Disseminated on behalf of Surge Battery Metals Inc.

Electric vehicles (EVs), energy storage systems (BESS), and clean energy technologies depend heavily on lithium. Yet even with fast-rising demand, the United States still produces far less lithium than it needs.

In 2024, U.S. production reached only about 25,000 tonnes of lithium carbonate equivalent (LCE) – roughly 2% of global supply, which totaled around 1.2 million tonnes. That output is enough for only about 158,000 Tesla Model 3 battery packs per year.

The gap between national demand and domestic production keeps widening. Most lithium used in the U.S. comes from imports, mainly from Chile, Australia, and China. This dependency exposes the country to supply disruptions, trade restrictions, and price volatility. If imports are interrupted, the U.S. battery and EV industries could face serious setbacks.

Growing Demand Creates a Structural Deficit

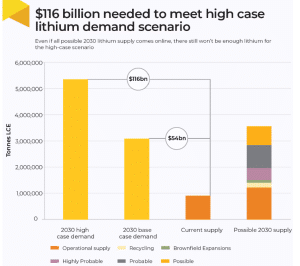

Global demand for lithium is growing quickly. Analysts expect it to quadruple by 2030 as more countries adopt EVs and build large-scale battery storage.

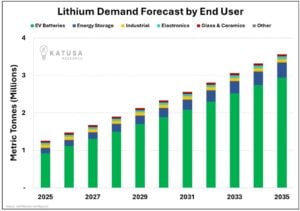

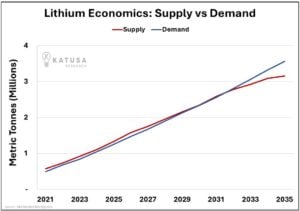

According to Katusa Research (2025), global lithium demand is projected to climb from 1.04 million tonnes in 2024 to 3.56 million tonnes by 2035 — a 3.5× increase. About 83% of that demand will come from EV batteries, while energy storage will account for another 11%.

Source: Katusa Research

Per the International Energy Agency, the U.S. alone may need over 625,000 tonnes of LCE per year by 2030, compared with only a small fraction produced domestically today.

Building new mines takes time – often 10 to 15 years from exploration to commercial production. This long timeline makes it difficult to ramp up supply fast enough to meet demand. Therefore, a lasting shortage is forming. If the U.S. does not accelerate new projects soon, it may depend on imports for decades.

Each EV battery pack uses large amounts of lithium. On average, an EV requires about 60 kilograms of LCE – or 8 to 10 kilograms per kilowatt-hour (kWh) of battery capacity. As automakers build more gigafactories, that adds up quickly.

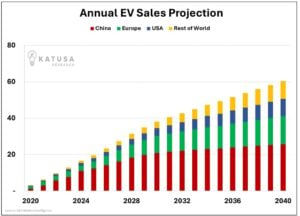

Katusa’s data also shows that global EV sales jumped from 2 million in 2020 to 11 million in 2024, a 450% surge — and could exceed 60 million units per year by 2040, more than half of all cars sold globally.

Source: Katusa Research

The U.S. is expected to have 440 gigawatt-hours (GWh) of battery manufacturing capacity by 2025 and more than 1,000 GWh by 2030. That growth alone could double or triple national lithium demand.

Introducing the Nevada North Lithium Project

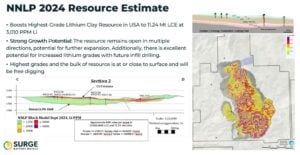

One company aiming to help close this gap is Surge Battery Metals. Its flagship asset, the Nevada North Lithium Project (NNLP) in Elko County, Nevada, is one of the few high-grade lithium clay deposits in the United States.

The project has an inferred resource of 11.24 million tonnes of LCE, grading about 3,010 ppm lithium, making it the highest-grade lithium clay resource in the country.

The project benefits from ideal logistics. NNLP is only 13 kilometers from major power lines and close to all-season roads. The Bureau of Land Management (BLM) has issued a Record of Decision and a Finding of No Significant Impact (FONSI), allowing expanded exploration over 250 acres. These factors make NNLP a leading U.S. candidate for large-scale lithium development.

How NNLP Helps Close the Supply Gap

Surge Battery Metals’ Nevada North project has features that position it well to help close America’s lithium gap. Its high grade and large resource size suggest it could deliver significant output once in production. Higher-grade deposits typically allow lower extraction costs and shorter payback periods.

Because NNLP already has key permits and environmental clearance, it may reach production faster than many early-stage peers. That speed is critical as EV demand accelerates and the U.S. targets more domestic battery manufacturing.

Just as important, NNLP supports U.S. policy goals for supply chain security. Producing lithium domestically reduces reliance on imports, helping stabilize supply and pricing for American automakers. It also supports the Inflation Reduction Act, which requires that most EV battery minerals come from North America or allied countries by 2027.

In March 2025, the U.S. government took direct equity stakes in several lithium ventures, including Lithium Americas’ Thacker Pass, signaling a strong federal commitment to reshoring critical mineral production. This policy backdrop reinforces projects like NNLP as part of a national security priority.

Strengthening NNLP Through Strategic Partnership

Moreover, Surge Battery Metals signed a joint venture letter of intent (LOI) with Evolution Mining (ASX: EVN), allowing Evolution to earn up to 32.5% ownership by funding C$10 million toward the Preliminary Feasibility Study (PFS) for the Nevada North Lithium Project (NNLP). Surge retains majority control and project management, keeping its long-term vision and stakeholder priorities front and center.

This partnership delivers big strategic value. By merging Surge’s lithium expertise and mineral rights with Evolution’s 75% stake in 880 acres of private land – and over 21,000 added acres nearby – the deal significantly increases the JV’s land position. The expanded acreage boosts the overall exploration area and brings in mineral rights in key southern zones, possible clay unit extensions to the north, and territory in historic mining districts and key drainage areas.

Importantly, Evolution’s staged funding speeds up completion of the PFS and helps NNLP reach development milestones while lowering capital risk for Surge shareholders. If Evolution completes its full commitment, it will own 32.5% of the JV, but Surge remains the lead partner. This setup means Surge still directs the project, while using Evolution’s operations know-how and resources. With a larger land package and a joint operating committee, NNLP is well on its way to Tier 1 status and is strengthening its spot in North America’s battery metals supply chain – vital for clean energy and EV growth.

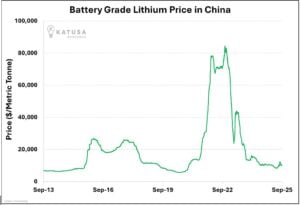

Like any mining venture, NNLP faces challenges. Lithium prices fell nearly 90% from their 2022 peak, but from June to September 2025, they rebounded 24%, showing early signs of recovery.

This cyclical pattern reflects Katusa’s “cost floor” concept — production costs in China and Australia now average around $5,000–6,000 per tonne LCE, while South American and U.S. projects need about $8,000/t to stay profitable. If prices fall near those levels, high-cost mines pause output, tightening supply again and stabilizing prices.

Another factor is resource expansion. NNLP’s current resource is inferred, but the company expects to complete its current drilling program at NNLP by the end of October 2025. Once the results are released, the lithium resource will be upgraded from Inferred to Indicated and Measured categories. This step will strengthen confidence in the deposit’s scale and quality, supporting the upcoming Pre-Feasibility Study (PFS).

Permitting and community engagement also remain important; even in a mining-friendly state like Nevada, water use and land reclamation practices must meet strict environmental standards.

Surge Battery Metals has emphasized sustainable practices, including water recycling and progressive site reclamation, as part of its exploration and development plan.

Competition is growing, too. Lithium projects across South America, Australia, and Canada are advancing quickly. Still, Nevada’s combination of stable governance, established mining laws, and proximity to major battery plants gives U.S. projects like NNLP a strong advantage.

A National View: U.S. Lithium Resources and Reserves

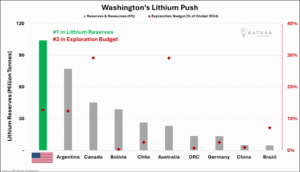

The U.S. is home to some of the world’s largest lithium reserves, but it still underdevelops them. According to the U.S. Geological Survey, global lithium reserves total around 21 million tonnes, with the U.S. holding roughly 12%. Nevada alone hosts the country’s biggest lithium resources, concentrated in the Thacker Pass region and the northern claystone belts – where NNLP is located.

Unlocking these resources is vital. Every new project that moves forward strengthens the domestic supply chain and supports national goals to lead in clean energy technology.

Surge Battery Metals plans to continue advancing NNLP through new drilling campaigns and metallurgical studies in 2025. These programs aim to expand and upgrade resources, optimize extraction processes, and confirm the potential to produce battery-grade lithium carbonate with 99.9% purity. The company is also evaluating potential offtake partnerships with battery and automotive manufacturers.

Analysts and investors will be watching for:

Updated resource estimates and grade expansion

Progress toward pre-feasibility studies

Partnerships or funding deals with strategic investors

Regulatory updates supporting U.S. critical mineral development

Positive results in these areas could accelerate NNLP’s move toward construction and help it become one of the first next-generation lithium clay projects to enter U.S. production.

Powering the U.S. Energy Future

The U.S. faces a widening gap between lithium supply and demand that could slow its clean-energy transition. Katusa Research projects a 400,000-tonne global supply shortfall by 2035, roughly the world’s entire 2020 output – a deficit that could keep prices elevated long term.

Source: Katusa Research

Surge Battery Metals’ Nevada North Lithium Project provides a realistic and timely opportunity to help close that divide. With its high-grade resource, strong economics, strategic location, and environmental focus, NNLP could play a central role in building a stable, self-sufficient lithium supply for the United States.

As the nation races to electrify transportation and decarbonize energy, projects like NNLP will be critical. They are not only about producing lithium – they are about powering the next chapter of American industry and ensuring that the clean-energy future is built on secure, sustainable ground.

New Era Publishing Inc. and/or CarbonCredits.com (“We” or “Us”) are not securities dealers or brokers, investment advisers, or financial advisers, and you should not rely on the information herein as investment advice. Surge Battery Metals Inc. (“Company”) made a one-time payment of $50,000 to provide marketing services for a term of two months. None of the owners, members, directors, or employees of New Era Publishing Inc. and/or CarbonCredits.com currently hold, or have any beneficial ownership in, any shares, stocks, or options of the companies mentioned.

This article is informational only and is solely for use by prospective investors in determining whether to seek additional information. It does not constitute an offer to sell or a solicitation of an offer to buy any securities. Examples that we provide of share price increases pertaining to a particular issuer from one referenced date to another represent arbitrarily chosen time periods and are no indication whatsoever of future stock prices for that issuer and are of no predictive value.

Our stock profiles are intended to highlight certain companies for your further investigation; they are not stock recommendations or an offer or sale of the referenced securities. The securities issued by the companies we profile should be considered high-risk; if you do invest despite these warnings, you may lose your entire investment. Please do your own research before investing, including reviewing the companies’ SEDAR+ and SEC filings, press releases, and risk disclosures.

It is our policy that information contained in this profile was provided by the company, extracted from SEDAR+ and SEC filings, company websites, and other publicly available sources. We believe the sources and information are accurate and reliable but we cannot guarantee them.

CAUTIONARY STATEMENT AND FORWARD-LOOKING INFORMATION

Certain statements contained in this news release may constitute “forward-looking information” within the meaning of applicable securities laws. Forward-looking information generally can be identified by words such as “anticipate,” “expect,” “estimate,” “forecast,” “plan,” and similar expressions suggesting future outcomes or events. Forward-looking information is based on current expectations of management; however, it is subject to known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those anticipated.

These factors include, without limitation, statements relating to the Company’s exploration and development plans, the potential of its mineral projects, financing activities, regulatory approvals, market conditions, and future objectives. Forward-looking information involves numerous risks and uncertainties and actual results might differ materially from results suggested in any forward-looking information. These risks and uncertainties include, among other things, market volatility, the state of financial markets for the Company’s securities, fluctuations in commodity prices, operational challenges, and changes in business plans.

Forward-looking information is based on several key expectations and assumptions, including, without limitation, that the Company will continue with its stated business objectives and will be able to raise additional capital as required. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated, or intended.

There can be no assurance that such forward-looking information will prove to be accurate, as actual results and future events could differ materially. Accordingly, readers should not place undue reliance on forward-looking information. Additional information about risks and uncertainties is contained in the Company’s management’s discussion and analysis and annual information form for the year ended December 31, 2024, copies of which are available on SEDAR+ at www.sedarplus.ca.

The forward-looking information contained herein is expressly qualified in its entirety by this cautionary statement. Forward-looking information reflects management’s current beliefs and is based on information currently available to the Company. The forward-looking information is made as of the date of this news release, and the Company assumes no obligation to update or revise such information to reflect new events or circumstances except as may be required by applicable law.

For more information on the Company, investors should review the Company’s continuous disclosure filings available on SEDAR+ at www.sedarplus.ca.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: None.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

Google, Meta, and McKinsey & Company have made a major move in corporate climate action. They signed a long-term deal to remove carbon from the air in Appalachia. The project is run by Living Carbon and focuses on restoring forests on degraded lands. Under this deal, the companies will remove 131,240 tonnes of CO₂ over the next ten years.

A New Deal for Climate

The effort targets a much larger problem. Across the United States, about 1.6 million acres of abandoned mine land remain damaged by past mining. These lands often have poor soil, erosion, toxic metals, and invasive species that block natural regrowth.

In addition, around 30 million acres of degraded agricultural land could be restored through reforestation. Appalachia is one of the hardest-hit regions due to decades of coal mining.

The deal is backed by the Symbiosis Coalition, a group of buyers that funds high-quality carbon removal projects. The coalition is an advance market commitment (AMC) launched in 2024 by Google, Meta, Microsoft, and Salesforce.

The group has pledged to contract up to 20 million tonnes of carbon removal credits by 2030. This commitment aims to create strong market demand and support the growth of high-impact, science-based restoration projects that can help advance global climate goals.

The agreements they have give developers a steady demand. They also help unlock financing and allow projects to scale.

Symbiosis selected the Appalachian project after a strict review process. It looked at data, field conditions, and long-term risks. The group follows key standards such as durability, transparency, ecological integrity, and community impact. This helps ensure that every credit represents real and measurable carbon removal.

Source: Symbiosis

Julia Strong, Executive Director of the Symbiosis Coalition, remarked:

“Our support of Living Carbon reflects our belief that effective nature-based carbon removal requires both strong science and solid execution. Their project stands out for its rigor and for its thoughtful and scalable approach shaped around the needs of local communities, ecosystems, and economies in Appalachia.”

Why Appalachia Matters: From Coal Hubs to Carbon Heroes

The Appalachia region, in the eastern United States, was once a center of coal mining. Today, many of these lands remain unused and degraded. Living Carbon is working to restore them by planting native hardwood and pine trees on former mine sites and damaged farmland.

The project uses a mix of careful site preparation, invasive species control, and strategic planting. This helps trees grow in areas where nature cannot easily recover on its own. The goal is not just to plant trees, but to rebuild entire ecosystems and support long-term carbon storage.

The benefits go beyond carbon removal. Restoring forests improves soil health, water quality, and biodiversity. Native trees help rebuild habitats for local plants and wildlife. These changes can also reduce erosion and improve land stability over time.

The project also creates real economic value. Landowners earn lease payments from land that was once unproductive. Local workers are hired for planting and land restoration.

In some cases, old mining equipment is reused to support ecological recovery. This helps turn former industrial sites into productive carbon sinks.

Community engagement is a key part of the project. Living Carbon works closely with landowners, local groups, and government agencies. This helps build long-term support and ensures the project fits local needs. Strong local partnerships also improve the chances that the forests will be maintained over time.

The project stands out for its strong science and clear execution plan. It uses careful monitoring and conservative estimates to ensure carbon removal is real. It also applies new methods for tracking results, including advanced baselines and lifecycle analysis.

This type of approach shows that high-quality nature-based carbon removal can deliver more than climate impact. It can restore ecosystems, support local economies, and scale across similar regions. In places like Appalachia, it offers a way to turn damaged land into a long-term climate solution.

More corporations are now buying carbon removal credits to meet climate goals. For example, Microsoft bought 45 million tonnes of carbon removal in fiscal year 2025. This is nearly double the amount from 2024 and nine times what they bought in 2023.

These purchases are part of a broader climate strategy. Companies are combining emissions reductions with long-term removal commitments. Durable carbon removal credits, which permanently store CO₂, are becoming more important. Businesses feel pressure to deal with emissions that they cannot completely eliminate.

A major supporter of these deals is Frontier, launched in 2022 by Stripe, Alphabet (Google’s parent company), Meta, Shopify, and McKinsey Sustainability. Frontier wants to boost early demand and funding for promising carbon removal technologies.

The company does this through long-term purchase agreements. Its initial goal was $1 billion in purchases by 2030, sending a strong signal to the market about future demand.

Source: Frontier

By 2025, Frontier signed contracts for various technologies. These include bioenergy with carbon capture and storage (BECCS), direct air capture (DAC), and enhanced weathering. Several contracts are worth tens of millions of dollars. These agreements help developers survive the early “valley of death,” when financing is hardest to secure.

Market Trends: From Niche to Necessity

The carbon removal market is still small compared with global climate goals, but it is evolving quickly. Industry forecasts say that demand for durable carbon removal credits might hit 100 million tonnes of CO₂ each year by 2030.

This growth is fueled by corporate commitments and government purchases. This is roughly double the supply currently announced, showing a large gap between demand and delivery.

Globally, carbon removal is still a tiny fraction of what is needed. Scientific assessments show that to meet the Paris Agreement, carbon removal needs to increase. By 2050, it should reach 7–9 billion tonnes of CO₂ each year. This is about 4,000 times more than what we do now.

Source: CUR8 website

Market projections show strong growth in the next decade. A report by Oliver Wyman and the UK Carbon Markets Forum estimates that the global carbon removal market could grow from $2.7 billion in 2023 to $100 billion per year by 2030–2035, provided policies and standards evolve to support it.

Local and Global Wins

The Appalachia project highlights how carbon removal can benefit both the climate and communities. Restoring degraded lands improves water filtration, soil health, and wildlife habitats. Communities also gain jobs and income through forest management.

Nature-based projects, including reforestation and forest management, currently dominate removal activity. However, they do not offer the same permanence as engineered removals like BECCS or DAC, which store carbon for centuries or longer. Still, both approaches are necessary to scale the carbon removal market.

From Milestones to Market Momentum

The Google, Meta, and McKinsey deal is a milestone for corporate climate action. Long-term agreements help projects secure funding and expand. They also send strong signals to developers and investors. These deals can shift the market from short-term offsets to long-term, permanent carbon removal solutions.

The industry must grow significantly to meet global climate targets. Expanding beyond early adopter companies is essential. Continued policy support, strong standards, and wider sector participation will help scale removals.

In the next decade, how fast carbon removal technologies grow and the amount of credits produced will be key to achieving net-zero goals. Deals like the Appalachia reforestation project are early steps in building a foundational, long-term carbon removal industry.

The sustainability landscape is increasingly complex. More and more carbon-capture solutions are entering the market, and innovation is a constant thread running through the carbon market. With more possibilities, buyers are faced with more considerations than simply offsetting carbon. In this sphere, two main directions are taking shape—nature-centred or tech-focused.

Nasdaq has backed one of the first carbon removal credit deals licensed under European Union rules. The project is based in Stockholm and is designed to generate high-quality carbon removal credits under a formal EU framework.

This marks a key shift. For years, carbon markets have relied on voluntary standards with mixed credibility. Now, the European Union has developed a regulated system to define what counts as a valid carbon removal. This move aims to build trust and attract large investors into a market that is still in its early stages.

The deal shows growing interest from major companies. It also reflects rising demand for reliable ways to remove carbon from the atmosphere.

Inside the Stockholm Carbon Removal Project

The removal project is run by Stockholm Exergi. It uses a process called BECCS, or bioenergy with carbon capture and storage. This method burns biomass, such as wood waste and agricultural residues, to produce heat and electricity. At the same time, it captures the carbon dioxide released and stores it underground.

The captured CO₂ will be transported and stored deep beneath the North Sea in rock formations. Over time, it will turn into solid minerals. This makes the carbon removal long-lasting and more secure than many nature-based solutions.

The facility is expected to start operating in 2028. Once active, it will generate carbon removal credits that companies can buy to balance their remaining emissions.

Beccs Stockholm is one of the world’s largest carbon removal projects. In its first ten years, the project could remove about 7.83 million tonnes of CO₂ equivalent. This makes it a key tool for helping the European Union reach climate neutrality by 2050.

The project also aims to scale carbon removal by building a full CCS value chain in Northern Europe and supporting a growing market for negative emissions credits.

This project is important because it is one of the first to follow the EU’s new carbon removal certification rules. These rules define how carbon removal should be measured, verified, and reported. They also aim to reduce risks like double-counting and weak accounting.

EU Certification: Building Trust in a Fragile Market

The European Commission has introduced a framework, also called Carbon Removals and Carbon Farming (CRCF) Regulation, to certify carbon removal activities. This includes technologies like BECCS, direct air capture with carbon storage, and biochar.

The goal is to create a trusted system that investors and companies can rely on. It also established the first EU-wide certification framework for carbon farming and carbon storage in products, not just removals.

Until now, the voluntary carbon market (VCM) has faced criticism. Concerns about transparency and “greenwashing” have made some companies cautious. Many buyers want stronger proof that credits represent real and permanent carbon removal.

The EU framework tries to solve this problem. It sets clear rules for:

Measuring how much carbon is removed.

Verifying results through independent checks.

Ensuring long-term storage of CO₂.

This structure may help standardize the market. It could also make carbon removal credits easier to compare and trade across borders. The Commission states that the goal of having the framework is:

“to build trust in carbon removals and carbon farming while creating a competitive, sustainable, and circular economy.”

Corporate Demand Is Growing—but Still Limited

Large companies are starting to invest in carbon removal. However, the market remains small compared to what is needed.

One major buyer is Microsoft. It currently holds about 35% of all global carbon removal credits, making it a dominant player in the market. In fact, it is responsible for 92% of purchased removal credits in the first half of 2025.

Other companies, including Adyen, a Dutch payments provider, have also joined the Stockholm project. These early buyers aim to secure a future supply of high-quality carbon credits as demand grows.

Ella Douglas, Adyen’s global sustainability lead, said in an interview with the Wall Street Journal:

“This project does exactly that [“catalytic impact” to the VMC] while also building key market infrastructure in collaboration with the European Commission.”

Still, many firms remain cautious. Carbon removal technologies are often expensive and not yet proven at a large scale. Some companies also worry about reputational risks if projects fail to deliver real climate benefits.

This creates a gap. Demand is rising, but the supply of trusted credits is still limited.

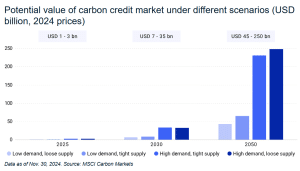

Despite these challenges, the long-term outlook for carbon removal is strong. Estimates suggest the market could reach $250 billion by mid-century, according to MSCI Carbon Markets.

Several factors drive this growth:

First, global climate targets require large-scale carbon removal. The Intergovernmental Panel on Climate Change estimates that the world may need to remove around 10 billion metric tons of CO₂ per year by 2050 to limit warming.

Second, many companies have set net-zero goals. These targets often include removing emissions that cannot be avoided, especially in sectors like aviation, shipping, and heavy industry.

Third, new regulations are pushing companies to disclose and manage emissions more clearly. This increases demand for credible carbon solutions.

However, the current supply falls far short of what is needed. Only a small share of the required carbon removal credits has been developed or sold so far.

Balancing Removal and Emissions Cuts

While carbon removal is gaining attention, experts stress that it cannot replace emissions reductions. Removing carbon from the atmosphere is often more expensive and complex than avoiding emissions in the first place.

Groups like the European Environmental Bureau warn that over-reliance on credits could delay real climate action. They argue that companies should set separate targets for reducing emissions and for removing carbon.

The EU framework reflects this concern. It treats carbon removal as a tool for addressing residual emissions, not as a substitute for cutting pollution at the source. This distinction is important. It helps ensure that carbon markets support, rather than weaken, overall climate goals.

From Concept to Market Infrastructure

The Stockholm project marks a turning point for carbon removal. It shows how rules, strong verification, and corporate backing can bring structure to a fragmented market.

With support from players like Nasdaq, carbon removal is moving closer to becoming a mainstream financial asset. At the same time, the European Union’s certification system is setting the foundation for a more credible and scalable market.

The path ahead remains complex. Technologies must scale. Costs must fall. Trust must grow. But the direction is clear.

Carbon removal is no longer a niche idea. It is becoming a key part of the global climate economy, with the potential to shape investment flows for decades to come.