weather systems to get stuck over one region, leading to prolonged heatwaves.

These circulation changes have contributed to Europe’s rapidly warming summers.

However, while Europe’s heatwaves are being influenced by declining aerosols, it is “wrong” to say they are being “caused” by them, says Prof Erich Fischer, a climate scientist at ETH Zurich.

Fischer, who was not involved in the study, tells Carbon Brief:

“Heatwaves are caused by high-pressure systems and are now much more frequent and intense because they are happening in a climate that is much warmer than 100 years ago as a result of greenhouse-gas-induced warming.

“The paper shows that the greenhouse-gas-induced summer warming had been temporarily masked by air-polluting aerosols. The full extent for European summers only becomes visible now as the air-polluting aerosols have declined.”

Samset adds:

“Air pollution never causes or removes global warming, it only temporarily moderates it.”

Study lead author Dr Pedro Roldán‐Gómez, an associate researcher at the Barcelona Supercomputer Centre, is quoted in the Daily Telegraph saying that “most” of the “excess warming” in Europe, beyond that of comparable regions in the northern hemisphere, can be linked to declining aerosols.

But, earlier in the article, the newspaper interprets this as, simply, “most of the extra heat experienced in Britain and Europe” is down to air pollution.

GB News uses a similar phrasing, reporting that “much of the additional warming across Britain and western Europe since the 1980s is linked to the sharp decline in airborne particles known as aerosols”.

This is “misleading”, says Fischer, while Roldan-Gomez tells Carbon Brief that this is a “tricky point”, which “could lead to wrong interpretations if not properly explained”. He adds:

“The contribution of greenhouse gases is, in any case, the most important factor.”

Cleaner air

The Daily Telegraph’s article was seized upon by Reform’s Richard Tice to claim that “cleaner air” was causing higher temperatures, rather than CO2.

This continued his position – refuted by long-established climate science – that CO2 does not drive global warming.

Tice also claimed in his post that net-zero policies are “contributing to rising temperatures”. Tice appears to be linking declining air pollution to a shift from fossil fuels to renewable energy.

Samset points out that net-zero became a goal “decades later” than the cumulative efforts to reduce air pollution since the 1980s and that it is “simply wrong” to link it to the study.

“The scientific community will keep working to understand how greenhouse gas warming and air pollution interact,” he says, but “nothing we do will change the fact that the consequences of global warming are due to human-induced CO2 emissions”.

Fischer adds:

“Let us not forget that cleaning up air-polluting aerosols is highly desirable. According to the World Health Organisation, 7 million people still die prematurely every year due to air pollution.”

Clean air legislation

Finally, the Daily Telegraph article and the study itself both attribute Europe’s declining air pollution from the 1980s onwards to the Montreal Protocol.

This is a “glaring error”, Samset says, and it is “surprising that it wasn’t picked up” in the peer-review process for the study. He explains:

“The Montreal Protocol did not deal with air pollution. It dealt with ozone-depleting gases and has been an extremely successful multi-national effort against environmental damage. “

Clean air legislation was already in place in many European countries by the time the Montreal Protocol was signed in 1987, says Samset.

In response, Roldán‐Gómez says that while the protocol did not target aerosols specifically, it “boosted the clean air policies”.

The post Factcheck: No, Europe’s heatwaves are not being ‘caused’ by declining air pollution appeared first on Carbon Brief.

Factcheck: No, Europe’s heatwaves are not being ‘caused’ by declining air pollution

Empowering women through greater access to finance could “strengthen” households’ resilience to “climate shocks”, according to a new study.

Published in Climate Risk Management, it analyses the impact of financial access on “women-headed households” in sub-Saharan Africa.

The study finds that where women had formal financial access – such as through owning a bank account – households were more able to withstand short-term shocks.

It adds that “climate shocks”, such as extreme weather events and the impacts of climate change, can cause economic crises, which destabilise communities and households.

However, the authors say that in order to protect households from long-term climate vulnerabilities – including “droughts, floods and sea-level rise” – financial access would need to be paired with wider efforts to tackle gender inequality.

They add that the findings could have important implications for policy in sub-Saharan Africa, where many countries and households are vulnerable to climate disasters.

Financial inclusion

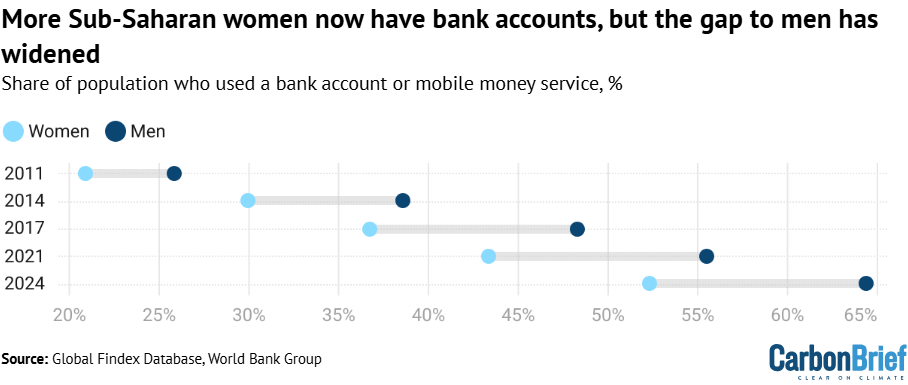

The study highlights that entrenched gender disparities mean many women still have unequal access to financial services in sub-Saharan Africa

For example, women are still less likely to have their own bank accounts and instead are often dependent on male relatives for access to finance.

The number of women with access to an account in the region had risen to 52% as of 2024, according to data from World Bank Group.

However, as shown in the chart below, the gap between men and women has also increased, rising from just under 5 percentage points in 2011 to 12 in 2024.

Using survey data from Afrobarometer, the new study analyses 25,511 women-headed households across 37 sub-Saharan countries.

The authors use the Organisation for Economic Co-operation and Development’s (OECD) framework to measure “financial inclusion”. This looks at factors such as having a bank account, owning a mobile phone and having internet access.

Francis Anaisie, a co-author on the study, tells Carbon Brief the researchers were motivated by the UN’s sustainable development goals (SDGs). Anaisie, an economist at the University of Cape Coast, Ghana, says the study specifically looked at SDGs five and 13, on gender equality and addressing climate issues. He adds:

“Financial inclusion is one of the key policy tools for empowering women or for empowerment. But as to whether this actually translates into better climate outcomes for women is not known or is limited; this study seeks to address that gap.”

The study finds households with higher levels of financial access for women had higher levels of women’s empowerment, when this is defined as the ability to make choices and have control over economic and social outcomes.

This was checked by cross-comparing financial access against different measures of women’s empowerment, such as financial security, voting rights and connection to communities.

In particular, the study found that “financially included” women had greater political and economic empowerment, such as financial security and voting rights. On some measures of social empowerment, however, the link was weaker – financial access alone was not enough to erase cultural and social barriers to gender equality.

Women and climate change

It has been well documented that women are more vulnerable to the impacts of climate change than men.

Environmental shocks affect women disproportionately due to a range of factors. These include income disparities, higher rates of displacement and unequal access to land.

Financial inequality and barriers to economic resources, such as needing internet access to make digital payments, play a key role in climate vulnerability, says Tracy Kajumba. She is director for the Least Developed Countries initiative for Effective Adaptation and Resilience (LIFE-AR) interim secretariat at the International Institute for Environment and Development (IIED).

Kajumba, who was not involved in the study, explains to Carbon Brief:

“Women are on the front line doing farming, planting, harvesting and these things that are all impacted [by climate change]. If they don’t have the income to invest either in drought-resistant crops or water-saving technologies, it becomes difficult for households to adapt.”

Calculating climate resilience

The new study measures the impact of financial inclusion on women’s empowerment and, in turn, on climate resilience.

It evaluates a household’s ability to withstand and recover from “shocks and stressors” by using a UN Food and Agriculture Organization metric for “resilience index measurement and analysis” (RIMA).

For example, questionnaires are used to gather information about households in certain areas. The data is then used, together with key indicators, to quantify a household’s resilience to food insecurity, climate variability and economic crisis, amongst other risks.

The 25,511 households surveyed across sub-Saharan Africa were found to be relatively resilient overall and had a high capacity to bounce back from climate shocks. However, they had much lower ability to adapt, in order to build protective capacity in advance of extreme events.

In addition, the study finds that women’s financial empowerment had a positive impact on a household’s ability to “absorb” a climate shock, suggesting that financial access is critical for responding to climate change.

Increased empowerment through financial access enables women to make decisions about planting crops, to access credit in emergencies and to buy or sell food at a better price, the study notes.

For example, it says increased financial access and women’s empowerment help households to deal with the immediate consequences of an extreme weather event, such as a drought. This could be through building community mutual-support networks and by enabling access to savings, to keep the household running.

Anaisie says the study shows women’s empowerment has a significant impact on climate resilience. He tells Carbon Brief:

“If we include women in the financial system, in the case of any climate issue they can save, they can be independent, they can rely on investment to absorb these shocks. This empowerment will help them to be more resilient to climate shocks…We can make progress because SDG goals are all about inclusiveness. It’s all about inclusive growth.”

However, the study notes that financial access does not necessarily create long-term change, which would make the household less vulnerable to extreme weather in the first place.

The authors suggest that lasting structural and cultural change is important for bringing about long-term resilience. They say that policies to address gender inequalities would help bring this about.

They say such policies could include gender-sensitive agricultural credit schemes, subsidised climate insurance for women farmers in drought-prone regions, joint land-titling programmes and quotas for women in local climate-adaptation committees.

Such policies would have helped women impacted by recent severe floods in Ghana to protect their savings, Anaisie explains. He tells Carbon Brief:

“Women are engaged in economic activities, especially informal activities. They have resources and money, but when the flood came in, many women lost that. If they had access to insurance, this flood wouldn’t have cost them that much.

“So, if the government comes out with financial initiatives, training, civic education and gender-focused initiatives, leadership training, women will be empowered and this will translate into their resilience with regards to climate change.”

Addressing climate vulnerability in sub-Saharan Africa

The study could have policy implications for sub-Saharan Africa, a region particularly vulnerable to the effects of climate change. The region faces increasingly extreme weather, heatwaves, droughts, wildfires and floods, as well as food scarcity and threats to crops.

The study suggests that policies to address structural and cultural barriers to women’s financial autonomy could be a key way to build climate resilience across the region.

However, it recognises that even where financial access is expanded, gender norms and cultural constraints continue to shape women’s social empowerment. This, in turn, affects their ability to adapt to climate change in the long term.

Ultimately, addressing structural inequalities is needed to minimise climate vulnerability, says Kajumba. She adds that supporting adaptation with financial access can allow households to absorb shocks without falling into poverty – and to rebuild after climate impacts.

Kajumba says that supporting adaptation with women’s financial access can allow households to absorb shocks without falling into poverty – and to rebuild after climate impacts. She adds:

“When they are supported [with] microloans, savings and all that, you will see change in income, change in households, change in health and education for the children as well.”

However, Kajumba notes that structural inequalities still “amplify” women’s vulnerability to climate impacts and make it harder for them to exercise agency and leadership. She adds:

“The tools that are being used are not always favourable for women…When we look at women in leadership and participation, you cannot lead or you cannot participate unless you have some level of income.”

The post Access to finance ‘strengthens climate resilience’ among sub-Saharan women appeared first on Carbon Brief.

Access to finance ‘strengthens climate resilience’ among sub-Saharan women

As 2026 passes its halfway point, the world is watching one of the most rapidly intensifying El Niño events in the modern record take shape in the tropical Pacific.

The developing El Niño is boosting expectations for global temperatures, both this year and next.

El Niño is the warm phase of a recurring climate pattern in the tropical Pacific that releases heat from the ocean into the atmosphere, temporarily raising global temperatures and reshaping rainfall and extreme weather around the world.

Carbon Brief’s “state of the climate” report in April gave 2026 a 19% chance of setting a new global temperature record.

That chance now stands at 35% – a near-doubling in four months – with virtually all of the change driven by ever-stronger El Niño forecasts.

The key findings from the first half of 2026 include:

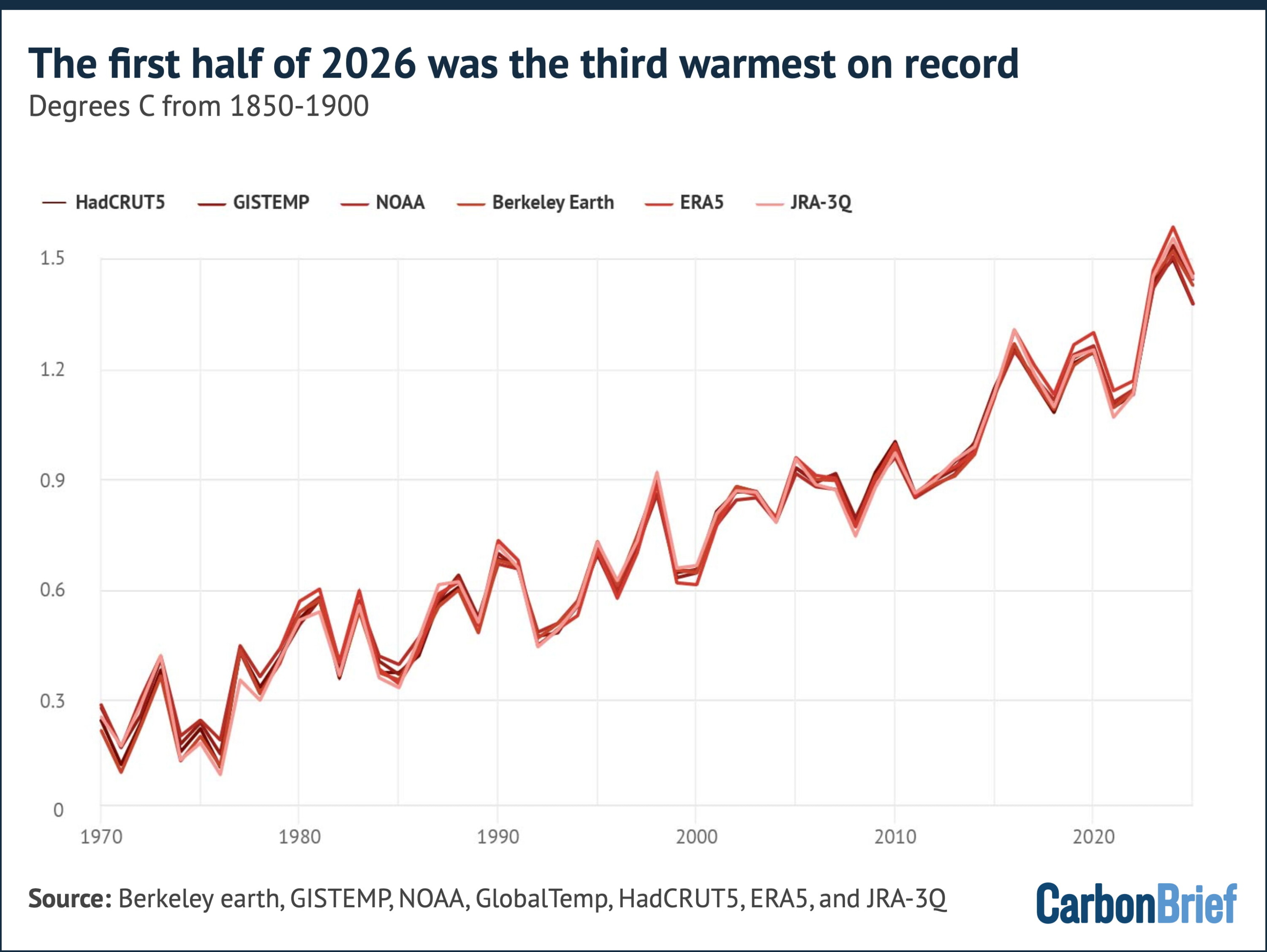

- The first six months of 2026 were the third-warmest start to a year on record – around 1.4C above pre-industrial levels – behind only 2024 and 2025.

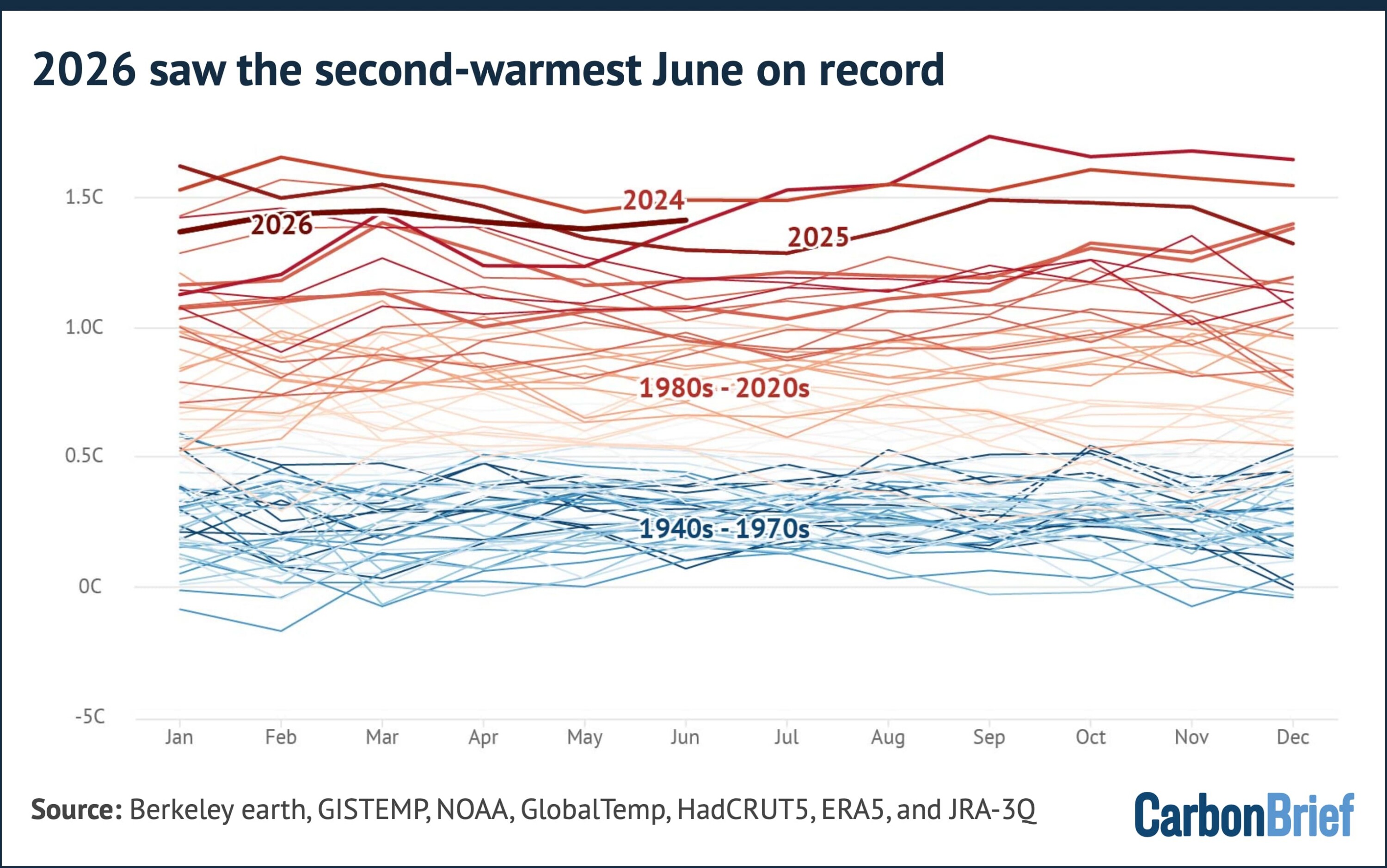

- While the first few months of the year came in as the fourth or fifth warmest, both May and June were the second-warmest ever recorded as El Niño conditions took hold.

- El Niño conditions arrived in April and reached the threshold for a “strong” event by June, when the Niño3.4 index reached 1.6C. Of the 667 model runs Carbon Brief examined, 91% project a peak later this year that is above the strongest El Niño in history.

- The chance that 2026 beats 2024 as the warmest year on record has risen to 35%. Carbon Brief’s central estimate remains that 2026 will be the second-warmest year, at around 1.51C above pre-industrial levels.

- Whether 2026 sets a record will depend on the dataset: the odds range from around two-in-three in NASA and Berkeley Earth data to around two-in-10 in ERA5 and one-in-10 in the JRA-3Q reanalyses.

- June 2026 was western Europe’s hottest June on record, amid a heatwave that set hundreds of individual records. Nearly 9% of the world’s surface saw record June warmth.

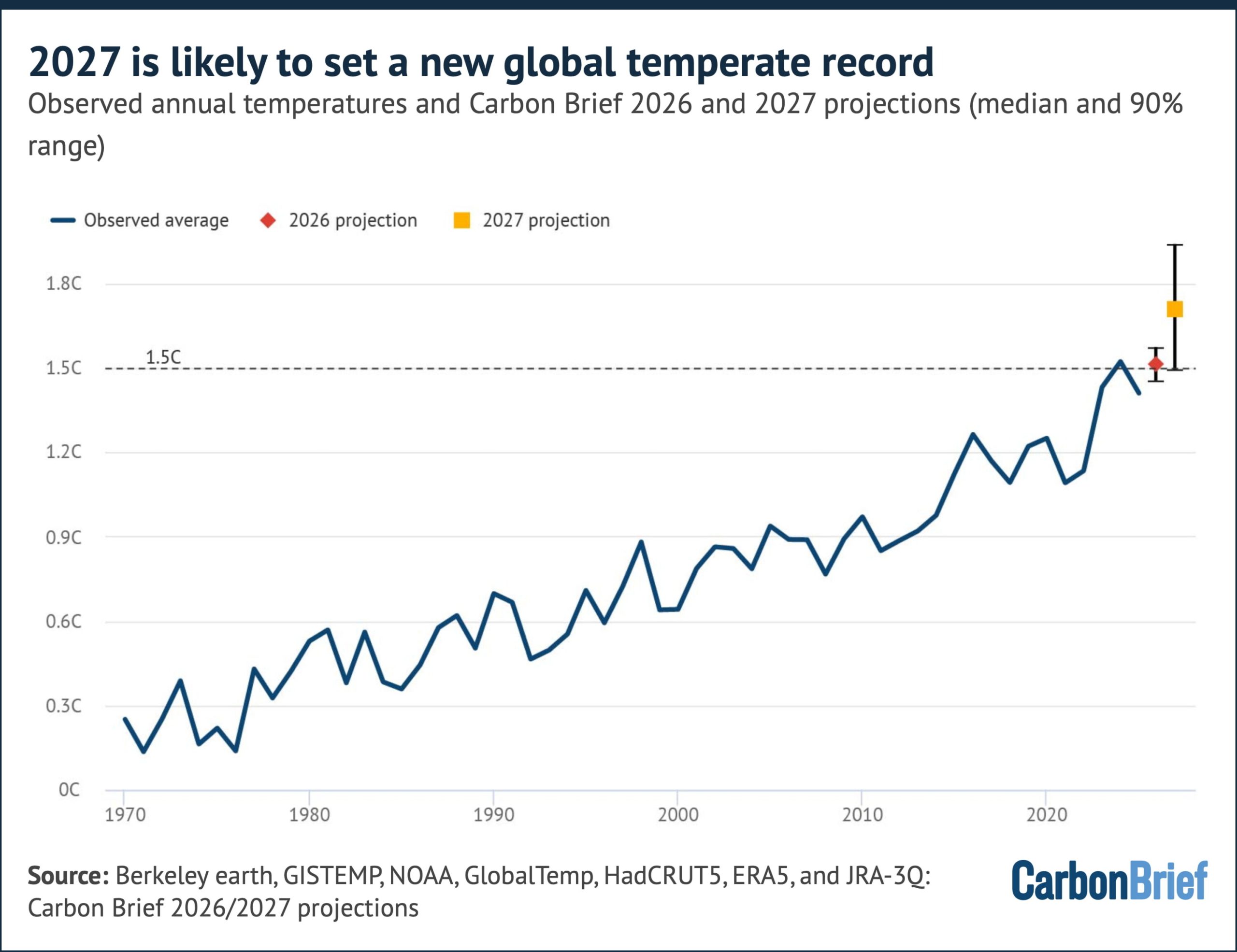

- The developing El Niño will have its largest impact on 2027, which Carbon Brief projects to be around 1.7C above pre-industrial levels – this would comfortably set a new record for the warmest year.

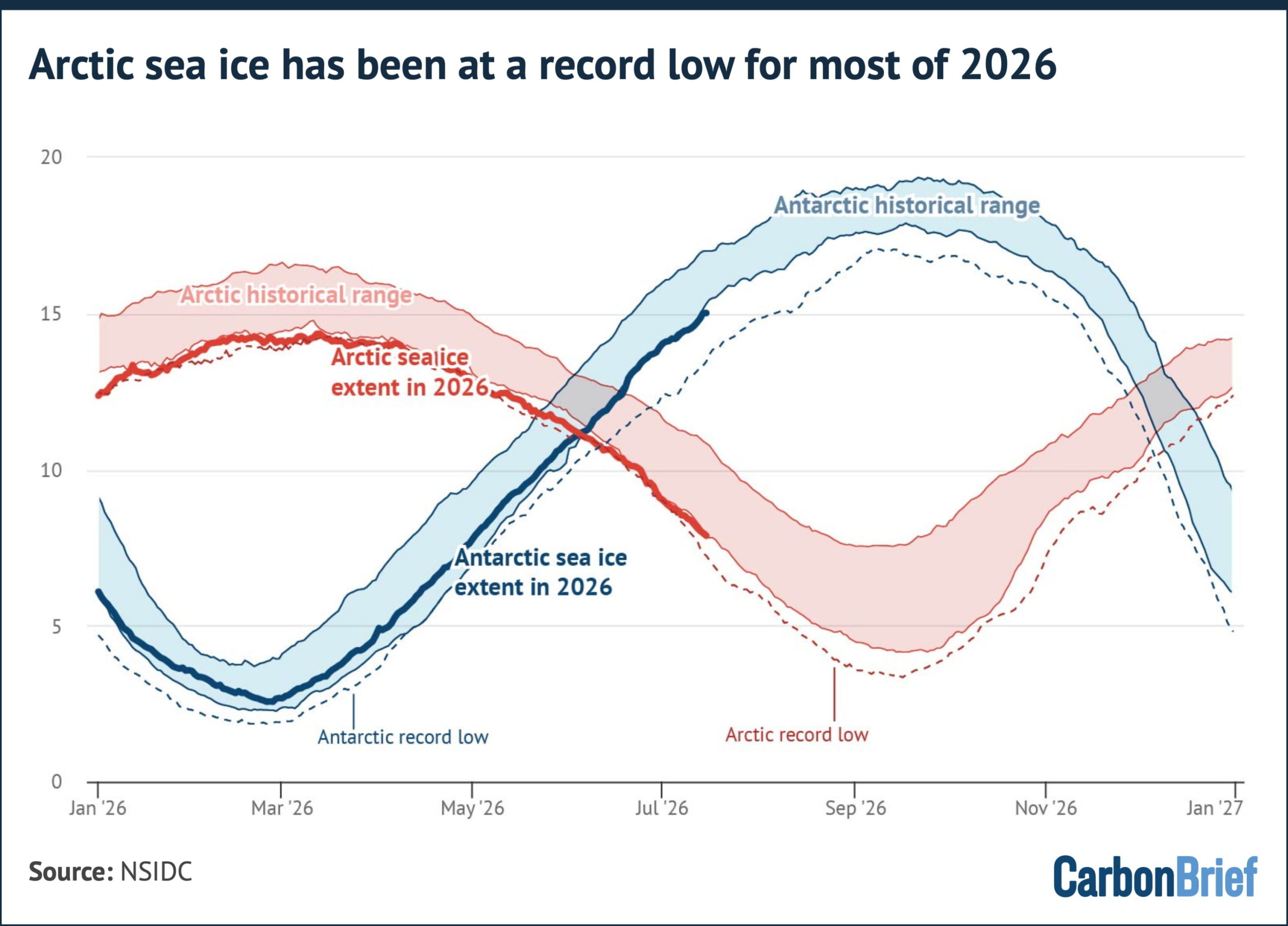

- Arctic sea ice has spent 39 days of 2026 so far at, or below, record daily lows following its joint-lowest winter maximum in the satellite era.

Third-warmest start to a year

Carbon Brief analyses records from six different groups that report global surface temperatures: NASA GISTEMP, NOAA GlobalTemp, Hadley/UEA HadCRUT5, Berkeley Earth, Copernicus/ECMWF ERA5 and the JMA JRA-3Q reanalysis.

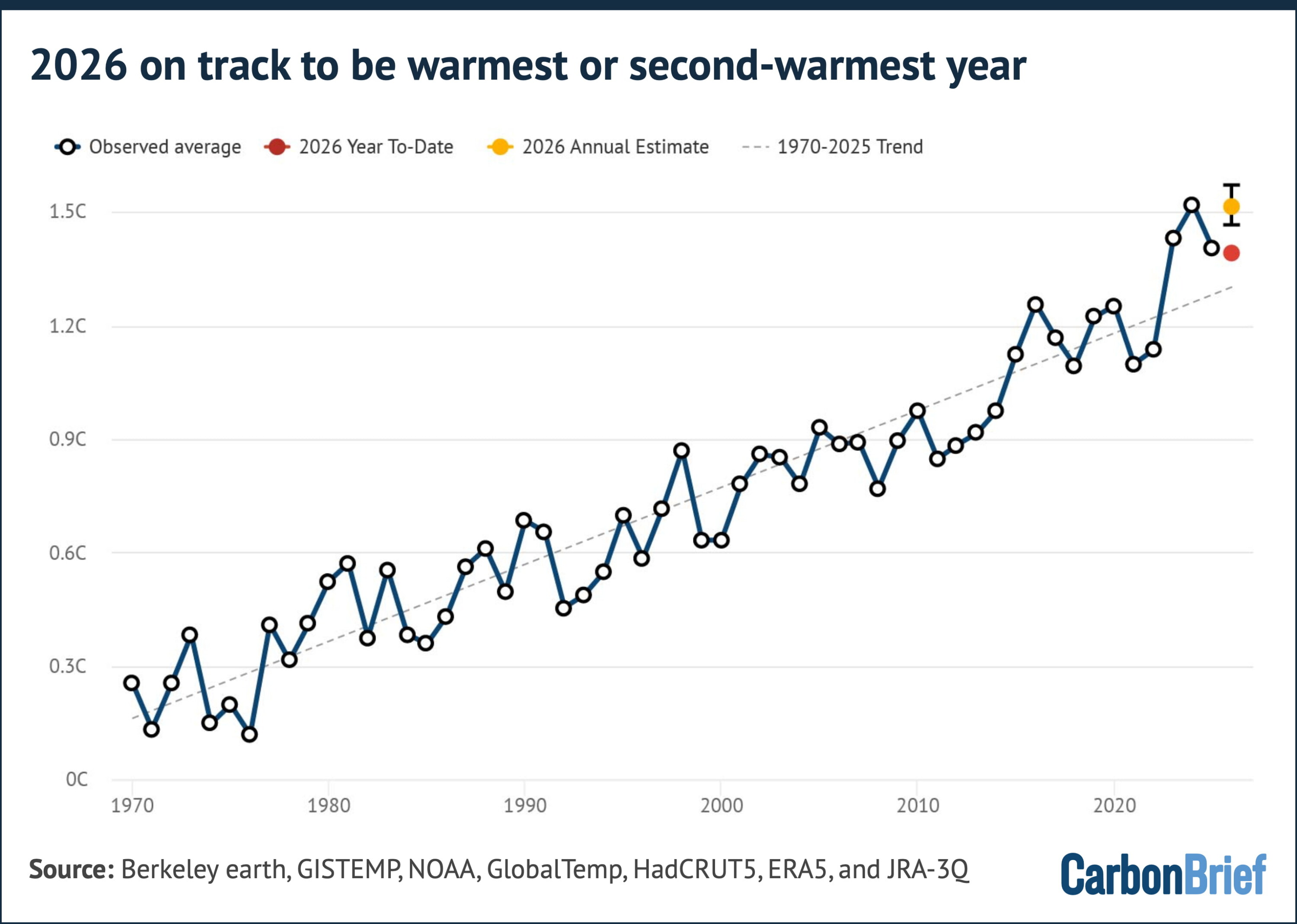

The first half of 2026 was the third warmest on record in every one of the six datasets, behind only 2024 and 2025. The figure below shows annual temperatures since 1970, along with the 2026 year-to-date average (January-June) for each group.

January 2026 was only the fourth- or fifth-warmest January on record, as lingering weak La Niña conditions suppressed temperatures. Since then, each month has climbed the rankings.

La Niña is the cool phase of the El Niño-Southern Oscillation (ENSO). It typically brings wetter conditions to Australia, Indonesia and equatorial South America and drier conditions to the southern US.

March was second-to-fourth warmest across datasets, April the third and both May and June were the second warmest ever recorded, behind only the corresponding months of 2024.

The chart below shows how June 2026 (thick red line) came in around 0.08C below the June record set in 2024 in the average of the six datasets.

Meanwhile, Copernicus reported that global sea surface temperatures over the ice-free oceans set a new June record.

A record-breaking El Niño

ENSO is the largest source of year-to-year variability in global temperatures.

The most common way to assess the strength of an El Niño or La Niña event is by looking at the sea surface temperature anomaly in the “Niño3.4” region of the tropical Pacific.

El Niño and its sister La Niña occur when temperatures in the tropical Pacific are more than 0.5C (El Niño) or less than 0.5C (La Niña) below normal, where normal is defined by removing the effects of long-term climate change.

The thresholds for defining the strength of an El Niño or La Niña are above/below 1C for “moderate” events, 1.5C for “strong” events and 2C for “very strong” (or “super”) events.

After two years dominated by La Niña conditions, the tropical Pacific flipped decisively in April when the Niño3.4 index crossed the 0.5C El Niño threshold. It subsequently reached 1C in May and hit 1.6C in June, marking one of the fastest onsets in the observational record.

In the first few weeks of July, the index shot above 2C, significantly outpacing the speed at which any prior El Niño events developed.

Forecast models expect even more to come.

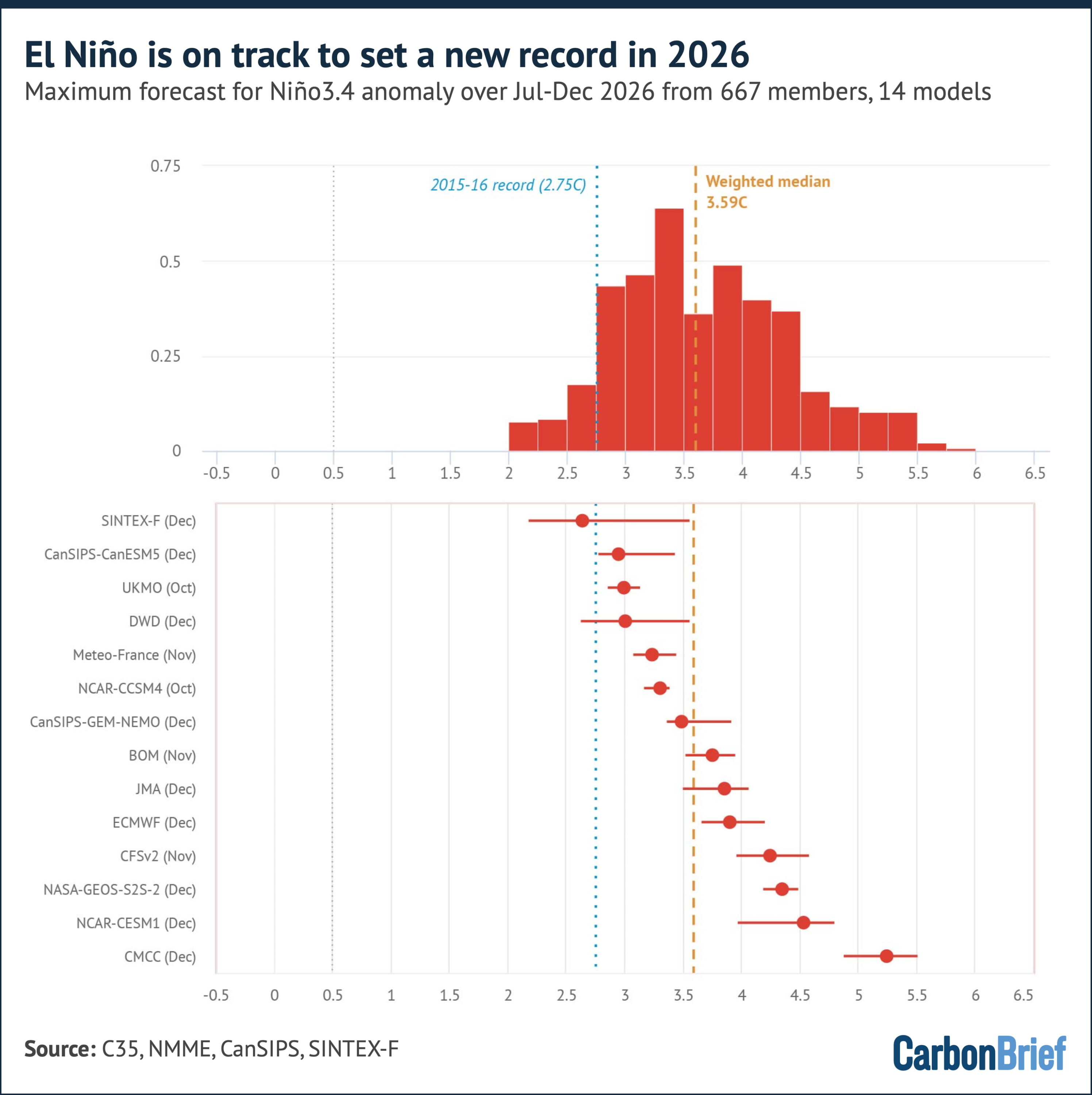

An analysis by Carbon Brief of the median of 667 model runs from 14 different modelling groups suggests that sea surface temperatures in theNiño3.4 region could peak at 3.59C between July and December.

More than 91% of runs predict the strongest El Niño event in the modern record. The previous record was set during the event of 2015-16, when temperatures peaked around 2.75C.

This is shown in the chart below, which features a histogram of the likelihood of different possible 2026 El Niño peaks across all the models on the top. The forest plot beneath shows the best estimate and range of outcomes predicted by each individual model.

The median forecast in every one of the 14 models suggests a peak that exceeds the 2C “super” El Niño threshold, with most models peaking in November or December.

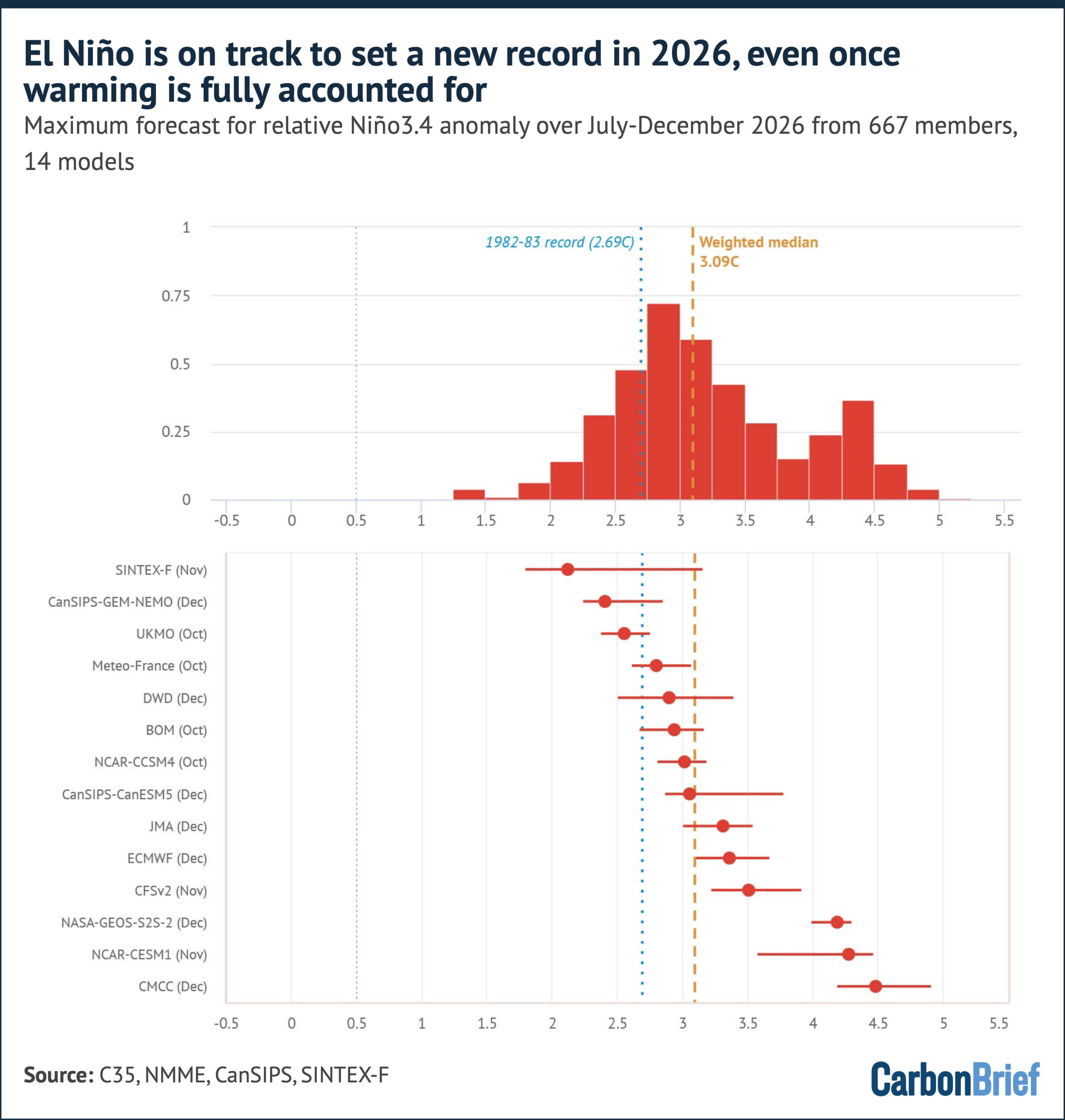

Some caution here is warranted, however. Raw model Niño3.4 anomalies are measured against a fixed climatology. Because the entire tropical ocean has warmed due to human-caused greenhouse gas emissions, the models tend to overstate event strength relative to the historical record.

A cleaner comparison uses the relative Niño3.4 index (RONI), which subtracts the average tropical ocean warming.

This relative measure suggests the median forecast peak for El Niño in the latter half of 2026 is 3.1C. The prior record stands at a lower 2.69C, set in 1982-83.

Nevertheless, 77% of model runs still show a new record event occurring. This is shown in the chart below.

In summary, on both indexes, the central expectation is now for the strongest El Niño in the observational record.

Model forecasts made in the spring and early summer have historically shown some bias toward overpredicting event strength. However, forecasts made after the spring are considerably more reliable.

Widespread record warmth and a massive European heatwave

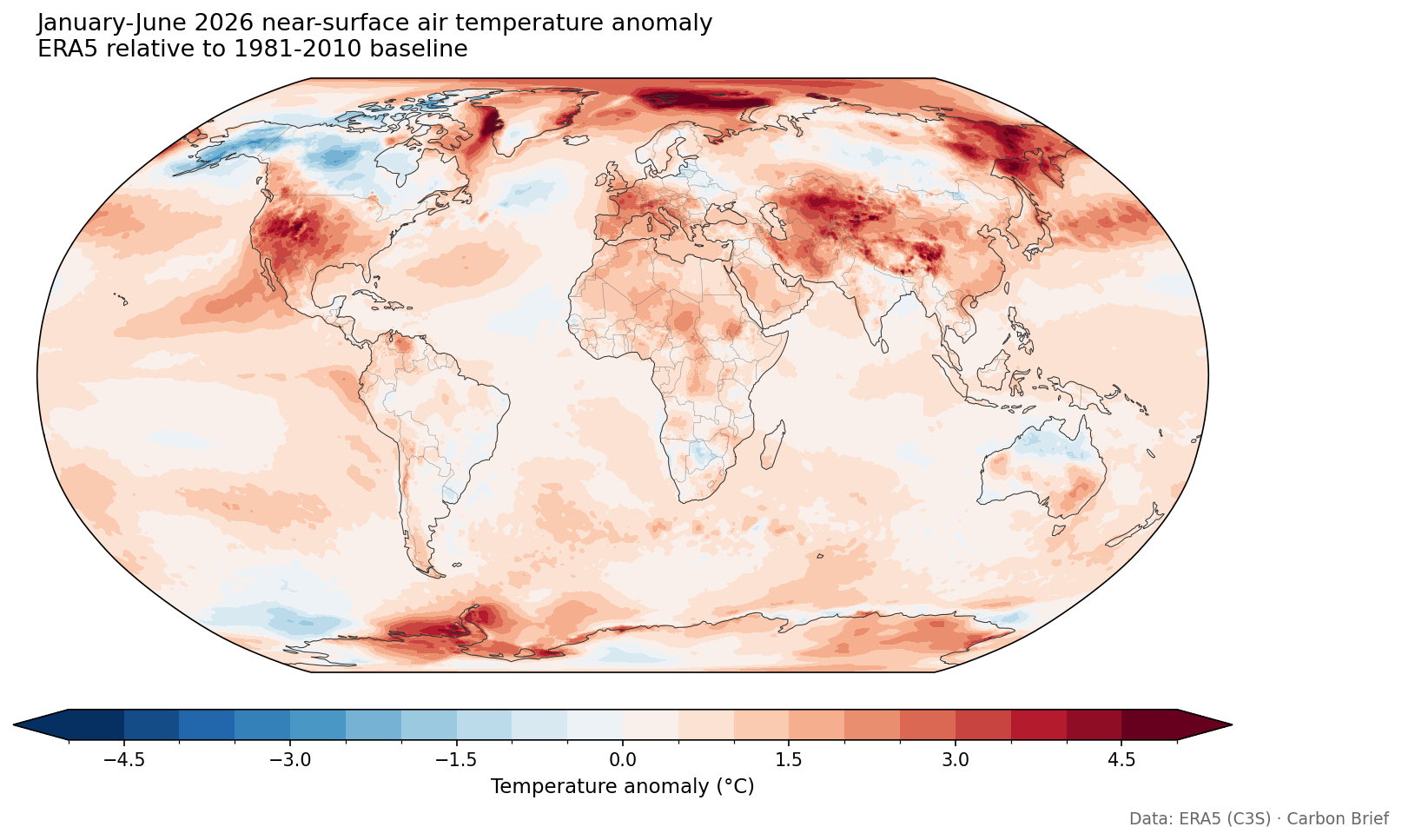

The map below shows the temperature anomaly for the first half of 2026 in the ERA5 dataset, relative to a 1981-2010 baseline period.

It shows how the largest warm anomalies were found across the Arctic – particularly north of Scandinavia and Svalbard – as well as western Europe, the western US, northern Mexico, central Asia, western China, eastern Russia and the Antarctic Peninsula region.

The developing El Niño is clearly visible as a tongue of warm anomalies stretching along the equatorial eastern Pacific. Only a few regions – central Canada, Alaska and parts of the Southern Ocean – saw temperatures below the 1981-2010 average.

Where 2026 ranks against history is even more striking. The map below shows where the period of January-June 2026 ranked among all 87 years in the ERA5 record, which stretches from 1940 to 2026. Grid cells marked in red saw temperatures in the first half of the year that were in the top-five warmest years.

More than 30% of the global surface had a top-five warmest start to the year and 7.1% saw its warmest on record, including much of western Europe, the eastern equatorial Pacific and the seas around Japan.

Not a single grid cell had a top-five coolest start to the year. In June alone, 8.9% of the world’s surface saw record warmth for the month. This is illustrated in the map below, where grid cells marked in red saw temperatures that were in the top-five warmest years and grid cells in blue in the top-five coolest.

The standout regional temperature event was a heatwave that struck Europe in late June.

Western Europe had its hottest June on record, recording an average temperature of 3.05C above the 1991-2020 average and beating the record set only a year earlier, according to Copernicus. A heat dome over 22-30 June broke 10 all-time national heat records and around 400 long-record station records.

France set a new June national record of 44.3C, while the UK broke its June record on three consecutive days, reaching 37.3C. The humid heat drove a death toll estimated in the thousands.

A separate heat dome also brought record June temperatures to parts of North America in late June.

On track to be second warmest, but a real chance at first

Carbon Brief’s updated projection for 2026 as a whole combines the observed January-June temperatures with the latest El Niño forecast. It uses a statistical model trained on the historical relationship between the first half of the year, ENSO conditions and annual temperatures observed over 1950-2025, excluding major volcanic eruption years.

Carbon Brief estimates that 2026 will be around 1.51C above pre-industrial levels, with a 90% range of 1.45C to 1.57C, shown by the yellow dot in the chart below.

This is up from 1.47C in the projection set out in April – and is notably more certain now that half the year has passed.

This central estimate would make 2026 the second-warmest year on record, just below 2024 (1.52C) and ahead of 2023 (1.43C) and 2025 (1.41C).

Carbon Brief’s modelling puts the chance that 2026 beats 2024 as the warmest year on record at 35%, using the average of the six different surface temperature records assessed. It puts the chance that 2026 comes in above 1.5C at around 63%.

If it does, 2026 would be the second calendar year – after 2024 – where warming averaged above 1.5C, in a further sign that the world is rapidly approaching the Paris Agreement’s 1.5C limit.

A single year above 1.5C does not by itself constitute a breach of the goal, which refers to the longer term average temperature of the planet. This is defined as the midpoint of a 20-year period by the Intergovernmental Panel on Climate Change (IPCC).

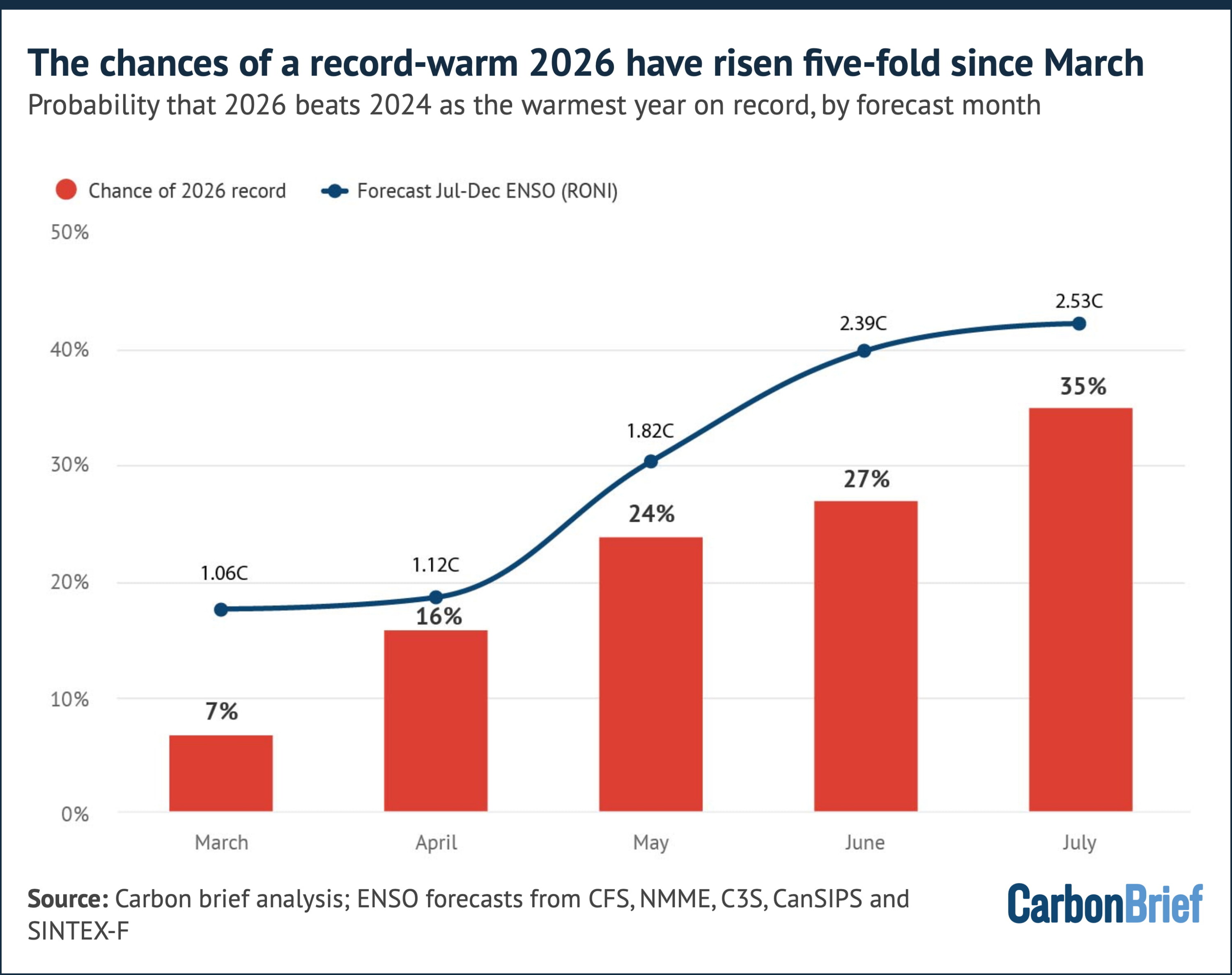

These likelihood of a record have been climbing rapidly throughout 2026.

Global temperatures so far throughout the year have run well below the record-setting levels of 2024 – around 0.13C cooler over the first six months.

On their own, temperatures observed so far in 2026 would make a new annual record unlikely.

However, rerunning the projection using only the data available at the end of each month since March – including both the year-to-date observations and the El Niño forecast issued that month – shows a shifting picture.

Using March data, 2026 had just a 7% chance of setting a new record. That rose to 16% in April, 24% in May, 27% in June and 35% using the latest data in mid-July.

This is shown in the chart below.

Notably, this rise has little to do with observed temperatures. The year-to-date anomaly has actually drifted slightly down, from 1.41C after March to 1.39C after June.

Observed temperatures and fewer remaining months of the year contributed only around four percentage points of the 28-point rise in the likelihood; the remaining ~84% of the change comes from successive upward revisions to the El Niño forecast for late 2026.

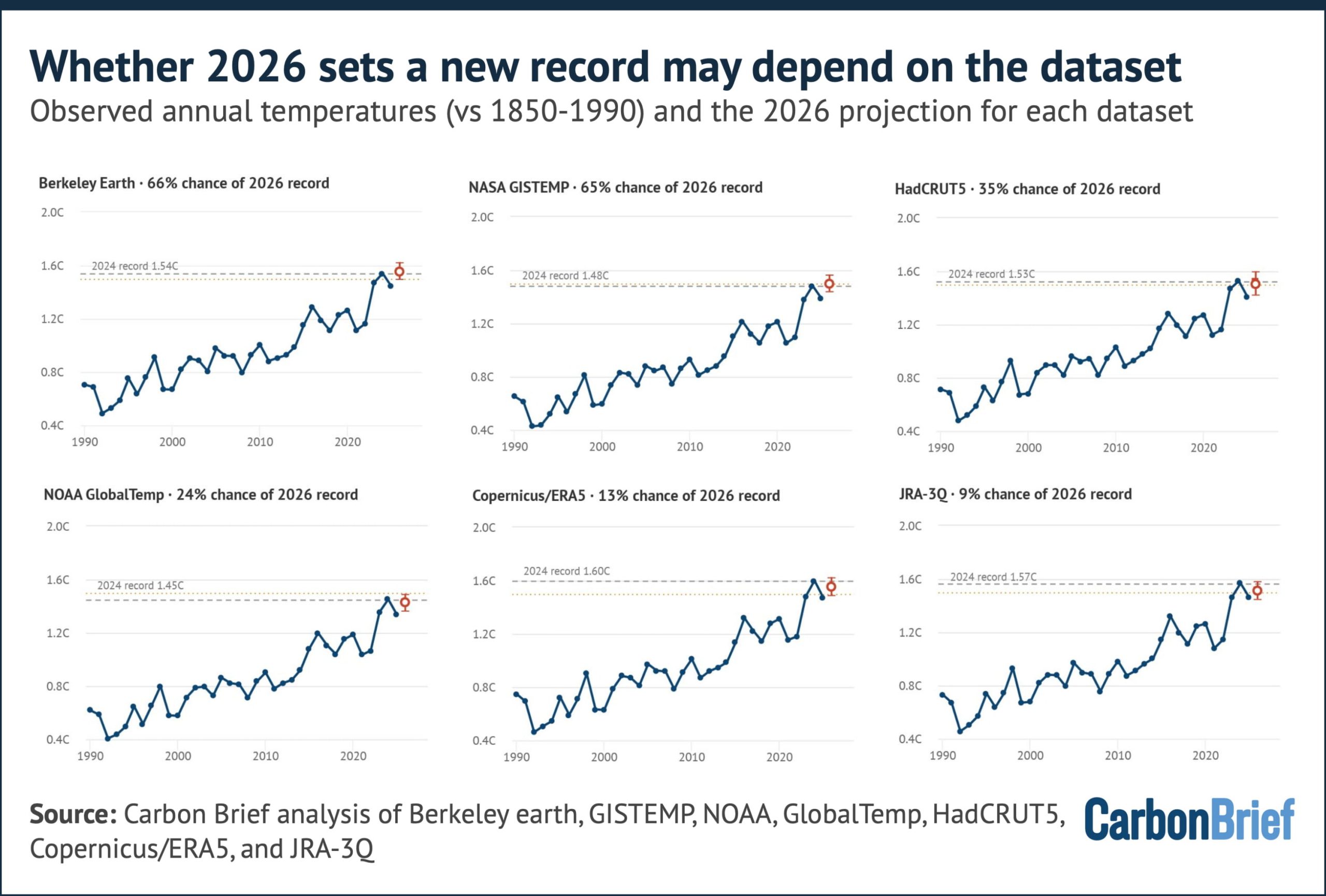

However, whether 2026 ends up becoming the warmest year on record may end up depending on which dataset is used.

Running the same projection gives odds of a 2026 record of around two-in-three for Berkeley Earth (66%) and NASA GISTEMP (65%), but only 35% for HadCRUT5, 24% for NOAA and just 13% and 9% for the ERA5 and JRA-3Q reanalyses, respectively.

This is shown below.

The divergence between projections mostly reflects how exceptional each dataset’s 2024 was.

The reanalysis approaches recorded a particularly warm 2024, leaving 2026 more ground to make up. GISTEMP and Berkeley, on the other hand, project 2026 modestly above their 2024 values.

A repeat of the situation in 2015 where different groups disagreed on record rankings is a real possibility. Headlines in January 2027 may hinge on choices of dataset.

2027 likely to be the warmest year in human history

The biggest climate story of the developing super El Niño may not be 2026 at all.

Global temperatures typically lag in the tropical Pacific by around three months. So, an El Niño event peaking in November and December 2026 will have its largest warming influence on 2027.

We saw this same pattern occur in 1997-98, 2015-16 and 2023-24 – where the year in which the El Niño developed was warm, but the following year was record-smashing.

Carbon Brief has extended its projection into 2027 by using the historical relationship between year-over-year temperature changes and ENSO conditions in the preceding autumn.

This yields a best estimate for 2027 of around 1.71C above pre-industrial levels, with a 90% range of 1.49C to 1.93C. This is shown by a yellow square on the chart below.

That would give 2027 a 92% chance of setting a new global temperature record and a 94% chance of exceeding 1.5C.

Taking 2026 and 2027 together, there is a 93% chance that at least one of the two years sets a new record.

The 2027 estimate is more uncertain than the 2026 one. As with 2026, there are uncertainties in the projection due to unknowns around exactly how strong the El Niño peak proves to be and how quickly it decays.

However, even the low end of the 2027 range would put it among the warmest years on record and the central estimate of 1.71C would exceed 2024 by nearly 0.2C.

If these projections bear out, the 2020s will have delivered new global temperature records in 2023, 2024 and 2027 – and potentially 2026 too – with a number of individual years well above the 1.5C threshold.

The long-term warming trend, driven by human emissions of carbon dioxide and other greenhouse gases, has increased from around 0.18C per decade in the early 2000s to around 0.27C per decade today. El Niño and La Niña play a big role in determining which years along that rising path stand out as records.

Arctic sea ice at record lows

Arctic sea ice has spent much of 2026 in record-low territory.

Following the joint-lowest winter maximum in the satellite record in mid-March, daily extent has set or tied record lows for the date on 39 days so far this year, including extended spells in mid-to-late March and in early-to-mid June.

The most recent record-low days were in early July.

The chart below shows how Arctic sea ice in 2026 (dark red line) has been below the historical range (shaded red).

It also shows how Antarctic sea ice (dark blue), meanwhile, has remained below the 1979-2010 range for almost all of 2026 to date.

As of mid-July, Arctic extent is a bit below the 1979-2010 historical range for the date, though it remains around 0.6m square kilometres (km2) larger than the record low for the date set during 2020’s exceptional summer melt season.

The trajectory over the coming two months will determine whether 2026 challenges 2012’s record September minimum. Early-summer conditions are a poor predictor of the September minimum, which depends heavily on summer weather.

Antarctic sea ice, meanwhile, is currently around 300,000km2 below the historical envelope, but has stayed well clear of the record lows set in 2023 and has not set any new daily records yet this year.

Q&A: Europe’s May and June heatwave deaths – and how they were counted

Guest post: France’s June heatwave caused more than 2,700 heat-related deaths

Guest post: Climate change has caused one-fifth of Pine Island glacier retreat

Media reaction: How climate change intensified Europe’s record-breaking June heat

The post State of the climate: Rapidly developing El Niño raises chance of record-warm 2026 appeared first on Carbon Brief.

State of the climate: Rapidly developing El Niño raises chance of record-warm 2026

-

Greenhouse Gases12 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Climate Change12 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Renewable Energy9 months ago

Renewable Energy9 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Greenhouse Gases1 year ago

嘉宾来稿:探究火山喷发如何影响气候预测