Ahead of Donald Trump’s second term as US president, a rerun of his first trade war with China is firmly on the cards – and minerals key to the energy transition may end up in the crossfire.

The president-elect has threatened to raise tariffs on goods from China, as well as on other countries through which Chinese goods flow to the US.

While his overall stance towards China remains unclear, Trump has also pinpointed eliminating “dependence on China in all critical areas” as a priority.

Meanwhile, China has been developing a “versatile” policy toolkit to cope with rising trade tensions – including with the EU and Japan, as well as the US.

One notable recent example is China’s use of export controls, which it has placed on four minerals: germanium, gallium, graphite and antimony.

All of these minerals play important roles in low-carbon technologies, but also have other applications, including military uses.

Analysis by Carbon Brief and others shows that China’s initial export controls, introduced in summer 2023, did not have a sustained impact on critical-mineral supply chains.

However, an announcement in early December 2024 of stricter controls, specifically on exports to the US, has sparked debate over how impactful these might be.

In this article, Carbon Brief examines what US-China tensions over critical minerals could mean for the stability of their supply chains and for the transition to cleaner energy.

- Which minerals are important to the clean-energy transition?

- How has China’s ability to control its critical minerals evolved?

- How did the initial export bans affect critical mineral trade flows?

- Do the US-specific controls represent a significant change in China’s strategy?

- Could future US-China tensions exacerbate critical mineral controls?

Which minerals are important to the clean-energy transition?

Minerals are crucial to the development of several low-carbon technologies.

Indium and gallium are used in the coatings for solar panels, copper and “rare earth” metals are used in the conductors and permanent magnets in wind turbines, and a plethora of minerals from lithium to manganese are used in various types of batteries.

China holds a significant presence in the supply chains for many minerals – particularly in terms of processing. As seen in the table below, more than half of global extraction of graphite, rare-earth elements (REEs) and vanadium, as well as the majority of processing of aluminium, cobalt, graphite, indium, lithium, REEs and silicon, occurs in China, according to a study by the Grantham Research Institute on Climate Change and the Environment.

A list of several minerals important for low-carbon technologies, plus the share that China holds in its reserves, extraction and processing industries. Source: Grantham Research Institute on Climate Change and the Environment.

However, not all of these materials are considered “critical minerals”, which is a political term used to describe those that play a role in strategically important sectors, with each country setting their own parameters for strategic importance.

The US lists 50 minerals as critical, while the EU has identified 34 critical minerals and an additional 16 “strategic raw materials”, while Japan has 35 minerals on its list.

Although China has not updated its official critical minerals list since 2016, a November 2023 post on the official WeChat account of the Ministry of State Security (MSS) revealed that it considers at least 31 minerals to be critical.

The post compares areas of overlap and divergence between the critical mineral listings of China (orange), and those in the EU (green) or the US (blue).

The minerals that are “on similar lists” for China and the EU and US are “where there's more competition” when it comes to sourcing, John Johnson, special advisor and former CEO for commodities consulting firm CRU Group’s China office, tells Carbon Brief.

However, despite some countries’ efforts to diversify their imports of critical minerals away from China, analysis by the International Energy Agency (IEA) found that, based on announced projects, the status quo for supply of minerals such as lithium, nickel, cobalt and graphite was unlikely to change between now and 2030.

The IEA analysis noted that, in some areas, such as battery cell manufacturing, “announced capacity additions in Europe and the US should be sufficient to meet the 2030 domestic deployment needs” – although it added that, globally, demand for a number of critical minerals is likely to far exceed supply.

However, Tony Alderson, a senior analyst focused on graphite at price reporting agency Benchmark Minerals Intelligence, is sceptical, telling Carbon Brief that “it's almost unheard of for a facility to be at 100% utilisation rates”. He adds that, for graphite, demand in the US and EU would likely outstrip supply well beyond 2030.

How has China’s ability to control its critical minerals evolved?

China has a well-documented history of using trade restrictions to achieve broader political aims.

The first trade war with the US between 2016 and 2020 saw China try to deescalate US tariffs on Chinese goods by imposing tariffs of its own, as well as non-tariff trade barriers.

The country has also used trade controls to affect non-trade-related political clashes.

Under the Biden administration, the US developed a “small yard, high fence” approach – meaning the US would “be selective in choosing technologies that need protecting, but be aggressive in safeguarding them”.

It placed a series of export controls on semiconductors and products used to make them, encouraging allies such as Japan and the Netherlands to do the same.

In response, China began limiting exports of some critical minerals, placing restrictions in August 2023 on exports of certain types of gallium and germanium, followed by similar restrictions on graphite from December 2023 and on antimony from September 2024.

With the exception of antimony, these restrictions were enacted in a clear response to US moves to curb Chinese imports for use in its semiconductor sector.

At the same time, China began enhancing its export control regime, which unified and rationalised an existing constellation of export control policies into a single framework.

This included development of an “unreliable entity list”, an export control law, legislation to counter foreign sanctions and regulation of items that are considered “dual-use”, meaning they can be used for military as well as civilian purposes.

“Historically, [China’s] export control regime has been extremely piecemeal,” Cory Combs, head of critical mineral and supply chain research at consultancy Trivium China, tells Carbon Brief.

He adds that one of the recent policy push’s major aims was to improve compliance by “making sure everything's in one place and the rules are consistent – that you don't have slightly different standards for different types of controls”.

These efforts paved the way to restrictions on critical minerals being intensified in early December 2024, when China sharpened restrictions on exporting graphite and banned exports of gallium, germanium and antimony to the US “in principle”.

A spokesperson from China’s commerce ministry stated this was in response to the US “weaponising” its own export controls by imposing broad restrictions on the Chinese chip-making industry.

How did the initial export bans affect critical mineral trade flows?

Analysis of China’s initial export controls on gallium, graphite and germanium shows that trade largely continued to flow, despite the new rules.

As shown in the graphs compiled by Carbon Brief below, Chinese exports of restricted types of gallium and germanium stopped for two months after the August restrictions came into effect. However, exports resumed from October 2023, albeit at slightly lower levels.

Not all types of the targeted critical minerals seemed to have been affected by the two-month suspension, with flows of non-controlled products, such as germanium oxides, seeing no significant change.

For graphite, exports of major products remained relatively stable, with the exception of a spike in exports ahead of the restrictions coming into place, likely due to stockpiling. Average exports in 2024 were higher than in 2022.

Both Combs and Johnson both note that, anecdotally, they had not heard of any cases of exporters being unable to acquire licences to export products.

Alderson tells Carbon Brief that exporters, nevertheless, found that the approvals were particularly quick for South Korea and Japan, while it took “longer for [products destined for the] US and India to get licenses approved”.

Analysis by the US-based Peterson Institute for International Economics (PIIE) similarly found that, for the US in particular, the export controls on gallium, germanium and graphite “haven’t radically altered the US-China trading relationship around these minerals and related products”, as shown in the graph below.

For graphite (the blue line in the chart), US imports from February to August 2024 were “only a hair lower than in the seven months preceding the announcement of export controls”, it found.

For germanium (black), in 10 months following the enactment of controls, exports were “down only one percentage point from the ten months preceding the ban”, it added. For gallium (red), while exports have fallen to zero, “the chart makes very clear [that] the US was never particularly reliant on China for sourcing in the first place”.

The PIIE analysis concluded in August 2024, ahead of the restrictions on antimony and US-specific controls.

This outcome was likely by design, due to the calculated nature of China’s export controls.

The goal of the initial export controls was to improve China’s visibility of how the minerals it processed were being used, Combs tells Carbon Brief, which is why the initial controls required exporters to apply for licences, rather than implementing a blanket ban on exports.

Alderson says that the new licences required companies to share more information about themselves, their products and their end users.

As such, cutting off supplies to other countries immediately was not the aim of the original announcements.

The initial controls on critical minerals broadly follow similar patterns to China’s previous non-tariff trade measures. With the exception of antimony, the critical mineral controls were imposed in response to perceived attempts to “undermine China’s national sovereignty, security, and development interests”, rather than being the first salvo of a trade dispute.

This is because, according to a Royal United Services Institute (RUSI) report, China is aware that outright export bans would accelerate other nations’ efforts to derisk and diversify supply chains, weakening its long-term position.

The RUSI report added that export controls must be examined to determine whether the move is meant to be a political signal or a more serious attempt at “economic coercion”.

Stringent export controls incur a domestic cost in China, impacting both industrial activity and broader economic growth. As such, export controls are likely to be calibrated to capture headlines without incurring as severe an economic impact as they imply, RUSI said.

A government official involved in the design of the gallium and germanium controls said they were meant to be a “deterrent”, the Financial Times reported, quoting the official saying: “We had many options…This was not our most extreme move.”

An example of China “going for the throat” with export controls, Combs tells Carbon Brief before the US-specific controls were announced, would be placing controls on copper.

He explains this is because – although Chinese copper is a vital resource in global manufacturing, particularly in clean-energy technologies – the majority of copper smelted in China is consumed domestically. As a result, an export control on copper “would be a perfect case of hurting others without hurting itself too much”.

“Instead”, he says, the initial moves seemed to be saying “don’t test us”.

Do the US-specific controls represent a significant change in China’s strategy?

The measures announced in early December 2024 are a pointed escalation of China’s use of critical mineral export controls.

Under the new rules, gallium, germanium and antimony will “in principle” no longer be permitted to be shipped to the US and tighter controls will be placed on sales of graphite.

In an analysis, Combs and Trivium China co-founder Andrew Polk wrote that the restrictions are a signal that China is “ready to counter US moves much more aggressively”.

This was echoed by China’s former central bank governor Yi Gang, who the South China Morning Post quoted saying: “We all understand that, from an economics perspective, [retaliatory actions are] never a good choice…but there’s not much policymakers can do about that [in the face of domestic pressure].”

More time will be needed to see “how strict” implementation will be, Alderson says, adding that for graphite, it is not yet clear which products will be affected – the stricter controls could be limited to “the 99.999% [purity] which goes into military end-use materials”, rather than the lower-grade graphite used in electric vehicle batteries.

Trivium China’s assessment noted that the announcement suggested China would “close” loopholes that allowed for “export leakage”, adding that it is not clear “how far Beijing might go to investigate or punish third countries suspected of prohibited re-exports”.

Gerard di Pippo, senior geoeconomic analyst for Bloomberg Economics, was sceptical about the significance of the threat, writing that “China lacks the legal reach, export-control surveillance capabilities and alliance network” needed to enforce third-country compliance.

Other analysts told MIT Technology Review that, “for the most part, the bans won’t have major economic impacts”, due to existing US efforts to diversify its supply chains

Nevertheless, Alderson says, the current uncertainty underscores the fact that “localisation is critical” for those that rely on critical minerals.

Could future US-China tensions exacerbate critical mineral controls?

China’s motive for the most recent controls is unclear, Combs and Polk wrote. It could be to protest against the US move to restrict exports of particular chips and chip-making tools as well as the addition of 140 Chinese companies to a trade blacklist, they said, or to “warn the incoming Trump administration” against raising tensions.

It is broadly expected that US-China trade tensions will escalate after Donald Trump begins his second term as US president.

US concerns around the “threat” that China poses to its industrial capabilities have been notably bipartisan. However, where Biden’s approach was characterised by relatively nuanced policies, the second Trump administration – much like the first – could prioritise the use of broad tariffs to shrink the US’ trade deficit with China.

Combs tells Carbon Brief that Beijing’s goal is to “change US behaviour”, so it would “use terms that Trump understands”, such as broad trade tariffs, in trade disputes with the US, rather than the more nuanced controls it has used in response to the Biden administration. He explains:

“Most of the [trade volume and value of these] minerals are way too small to affect the trade balance…so purchases of beef, soy and similar items would make more sense as a retaliation mechanism [for China to use].”

It remains to be seen, he says, how much emphasis Trumps’ advisors, particularly new commerce secretary Howard Lutnick, will place on critical minerals. The issue could appear on the radar should Beijing use additional controls to pressure particular US companies to lobby the US government, he adds.

Johnson notes that China has reasons to avoid escalating the issue of critical mineral exports further, such as its dependency on the US for exports of a number of minerals, such as high purity quartz, iron ore and potash.

In addition, he says, the minerals that countries consider critical “change over time”, as new technologies create demand for new minerals and render other minerals obsolete.

Progress in developing recycling processes could also relieve pressure on supply chains. Scrap is already a small source for supply of gallium and germanium, while germanium can also be recovered from existing products.

According to the IEA, successful scaling-up of recycling could “lower the need for new mining activity by 25‑40% by 2050”, under a scenario that assumes governments will meet all of their climate goals on time and in full.

Meanwhile, other regions seem to be treading cautiously. The Washington Post notes that pushback from the Japanese and Dutch governments led to a “delay” in the launch of the most recent US semiconductor export controls, which were watered down to “accommodate” their concerns.

Combs tells Carbon Brief that he does not see any flashpoints significant enough to trigger export controls on critical minerals to the EU.

“[Restricting China’s ability to buy from] ASML was the single most impactful [move against China by the EU],” he says, adding that there are few, if any, remaining political disputes where Europe would willingly trigger “significant retaliation” from China.

The post Q&A: What could a US-China trade war mean for the energy transition? appeared first on Carbon Brief.

Q&A: What could a US-China trade war mean for the energy transition?

Back in 1978, my year two teacher at Kelmscott Primary School in the foothills of Perth was a woman named Lesley Choules, who was especially fond of homely aphorisms as part of her teaching approach. Mrs Choules would deliver these cheerily, or icily, depending on how we had been behaving, but not much time would pass on any given day without her reminding us that “a smile costs nothing, but gives much”, or more ominously, “idle hands make the devil’s work”. All very old school, no doubt, but delivered with care and sincerity.

I think Mrs Choules was the first person I ever heard say that a “stranger is just a friend you haven’t met yet”. A simple but profoundly lovely sentiment, which is so at odds with the contemporary encouragement by demagogues and algorithms, to treat strangers with suspicion, or as subjects for exploitation.

And I’m exceedingly fortunate to experience the phenomenon of ‘stranger as friend’ quite a bit today as an adult. It occurs on every occasion when I meet someone new and end up finding out that they support Greenpeace.

These moments are wildly unpredictable in their timing-–being told “yes, I support Greenpeace”, mid-needle, by the person giving me the vaccination particularly stands out in my memory. But what I have learned, not just from reading organisational demographic reports but from my own daily life, is that we Greenpeacers are a varied bunch of human beings united by especially wonderful common threads: a sense of personal commitment to seeing an earth capable of nurturing life in all of its magnificent diversity, and a shared conviction that together we have the power to secure this future, whatever the odds. That’s Greenpeace.

So, to pick one recent example, I was on the road with a colleague, and we stopped in at a pub to grab a counter meal at the end of a long day. It was a fairly typical country hotel…some football playing on a big screen somewhere at the back, people tucking into their parmies and chips.

We found a table, and I went up to place our orders, accompanied by a bit of a chat with the person pulling the drinks. In the course of a polite conversation about the World Cup I mentioned in passing that I had South American work colleagues. The bartender then asked where I worked, to which I responded “Greenpeace”.

And then there was the moment.

‘Greenpeace! I get the emails and sign everything! I love the oceans. It started for me when I was travelling around the world and I realised how much damage was being done. I had to do something.’

These occasions carry an enormous significance to me, and to all of us at Greenpeace. On a personal level, they activate something profound and primal: a rush of belonging and sense of kinship and gratitude. I know, as a matter of intellect, that there are millions of people who support Greenpeace all over the world. But there is nothing like the experience of being told by a stranger, “I am part of Greenpeace too”, to viscerally reinforce that powerful, wonderful reality.

It is only this community of ‘strangers who are friends’ that enables Greenpeace to exist at all. Just to think on this for a moment, Greenpeace has run massive campaigns, taking on the most powerful vested interests in the world, for more than fifty years. Yet in that whole time, we haven’t taken funding from any government or business. We exist only because of people who believe in our mission and our method and give of themselves—their time, money, name, skill, energy, trust, talent, passion and perseverance. It is a miracle of collaborative action that we make possible every day, together.

So, with this in mind, I smile at the bartender and say a version of what I always do in these circumstances:

‘Thank you, thank you. Greenpeace only exists because of you, and me, and all of us. So, deeply and sincerely, thank you.’

And it is such a privilege to have the opportunity to say those words, on behalf of an organisation that I have loved since I was a kid, and for a mission that is my vocation, for all life on earth.

I don’t know what Mrs Choules would have made of Greenpeace—a bit naughty maybe—but I remember her as someone who loved nature, and she encouraged that love in her pupils. I like to think she would have recognised our common bonds, and been delighted at their regular discovery in these idiosyncratic encounters.

To meet someone who is part of Greenpeace is to know a friend. Another spirit who has found belonging, purpose, meaning and impact in our shared ideal. The truth is, you never know who, you never know where, but if you sail with Greenpeace, you have mates. You will never face the world alone.

Whatever is here now, whatever is to come, we will see it through together. We have agency on this earth. Across our many languages and lives, we will continue to dream a universal dream of a flourishing planet, and make good on our common conviction that together we have the power to make it so.

With Love,

David

Q & A

A question I was asked this week—and quite often get asked—is, what is the relationship between Greenpeace and other well known environmental organisations like the Wilderness Society, Australian Conservation Foundation, the World Wildlife Fund, Bird Life, Australian Marine Conservation Society and others?

Greenpeace is independent, but we are also deeply collaborative, and so often work closely with our good mates at these organisations and others. For example, a number of those organisations I have mentioned above are involved in opposing Woodside’s threat to Scott Reef, and we are all conscious that we have the greatest impact when we work together.

That said, organisations have varying strengths, histories, organisational and institutional realities, so we can often play different and complimentary roles, depending on our capabilities. On a personal level, I’ve always been very grateful for collegiate, trusting and frank relationships with colleagues and friends within the environmental movement (here’s my note of appreciation for Kelly O’Shanassy, on the occasion of her leaving ACF last year, for example). In that sense too, we are stronger together, and strongest when we each play our own part well

Climate Change

DeBriefed 3 July 2026: US faces scorching Independence Day | Record ocean temperatures | Vietnam’s EV surge

Welcome to Carbon Brief’s DeBriefed.

An essential guide to the week’s key developments relating to climate change.

This week

Heating up

NOT FREE FROM HEAT: “Dangerous, record-breaking” heat altered plans for 4 July celebrations across the US this weekend, reported the Associated Press. New York and Boston hit 100F (37.8C) on Thursday, said the newswire. CNBC reported that temperatures of up to 105F (40.5C) are forecast in central and eastern parts of the country, with “daily, monthly and all-time records possible”.

TEMPERATURES SOAR: Heat that hit western Europe last week spread east to “scorch” Germany, Hungary, Romania, Poland and others, said Bloomberg. Red warnings for extreme heat were issued in a number of nations, noted the outlet, adding that the heat “underscores how climate change is transforming summers in the world’s fastest-warming continent”. The Independent said last month was confirmed to be England’s hottest June on record.

HEAT DEATHS: June’s extreme temperatures caused more than 2,000 excess deaths in Spain and France, reported the Guardian. The countries are bracing for further heat that “could bring temperatures of 44C (111F) over the coming days”, said the newspaper. Deaths in France rose almost 30% at the heatwave “peak” on the week of 22 June, according to Le Monde. Last week’s conditions also led to around 480 excess deaths in the Netherlands, reported Reuters.

BOILING: Global ocean temperatures reached record levels for this time of year, reported NBC News, “fuelling fears of more dangerous heatwaves this summer and fanning concerns over the escalating global climate crisis”. Scientists told the Financial Times that this could lead the world towards “uncharted territory”. The newspaper said global average sea surface temperatures reached 20.96C on 21 June, exceeding June records for 2023 and 2024.

Around the world

- GOAL DROPPED: The World Bank will “abandon” its goal to devote 45% of annual lending resources to climate-related projects, reported Reuters. Carbon Brief explored what it could mean for global climate action.

- FIVE-YEAR PLAN: China plans to invest more than 20tn yuan ($2.9tn) in “key energy projects and new business models” over the next five years, according to International Energy Net.

- DRILLING: The Guardian said UK Labour politicians “urged” the likely next prime minister Andy Burnham to ignore “deluded” calls to develop the Rosebank oil field located in the Atlantic north of Scotland.

- PLASTIC TALKS: Countries and activists feared key issues could be sidelined at “critical” talks on a global treaty to curb plastic pollution in Kenya, said Climate Home News. A treaty could have “important implications” for climate change, reported Carbon Brief in 2024.

- CANADA PIPELINE: Canadian prime minister Mark Carney announced plans to build an oil pipeline to supply Asia with up to 1m barrels per day, reported the Financial Times. Earlier this week, Carney called the previous government’s climate plans “expensive” and “divisive”, said CBC News.

63

The number of UK newspaper editorials calling for more oil and gas extraction in the North Sea so far in 2026, according to Carbon Brief analysis.

Latest climate research

- Including emissions from permafrost thaw raises the likelihood of the Arctic becoming a net-carbon source by more than 50% at 2C of warming | Earth System Dynamics

- Net-zero scenarios relying less on carbon dioxide removals lead to fewer residual emissions, which offers greater health improvements for “non-white and low-income groups” in particular | Nature Climate Change

- Agricultural plots of land in sub-Saharan Africa owned by women face heat impacts 2-2.5 times higher than those owned by men | Nature Sustainability

(For more, see Carbon Brief’s in-depth daily summaries of the top climate news stories on Monday, Tuesday, Wednesday, Thursday and Friday.)

Captured

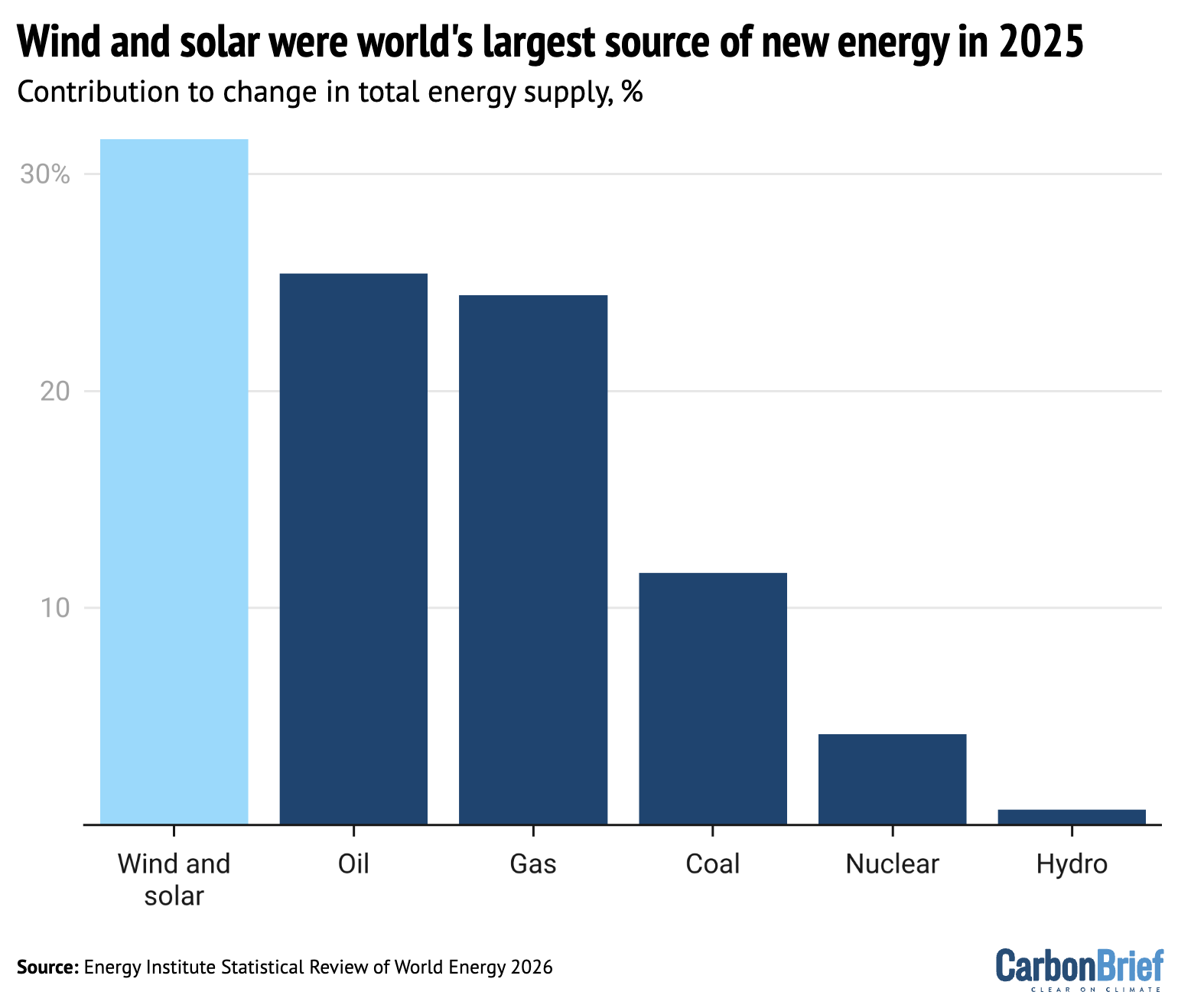

Wind and solar were the world’s largest source of new energy in 2025, according to Carbon Brief analysis of the latest Energy Institute statistical review of world energy. Wind and solar also saw the fastest growth, up by 18% in 2025. Nevertheless, every source of energy – including coal, oil, gas, nuclear and hydro – also reached global all-time highs last year.

Spotlight

Vietnam’s EV surge

Carbon Brief explores the reasons behind soaring electric-vehicle sales in Vietnam.

Motorbikes are a constant fixture on streets across Vietnam. They pollute the air in cities and make crossing the road a feat of endurance.

But, increasingly, people are moving away from petrol-powered vehicles to save money and reduce air pollution.

Sales of electric motorbikes, scooters and mopeds more than doubled in Vietnam last year, according to a recent report from the International Energy Agency (IEA).

This identified that Vietnam has the largest electric vehicle (EV) market in south-east Asia.

Nearly one-in-five of the two-wheeled vehicles sold last year were electric, it noted, in a nation with 102 million people and 77m motorbikes.

This is “particularly impactful” given they are the main mode of transport in Vietnam, said Lam Pham, Asia energy analyst at thinktank Ember. He told Carbon Brief:

“Electrifying road transport is essential for Vietnam to achieve its net-zero target by 2050. Road transport accounted for around 86% of transport-sector emissions in 2022.”

The nation has just 6.8m cars, but this number is also climbing, partly due to EVs, with nearly 40% of new car sales being electric.

This is “above levels seen in most European countries”, noted the IEA. (The UK’s figure is around 30%.)

EV incentives

Fuel costs surged in south-east Asian countries earlier this year after the energy crisis caused by the US-Israel war on Iran.

This “accelerated” discussions from “why use EVs” to “why keep paying more for fuel”, said Dr Tham Nguyen, a lecturer at the Ho Chi Minh City campus of Australia’s Royal Melbourne Institute of Technology (RMIT) University, who has researched Vietnamese public attitudes to EVs.

But the surge is “not driven by fuel prices alone”, noted Pham.

Increased EV sales can also be attributed to a “convergence of affordability, convenience and sustainability”, Nguyen said:

“Vietnamese consumers buy EVs because they see real value with immediate personal benefits, such as cost savings and energy security, alongside long-term environmental gains.”

Government policies have also incentivised sales through registration fee exemptions and tax cuts for EVs.

Another factor is affordable EVs sold by Chinese companies and Vinfast, a Vietnamese manufacturer. The IEA report noted that Vietnam is the only country in south-east Asia with “sizeable” domestic production of accessible EVs.

Vinfast reported a 219% year-on-year increase in orders for electric motorbikes and e-bikes in the first quarter of 2026, but the company has yet to turn a profit.

Pham noted that “growing public awareness of air pollution” has also “dramatically strengthened” public support for EVs.

Future plans

Vietnam’s major cities also have plans to get drivers to go electric or turn to public transport.

The capital city Hanoi announced that it would ban fossil-fuel-powered motorbikes from a central zone this month, but this has been postponed until 2028.

Ho Chi Minh City, the nation’s largest city with more than 9.5 million people, intends to introduce low-emission zones and swap 400,000 petrol-powered motorbikes to electric by 2028.

The city’s green transport plans focus on metro lines, electric buses and e-bikes, explained RMIT associate professor Catherine Earl. She noted that walking and cycling are currently “not popular, accessible or safe for many residents in Ho Chi Minh City’s hot and humid climate”.

Looking ahead, Pham said Vietnam could focus on “purchase subsidies, financing schemes and adequate charging or battery-swapping infrastructure, to ensure lower-income riders, including delivery and ride-hailing drivers, are not negatively affected”.

Watch, read, listen

‘JUST 1%’ OF EMISSIONS: The Guardian debunked arguments that climate actions from smaller countries are “insignificant”.

DRILLING RISKS: Mongabay reported on the possible impacts oil drilling in the Amazon could have on a “little-known reef”.

HEATING UP: The BBC Climate Question podcast discussed the weather pattern El Niño and its links to climate change.

Coming up

- 7-10 July: AI for good global summit, Geneva, Switzerland

- 7-15 July: UN high-level political forum on sustainable development, New York

- 8-10 July: Ninth meeting of the board of the fund for responding to loss and damage, Manila, Philippines

Pick of the jobs

- Green Alliance, senior partnerships officer | Salary: £42,748-£47,346. Location: London

- World Vision, environment and climate action senior adviser | Salary: Unknown. Location: Kenya

- Nature Energy, interim associate or senior editor | Salary: Unknown. Location: London or Milan

- Climate Analytics, senior communications manager – climate policy (maternity cover) | Salary €60,605-€66,880. Location: Berlin

- Carbon Exchange, researcher | Salary: Unknown. Location: Hong Kong

DeBriefed is edited by Daisy Dunne. Please send any tips or feedback to debriefed@carbonbrief.org.

This is an online version of Carbon Brief’s weekly DeBriefed email newsletter. Subscribe for free here.

The post DeBriefed 3 July 2026: US faces scorching Independence Day | Record ocean temperatures | Vietnam’s EV surge appeared first on Carbon Brief.

The World Bank has abandoned a target for 45% of the funding it gives developing countries to be “climate finance”, following months of pressure from the Trump administration in the US.

However, a concerted effort by developed- and developing-country shareholders has seen the bank hold onto its “action plan” for tackling climate change.

The multilateral development bank (MDB) – which is headquartered in Washington DC – is the single largest provider of climate finance globally, distributing $39.2bn in 2025 alone, primarily as loans.

Amid widespread aid cuts by developed countries, the World Bank and other MDBs have previously pledged to significantly scale up their climate finance over the next decade.

Despite scrapping its central target, the bank says it will continue to support the demands of its “clients”, many of which have explicitly stated their need for climate-related investment.

Here, Carbon Brief looks at the likely impact of the World Bank’s policy shift and whether it is – as one expert puts it – “mostly a symbolic victory” for the US.

- How does the World Bank support climate action?

- Why has the World Bank abandoned its climate-finance target?

- Why is the World Bank important for international climate finance?

- How will these changes affect global climate action?

How does the World Bank support climate action?

The World Bank is the oldest and largest MDB. It is tasked by its 189 member governments – the bank’s shareholders – with supporting development projects around the world.

The US is the bank’s largest shareholder, followed, in order, by Japan, China, Germany, France and the UK.

Every year, the bank provides billions of dollars – predominantly as loans – to developing countries.

(One part of the World Bank, the International Development Association – IDA – specifically distributes grants to lower-income nations, as well as lower-interest loans.)

Through its financing, the World Bank also has an important role in “mobilising” private investments in developing countries.

In recent years, the bank has increasingly focused on helping developing countries to cut emissions and adapt their economies for climate change.

The World Bank provided $164bn in what it calls financing with climate “co-benefits” between 2020 and 2025.

The largest share of this funding – roughly one-fifth – went to clean energy and electricity access projects. Smaller shares went to areas such as public transport, water supply and sustainable farming.

As the map below shows, the largest recipients of the bank’s climate funds since 2020 have been emerging economies, such as Turkey ($10.3bn), India ($9bn) and Nigeria ($6.3bn).

Among the largest World Bank projects in recent years are two extensive programmes in India, totalling nearly $3bn, supporting renewables and green hydrogen.

Others include $1.7bn for a Pakistan hydropower project, $926m for Iraq’s railways and $803m to boost “green development” in Colombia.

Despite the bank’s major role in providing climate finance to developing countries, it has faced heavy scrutiny from climate advocates.

In particular, they have noted the dominance of loans that push developing countries further into debt. The World Bank has also been criticised for a lack of transparency around how it classifies projects as “climate-related”, as well as “over-reporting” of climate finance.

Why has the World Bank abandoned its climate-finance target?

When World Bank president Ajay Banga – nominated by former US president Joe Biden – took over the institution in 2023, there were widespread calls for MDB reform.

Many of the bank’s shareholders wanted to see billions more dollars being channelled to support climate action. Later that year, Banga announced that the bank would ensure that 45% of the bank’s funding was climate finance by 2025.

This replaced an existing target of 35% for climate finance between 2021 and 2025, which had been set out in the bank’s second climate change action plan (CCAP).

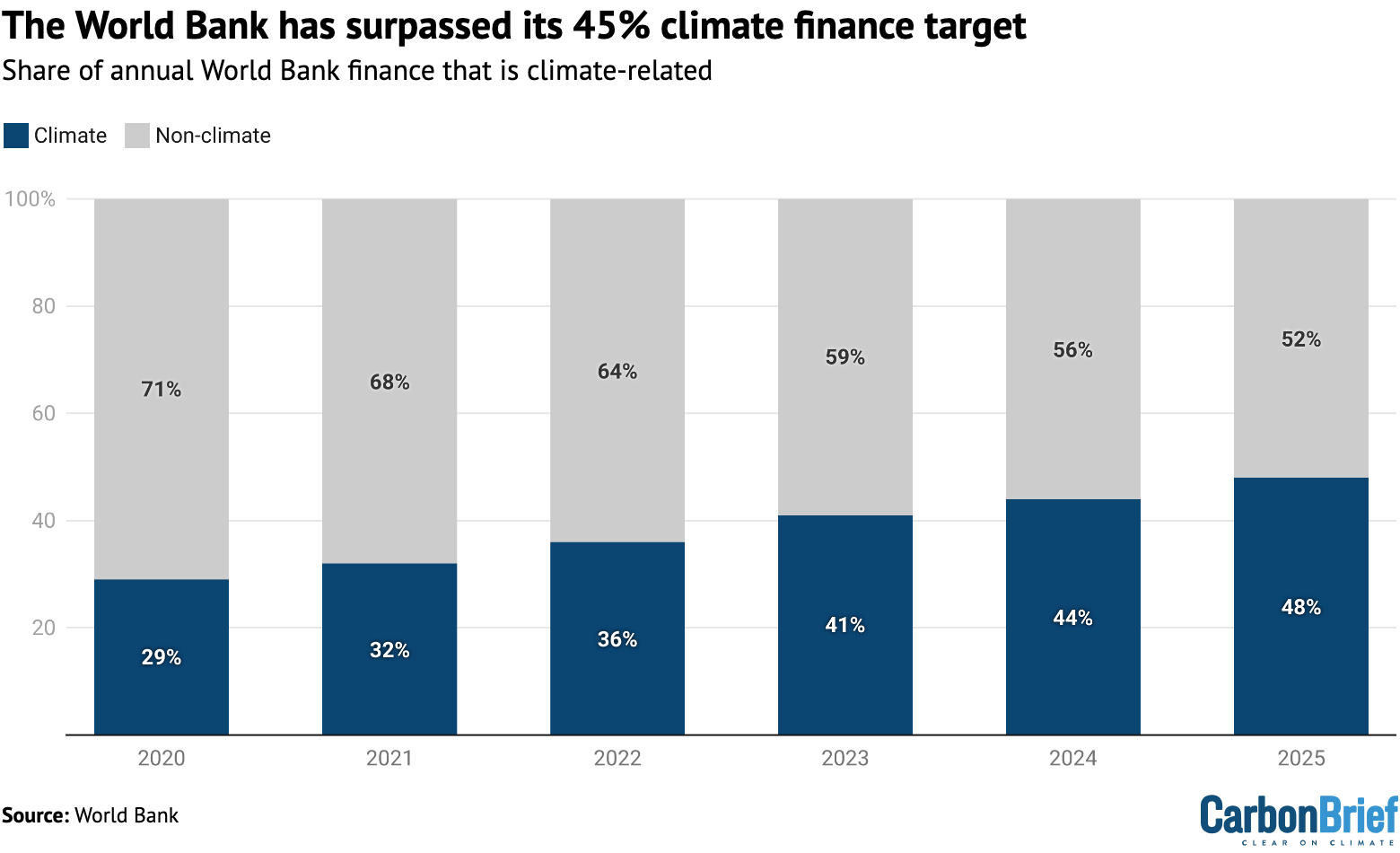

The CCAP is intended to “mainstream” climate action in the bank’s work. With it in place, the World Bank’s climate finance more than doubled from $17.2bn in 2020 to $39.2bn in 2025.

As the chart below shows, this meant the World Bank exceeded its 2025 goal, with climate-related projects making up a 48% share of total funding that year.

When Biden was replaced by Donald Trump as president in 2025, the US administration turned against international cooperation, including climate finance.

However, the US did not walk away from the World Bank, where it exerts considerable power as the largest shareholder.

With the CCAP due to expire in July 2026, the US has spent months pressuring the bank and its shareholders to weaken or abandon the plan altogether.

US Treasury secretary Scott Bessent issued a statement during the 2026 World Bank and International Monetary Fund (IMF) spring meetings in April 2026, in which he called for “jettisoning” the 45% climate-finance target. More broadly, he said:

“We welcome the coming expiration of the CCAP and…expect the bank to immediately shift its myopic focus on climate and financing volumes to one that emphasises high-quality, durable projects.”

This vision involves a push for the World Bank to finance more fossil-fuel projects, including drilling for new gas. (The bank has committed since 2019 to stop funding upstream oil and gas projects.)

The decision on whether to continue with the CCAP was negotiated behind closed doors by the board of directors – representing national shareholders. There were reports of “deep divides”.

A joint statement from 19 of the 25 directors last year affirmed the need for both a plan and a target. The US, Russia, Kuwait and Saudi Arabia all declined to sign up, while Japan and India abstained, according to Reuters.

There were reports of European nations championing a climate plan, bolstered by support from the developing countries that would stand to receive climate finance. The US call to drop the 45% target entirely was reportedly backed by Saudi Arabia and Russia.

Ultimately, the day before the CCAP was due to lapse, the World Bank announced what appeared to be a middle ground. It would drop both the 45% target and the 35% goal it had replaced, while also “extend[ing]” the CCAP.

UK development minister Jenny Chapman told a committee hearing in the House of Commons the next day that this marked a “compromise”. She said:

“It wasn’t clear we were going to get a CCAP at all and a bank without an action plan on climate is a problem for us – so that’s a good outcome.”

Supportive shareholders had been pushing for a one-year extension of the plan. While the World Bank did not initially define the length, Chapman confirmed on LinkedIn that the plan had, in fact, been extended “indefinitely”.

The bank said it would also engage an “independent evaluation group” to assess the CCAP, in line with a board request.

Gaia Larsen, director of climate finance at the World Resources Institute (WRI), tells Carbon Brief that this evaluation will likely be “relatively free from political ideology” and could be “focused on how to make the CCAP more effective”.

Why is the World Bank important for international climate finance?

Under the Paris Agreement, developed countries – including major World Bank shareholders in Europe and elsewhere – are obliged to provide climate finance for developing countries.

This includes a target of $300bn a year by 2035, which is expected to largely come from developed countries. One significant way these nations can contribute to this goal is via their support for MDBs, particularly the World Bank.

The World Bank has described itself as “by far the largest provider of climate finance to developing countries”. Each year, it oversees half of all climate finance from MDBs and far more than any single donor country.

Many developed countries have, therefore, enthusiastically backed the World Bank’s climate efforts, as well as a “bigger” role for MDBs in development more broadly. The bank can lend sums that far exceed the amount of new public finance that individual nations are willing to commit.

This is particularly significant, given many of these nations, including the UK, Germany and France, have announced large cuts to their aid budgets in recent years.

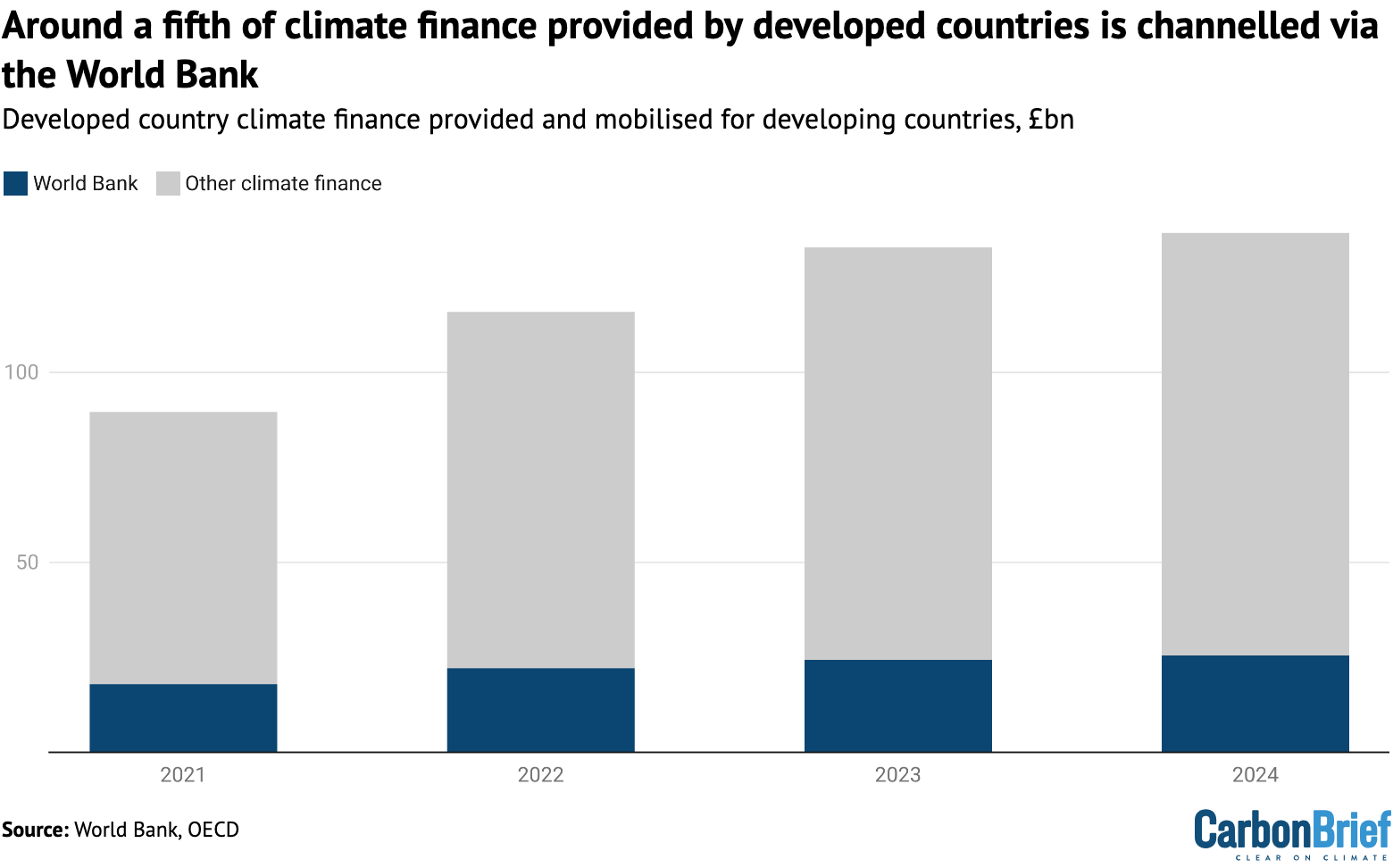

Carbon Brief analysis suggests that roughly a fifth of the international climate finance provided and “mobilised” by developed countries in recent years can be attributed to their World Bank contributions, as the chart below shows.

(This only accounts for the World Bank financing that can be linked to developed-country shares in the bank. Developing countries, such as China, also have significant shares, which are not included in the chart below.)

MDBs – including the World Bank – have committed to providing $120bn in climate finance to developing countries by 2030.

This was set to come from greater shareholder contributions, combined with a programme of reforms to free up capital.

If the World Bank continued to provide half of the MDB total, it would need to increase its climate finance by around 50%, from $39.2bn today to $60bn in 2030.

Therefore, experts see a “key” role for the World Bank in achieving not only the $300bn target, but also the more aspirational $1.3n target that countries agreed as part of the “new collective quantified goal” (NCQG) on climate finance at COP29 in 2024. This includes the private capital it could “unlock” through its lending.

Joe Thwaites, international climate finance director at Natural Resources Defense Council (NRDC), tells Carbon Brief that these “NCQG politics” are “quite important”. He says:

“The maths of the $300bn does not work if the MDBs pull back and so I think that’s why you’re seeing developed countries taking a stand.”

How will these changes affect global climate action?

To date, the World Bank has only released minimal details about its new climate plans. As such, experts say the impact on future climate finance remains uncertain.

Jon Sward, environment project manager at the Bretton Woods Project, tells Carbon Brief:

“They have said they are going to retain all the same processes about climate-finance reporting. So, of course, there is a world in which, actually, climate finance continues to increase like it has been.”

Some of the World Bank’s internal organisations will, in fact, keep their climate-finance goals for the time being. For example, the IDA’s largely grant-based funding retains a 45% target for its current round, which will last until 2028 – the year of the next US presidential election.

However, WRI’s Larsen tells Carbon Brief that the changes, from a bank that was previously a “champion for climate action”, remain significant:

“This reality, reinforced by the elimination of the 45% goal, means that it would not be surprising to see a reduction in climate investments.”

In a statement, the World Bank said its “work on climate is and will remain firmly client driven”, noting that it supports nations undertaking their Paris Agreement climate plans.

Therefore, its climate focus may come down to whether there is demand for climate action from “client” countries receiving finance.

At an April event in discussion with the climate sceptic Bjørn Lomborg, Bessent said that global financial institutions should focus on growth, characterising climate action as an “elite belief”.

The implication from the US Treasury secretary was that recipient countries are not interested in climate action. However, as reported by Devex, a group of World Bank shareholders representing nearly 100 developing countries, wrote a letter that appeared to push back against this framing.

This “G11+” group, led by Brazil and China, said the bank “must remain firmly client-driven”, noting that countries are “following nationally determined pathways toward climate action”. NRDC’s Thwaites tells Carbon Brief:

“It’s one thing for the Europeans to talk about climate…This was the client countries [100 developing countries] saying: ‘No, we want this.’”

Recent research by the ODI thinktank found that 79% of developing-country officials polled wanted to see MDB investment in solar projects, 54% wanted hydropower and 47% wanted wind power. Only 13% wanted investment in gas-power plants.

Rishikesh Ram Bhandary, a senior development researcher at Boston University, has stressed the need for an “enhanced CCAP”, which could be supported by the bank’s new independent evaluation. Among other things, he tells Carbon Brief:

“The bank needs to make a more convincing case about how climate change is being integrated into development priorities rather than competing with them.”

Thwaites says he is hopeful that the outcome is “mostly a symbolic victory for the US”.

However, he says major shareholders from Europe and elsewhere should make it clear to the bank that it is not “the only game in town” when it comes to climate finance. He says:

“If [the World Bank] are going to cave into one shareholder, when the vast majority of the other shareholders are supportive of continuing climate action, they can take their money elsewhere.”

The post Q&A: How will the World Bank’s abandoned finance goal affect climate action? appeared first on Carbon Brief.

Q&A: How will the World Bank’s abandoned finance goal affect climate action?

-

Greenhouse Gases11 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Climate Change11 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Renewable Energy8 months ago

Renewable Energy8 months agoSending Progressive Philanthropist George Soros to Prison?

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Greenhouse Gases12 months ago

嘉宾来稿:探究火山喷发如何影响气候预测