A new joint venture has launched to help countries enhance carbon mitigation efforts under Article 6 of the Paris Agreement. This partnership includes various technology and sustainability firms. They aim to build digital systems and tools for a carbon mitigation pipeline worth over US$100 billion. This funding focuses on forest and nature-based internationally transferred mitigation outcomes (ITMOs). Article 6 outlines rules for global cooperation on climate action through carbon markets.

The collaboration will help governments track emissions cuts. It will also verify climate actions and share mitigation results clearly. It will also develop digital infrastructure to promote high-integrity carbon credits and environmental assets across regions like Africa, South America, the Middle East, and Asia.

What the Joint Venture Will Do

The joint venture includes three partners with distinct expertise:

- Aleria: A specialist in artificial intelligence (AI) and data.

- Tawasal: A UAE-based super app platform.

- Xange.com: An environmental intelligence software provider.

They will work together to build digital systems for carbon accounting and ITMO transfers. This will help governments and project developers. Their tools include monitoring, reporting, and verification (dMRV) systems to capture verified mitigation data. They will also introduce a global infrastructure solution called GEMIS for policy-aligned project management.

A central registry and settlement platform will enable countries to track and transfer mitigation outcomes. This system will help governments manage carbon mitigation results from international trade. It follows the rules of Article 6 and will have a financial custodian bank in Chicago to host and oversee the settlement system.

The joint venture will connect its systems to millions of users through Tawasal’s platform. This includes payment systems from partners like Gnosis and Noxxo. They support transactions across different regions.

Eric Leandri, CEO of Aleria and Tawasal remarked during the Davos announcement:

“Article 6 requires governments to operate credible registries, data systems, and settlement processes under national authority. This joint venture focuses on delivering the technical infrastructure needed to support compliant accounting, monitoring, and transfer of mitigation outcomes. By combining Aleria’s sovereign data capabilities, Tawasal’s digital platform, and Xange.com’s market infrastructure, we are enabling countries to implement Article 6 mechanisms in line with Paris Agreement requirements.”

Why Article 6 Needs Strong Digital Infrastructure

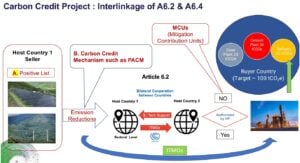

Article 6 of the Paris Agreement provides a framework for countries to work together on emissions reductions. It has three main parts:

- Article 6.2: Rules for accounting and trading of ITMOs.

- Article 6.4: A new mechanism for high-quality carbon credits and emissions reductions.

- Article 6.8: Non-market methods for climate action without trading emissions units.

Article 6 allows countries and companies to collaborate by transferring emissions reductions across borders. These transfers count toward climate targets known as Nationally Determined Contributions (NDCs). A strong digital tracking system is essential to prevent errors like double-counting.

International carbon market cooperation under Article 6 is growing. For instance, Singapore signed an agreement with Papua New Guinea in 2023. This deal enables the two countries to generate and trade carbon credits toward their climate targets.

African nations, like Rwanda, are also preparing to engage with Article 6 mechanisms and carbon markets. They are developing national frameworks and enhancing institutional capacity.

Countries like Indonesia and Norway are participating in Article 6 cooperation as well. At COP30, they talked about carbon trading deals. These could involve up to 90 million tonnes of CO₂ reductions. So far, 12.5 million tonnes are already committed.

These developments highlight the need for strong registry systems and verification infrastructure for effective international climate cooperation.

- SEE MORE: Billions at Stake: UN Panel’s Article 6.4 Recommendation Could Transform Global Carbon Trading

Digital MRV and Registries: The Market’s Missing Link

Successful carbon markets depend on accurate data and transparent tracking. The joint venture’s digital tools will help countries meet Article 6 requirements for emissions accounting. Key components include:

- dMRV tools: Capture verified emissions data and spot environmental risks.

- ITMO registry: A platform for recording, authorizing, and transferring mitigation outcomes.

- Settlement systems: Secure systems for transferring and ensuring transparency.

These tools are crucial because accurate tracking of mitigation outcomes is a requirement under Article 6. Countries must show that carbon credits or ITMOs represent real reductions. Without reliable systems, countries can’t trust transfers to meet climate goals.

This project helps build the Article 6 registry infrastructure by the United Nations Framework Convention on Climate Change (UNFCCC). In 2026, the UN started building systems to track mitigation outcomes. This includes international registries that help national systems work together to enhance transparency and confidence in carbon markets.

Global Momentum Behind Article 6 Cooperation

The JV has identified a pipeline of over US$100 billion in forest and nature-based outcomes aligned with the Paris Agreement. This figure reflects the projected value of various mitigation activities eligible for Article 6 cooperation.

Article 6 cooperation could unlock both private and public funding for climate mitigation. For example, Singapore started a public tender for at least 0.5 million metric tons of high-quality, nature-based carbon credits under Article 6. This is part of Singapore’s plan to reduce emissions to about 60 million metric tons of CO₂ equivalent by 2030. It estimates needing around 2.51 million metric tons of ITMOs annually from 2021 to 2030 to meet its targets.

Countries are also establishing bilateral and multilateral cooperation on Article 6. For instance, Zambia signed a cooperation agreement with Switzerland at COP30 in 2025 to set up frameworks for trading carbon credits. This deal aims to support climate mitigation projects and financing in Zambia.

Market analysts note that over 120 countries are willing to use Article 6 instruments for their NDCs. These countries recognize that cooperation can lower costs by allowing more effective climate action. Capacity-building programs under the UN Environment Programme aim to help developing countries engage in international carbon markets.

Integrity, Regulation, Risks, and Market Outlook

While interest in Article 6 markets is strong, challenges remain. Some project developers have raised concerns about retroactive changes to market rules. Standards bodies, like the Gold Standard, suggest new alignment requirements for Paris compliance. Developers warn that applying these rules retroactively could create uncertainty for existing projects. Stable rules are crucial for long-term investment in mitigation.

Another challenge is ensuring the integrity of mitigation outcomes. Countries and buyers need assurance that carbon credits or ITMOs reflect real emissions reductions. Article 6 systems aim to minimize risks like overestimation, but more work is needed as markets evolve.

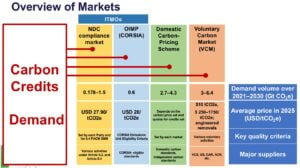

Despite these challenges, the market outlook for Article 6 cooperation is substantial. Projections from the University of Maryland and IETA estimate over $100 billion in annual trading by 2030. This matches wider industry forecasts. The CAREC Program sees Article 6 boosting the carbon market to $250 billion.

Also, Oxford Energy Studies expects annual demand to exceed 700 MtCO₂e. This demand is driven by NDC gaps and the growth of bilateral ITMO.

What This JV Signals for Future Carbon Markets

The new joint venture aims to support a US$100 billion carbon mitigation pipeline under Article 6 of the Paris Agreement. It will help countries create digital systems for tracking, reporting, and transferring ITMOs.

Creating registries, using digital monitoring, and ensuring secure settlement systems are key to building trust in carbon markets. Governments and markets are already building capacity. An increase in bilateral agreements and registry infrastructure indicates stronger adoption ahead.

The joint venture’s pipeline estimate signals significant investment potential in forestry and nature-based mitigation. While challenges exist, the emerging Article 6 ecosystem aims to unlock funding that helps countries meet climate goals with integrity and transparency.

The post $100B at Stake: New Joint Venture Builds Digital Backbone for Article 6 Carbon Markets appeared first on Carbon Credits.

A new beer is turning carbon removal into a real-world product. U.S.-based Aircapture and Almanac Beer have launched what they call the world’s first commercial beer carbonated using (carbon dioxide) CO₂ captured directly from the atmosphere.

The system uses direct air capture (DAC) technology. It pulls carbon dioxide from ambient air and delivers it on-site for use in brewing. The captured CO₂ replaces conventional industrial CO₂, which is usually sourced from fossil fuel processes.

The DAC unit is installed at Almanac’s brewery in California. It captures CO₂ from the air and feeds it directly into the beer carbonation process. This removes the need to transport CO₂ from external suppliers and reduces the carbon footprint of production.

While the volume of CO₂ used in beer is small, the concept is significant. It shows how captured carbon can move beyond storage and into everyday consumer products.

How Direct Air Capture Works in Practice

Direct air capture is a technology that removes CO₂ directly from the atmosphere. Unlike traditional carbon capture, which targets emissions at industrial sources, DAC works anywhere.

The process uses chemical materials to bind CO₂ from the air. The captured gas is then purified and either stored or reused. In this case, it is reused in beverage production.

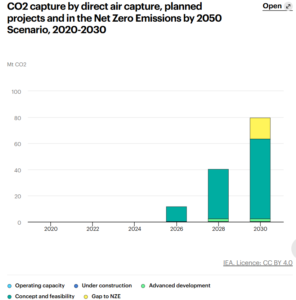

Globally, DAC is still at an early stage. According to the International Energy Agency, only 27 DAC plants are operating worldwide, capturing about 0.01 million tonnes of CO₂ per year.

However, the pipeline is growing. More than 130 DAC facilities are in development, including large-scale plants that could capture over 1,000 tonnes of CO₂ per year each.

Aircapture’s model is different from many large DAC projects. Instead of building centralized plants, it installs modular units directly at industrial sites. This allows companies to use captured CO₂ on-site, reducing transport costs and emissions.

This approach fits well with industries like food and beverage, where CO₂ is already used as an input.

Why CO₂ Matters in Beer Production

Carbon dioxide plays a key role in brewing. It creates the bubbles in beer and affects taste, texture, and shelf life. Most breweries rely on industrial CO₂ supplies, often sourced from fossil fuel processes or as a byproduct of fertilizer production.

This supply chain has faced disruptions in recent years. CO₂ shortages have affected breweries across the U.S. and Europe, highlighting the risks of relying on centralized supply.

Using DAC changes this model. Breweries can produce CO₂ on-site, reducing supply risks and emissions. It also provides a way to use carbon that would otherwise remain in the atmosphere.

Damian Fagan, CEO of Almanac Beer Co., stated:

“Brewing is both science and craft. By integrating direct air capture into our production floor, we’re rethinking one of our essential ingredients and contributing to carbon-removal efforts. Instead of relying on distant industrial supply, we’re sourcing CO₂ from the air right here in Alameda. It’s local, circular, and a glimpse of what the future will look like.”

This does not make beer carbon-negative on its own. But it reduces reliance on fossil-derived CO₂ and shows how carbon can be reused in circular systems.

Almanac’s DAC unit captures 50-100 tCO₂/year, small volume, massive market signal. On-site generation cuts fossil CO₂ emissions from trucking by 20-30% in the supply chain. It also creates premium utilization credits for beverage Scope 3 or supply chain emissions.

DAC Market Set for Explosive Growth

The launch comes as interest in carbon removal technologies is rising. Governments and companies are investing in solutions that remove CO₂ from the atmosphere, not just reduce emissions.

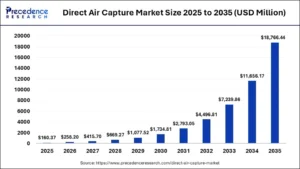

The DAC market is still small but growing fast. One estimate values the market at about $160 million in 2025, with projections reaching nearly $18.7 billion by 2035, growing at a 61% annual rate.

Other forecasts show similar trends. The market could reach over $9 billion by 2033, driven by corporate climate targets and government incentives.

This growth is supported by key factors, including:

- Net-zero commitments from major companies,

- Carbon pricing systems and policy support,

- Demand for high-quality carbon removal credits, and

- Advances in carbon capture technology.

North America currently leads the DAC market, accounting for a large share of global deployment. However, scaling remains a challenge. DAC systems require energy and infrastructure, and costs are still high compared to other climate solutions.

- SEE MORE: Deep Sky and Skyrenu Launch North America’s First Direct Air Capture (DAC) Storage Facility

From Storage to Utilization: A New Carbon Economy

Most DAC projects focus on storing CO₂ underground. This is known as carbon dioxide removal (CDR). It is essential for reaching global climate targets, especially for hard-to-abate sectors.

But there is growing interest in carbon utilization. This means using captured CO₂ as a resource rather than storing it. Common applications include:

- Synthetic fuels

- Building materials

- Chemicals

- Food and beverages

The beer project shows a simple but visible example of this shift. It turns captured carbon into a product that consumers can see and use.

While the scale is small, it helps build awareness and demand for carbon removal technologies. It also shows that DAC can integrate into existing industries without major changes to production systems.

Corporate Climate Strategies Drive Innovation

Projects like this are also linked to corporate climate goals. Many companies are looking for ways to reduce emissions across their operations and supply chains. Carbon removal is becoming part of these strategies.

Using captured CO₂ in products supports these goals. It reduces reliance on fossil inputs and creates new pathways for decarbonization.

More notably, in sectors like food and beverage, where emissions are harder to eliminate completely, these solutions can play a supporting role.

Carbon Markets Expand Beyond Offsets

The launch of a DAC-based beer highlights a broader shift in carbon markets. The focus is expanding from reducing emissions to actively removing and reusing carbon.

Carbon markets are expected to grow as demand for high-quality carbon credits increases. Many experts see carbon removal as essential for meeting global climate targets.

At the same time, new use cases for CO₂ could create additional value streams. Instead of treating carbon only as a cost, companies can use it as an input for products.

However, scale remains the key challenge. Current DAC capacity is far below what is needed. The IEA notes that global DAC deployment must reach around 65 million tonnes of CO₂ per year by 2030 to align with net-zero pathways. This will require major investment, policy support, and technological progress.

A Small Beer with a Big Climate Message

The beer itself is a niche product, but the idea behind it is larger. It shows how carbon removal can move into everyday life and consumer markets.

By turning captured CO₂ into a usable product, companies can demonstrate the value of climate technologies in simple terms. This can help build public support and encourage further investment.

The project also highlights a key trend. Climate solutions are becoming more integrated into business operations, not just separate offset programs.

For now, a single beer will not change global emissions. But it offers a glimpse of how carbon could be managed differently in the future, not just emitted or stored, but reused in practical ways.

The post From Air to Ale: Introducing the First-of-its-Kind Beer Made with Captured Carbon appeared first on Carbon Credits.

Carbon Footprint

IEA Sounds Alarm as War Disrupts Energy Markets, Boosting Australia’s Uranium Demand

The global energy system is under pressure again. This time, the shock is not just about oil and gas. It is also about minerals that power clean energy and nuclear technologies. Media reports revealed that, according to International Energy Agency chief Fatih Birol, the current crisis could soon look small compared to what lies ahead in critical minerals.

Speaking at a major industry event in Canberra, Birol warned that supply risks in minerals like uranium, copper, and battery metals could reshape global energy security. His message was clear: countries must diversify supply chains now or face deeper disruptions later.

A New Energy Shock Unfolds

The world is already dealing with a massive energy disruption. The ongoing conflict involving the United States, Israel, and Iran has removed the equivalent of around 10 million barrels of oil per day from global markets, according to the IEA. This supply gap has pushed countries to rethink energy security. Oil prices remain volatile, and supply routes are under strain. However, Birol stressed that the bigger challenge may not be oil at all.

Instead, the future risk lies in critical minerals. These materials are essential for clean energy systems, electric vehicles (EVs), and nuclear power. Without stable access to them, the global energy transition could slow down sharply.

The problem is concentration. Today, one country dominates the refining and processing of many key minerals. China controls more than 80% of global refining capacity for several critical materials, according to IEA estimates. This creates a major bottleneck in supply chains.

To sum up, without urgent diversification, countries could face even greater risks than today’s energy shock.

Amid these concerns, Australia is emerging as a key player. The country holds vast reserves of critical minerals and energy resources. This includes uranium, lithium, copper, and natural gas.

Australia has the world’s largest uranium reserves. It accounts for roughly one-third of the known global resources, according to data from the Minerals Council of Australia. At the same time, it ranks among the top global uranium producers, alongside Kazakhstan, Canada, and Namibia.

This puts the nation in a strong position as nuclear energy gains traction again worldwide. IEA highlighted that Australia is a reliable supplier that does not use energy exports as a geopolitical tool. This reliability is becoming more valuable as global tensions rise.

At the same time, Australia is also rich in battery minerals. It is the world’s largest producer of lithium and a major supplier of nickel and cobalt. These materials are critical for EV batteries and renewable energy storage.

The IEA expects global nuclear capacity to grow strongly through 2035. In its latest outlook, nuclear generation could rise by nearly 50% by 2040 under net-zero scenarios. This shift will significantly increase demand for uranium. According to the World Nuclear Association, uranium demand could double by 2040 if new reactors and SMRs scale up as expected.

For Australia, this presents a major export opportunity. Even though the country does not use nuclear power domestically, it plays a crucial role in supplying fuel to the global market.

One of the biggest shifts expected from this crisis is the revival of nuclear energy. Governments are now looking for stable, low-carbon energy sources that can reduce reliance on volatile fossil fuel markets.

As per WNA, in 2022, Australia produced 4087 tU of uranium, 8% of global production. Uranium comprises about 17% of the country’s energy exports in thermal terms.

Contracted Imports of Australian Uranium Oxide Concentrate – U3O8

LNG Demand Set to Rise

The current crisis is also boosting demand for liquefied natural gas (LNG). Damage to energy infrastructure in the Middle East has disrupted supply flows, forcing countries to seek alternatives.

Australia is already one of the world’s largest LNG exporters. Projects in Western Australia and Queensland supply key markets across Asia, including Japan, South Korea, and China.

Birol said demand for Australian LNG is expected to grow further as countries look for stable suppliers. This could strengthen Australia’s role in global gas markets in the short to medium term. Similarly, Wood Mac had also projected earlier that the nation’s exports would remain steady throughout this year,

According to the International Energy Agency, global LNG demand is projected to rise by around 3–4% annually through 2030, driven by Asia’s energy needs and coal-to-gas switching.

- READ MORE: War Could Boost Carbon Credit Demand: How Middle East Energy Crisis May Reshape Climate Markets

EV Growth Drives Copper and Battery Metals

Beyond nuclear and gas, electrification is another major trend shaping demand. The global shift to EVs and renewable energy systems is accelerating the need for metals like copper, lithium, and nickel.

Copper is especially important. It is used in power grids, EV motors, and renewable energy systems. Birol emphasized that expanding electricity grids worldwide will require massive amounts of copper.

The IEA estimates that clean energy technologies could double global copper demand by 2040. Similarly, lithium demand could grow more than 40 times under aggressive climate scenarios.

As said before, Australia is well-positioned here too. It leads global lithium production and has large untapped reserves of other key minerals. This gives it a strategic advantage as countries race to secure supply chains.

Investment Trends Show Growing Interest

Recent data shows rising investment in Australia’s resource sector. Uranium exploration spending has picked up after years of decline. According to the Australian Bureau of Statistics, uranium exploration spending reached about $55 million in 2023. This marked the highest level in over a decade.

This increase reflects renewed interest in nuclear energy and long-term expectations of higher uranium demand. At the same time, mining companies are investing more in critical minerals projects. Governments are also stepping in with policies to support domestic processing and reduce reliance on foreign supply chains.

While the current energy crisis is serious, Birol’s warning points to a deeper challenge. The world is entering a new phase where minerals, not just fuels, will define energy security. If supply chains remain concentrated, disruptions could become more frequent and more severe. This could slow down clean energy deployment and push up costs.

Diversification is key. Countries need to invest in new mining projects, expand refining capacity, and build resilient supply networks. And Australia is likely to play a central role in this shift. Its vast resources, stable political environment, and strong export infrastructure make it a critical partner for many nations.

The global energy landscape is changing fast. Oil shocks are no longer the only concern. Critical minerals are becoming the new backbone of energy systems. As nuclear power returns, EV adoption rises, and clean energy expands, demand for these materials will surge. This creates both risks and opportunities.

The challenge now is to scale supply, diversify processing, and ensure these materials remain accessible. If not, today’s energy crisis could soon be overshadowed by a much larger minerals crunch.

The post IEA Sounds Alarm as War Disrupts Energy Markets, Boosting Australia’s Uranium Demand appeared first on Carbon Credits.

A new agreement between Microsoft and Liferaft highlights the rapid growth of carbon removal markets. The deal covers 1 million carbon removal units or credits over 10 years, making it one of the latest long-term offtake agreements in the sector.

These agreements are important. They give developers guaranteed future demand while helping them raise capital, build projects, and scale operations. For buyers like Microsoft, they secure access to high-quality carbon removal credits in a tight market.

Phillip Goodman, Director, Carbon Removal at Microsoft, commented:

“At Microsoft, we’re pleased about the Liferaft project’s potential to pair high-quality, durable carbon removal with meaningful local benefits. Liferaft has strong plans for putting locally available biomass waste to productive use, generating local jobs, and supporting farmers and land managers. This demonstrates how carbon removal can strengthen agricultural communities, improve land outcomes, and deliver durable climate impact.”

The deal also reflects a broader shift. Companies are moving from short-term carbon offsets to long-term carbon removal contracts. These focus on physically removing carbon dioxide from the atmosphere and storing it for long periods.

Microsoft Expands Its Carbon Removal Playbook

Microsoft is the largest corporate buyer of carbon removal credits today. The company has rapidly scaled its purchases in recent years.

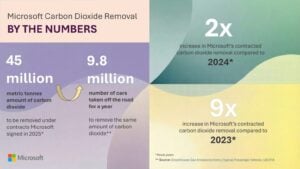

In 2025 alone, Microsoft signed agreements covering about 45 million tonnes of carbon removal. This was more than double its 2024 volume and a major jump from about 5 million tonnes in 2023.

- The company also dominates the broader market. In 2024, Microsoft accounted for about 63% of all durable carbon removal purchases, securing over 5.1 million tonnes.

Recent deals show how fast this is growing:

- 2.85 million tonnes of soil carbon removal credits with Indigo Ag over 12 years

- 2 million tonnes from afforestation projects in Africa

- 1.24 million biochar credits in one of the largest deals of its kind

- 3.6 million tonnes from a bioenergy carbon capture project in the U.S.

These numbers show a clear trend. Microsoft is using long-term contracts to build supply across multiple carbon removal pathways.

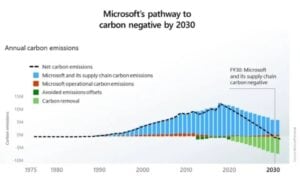

The company’s goal is ambitious. It aims to become carbon-negative by 2030 and to remove all its historical emissions by 2050. Carbon removal plays a key role in achieving this target.

- SEE MORE:

Why Biochar Is Dominating Early Carbon Markets

Biochar is produced by heating organic materials like agricultural waste in low-oxygen conditions. This process locks carbon into a stable solid form that can be stored in soil for hundreds to thousands of years.

It is considered one of the most practical carbon removal methods available today. Moreover, it is relatively low-cost compared to technologies like direct air capture. It can also scale faster because it uses existing biomass waste.

Biochar already plays a major role in the market. In 2024–2025, it accounted for about 86% of global carbon removal purchases and deliveries.

Demand is strong, but supply is limited. In 2024, biochar made up a large share of purchases, but actual issued credits remained below demand levels.

The long-term potential is also huge. Estimates suggest biochar could remove between 0.3 and 4.9 billion tonnes of CO₂ per year globally, with some studies pointing to around 3 billion tonnes annually using available biomass waste.

This makes biochar one of the most scalable carbon removal options available today.

How Offtake Deals Help Scale Carbon Removal

The Liferaft–Microsoft agreement follows a model that is becoming standard in carbon removal markets: long-term offtake contracts.

These deals serve several purposes:

- They provide price certainty for developers.

- They reduce investment risk for new projects.

- They help scale technologies that are still early-stage.

Microsoft has emphasized that early demand is critical. By committing to future purchases, companies help suppliers secure financing and expand capacity. This model is similar to how renewable energy markets grew. Long-term power purchase agreements helped scale solar and wind by guaranteeing revenue.

Now, the same model is being applied to carbon removal.

From Offsets to Permanent Carbon Removal

The carbon removal market is still small but growing fast. Demand is driven by corporate climate targets and stricter net-zero standards. Global purchases of carbon removal credits reached about 8 million tonnes in 2024, up nearly 78% from 2023.

By 2025, demand had already surged further, with tens of millions of tonnes under contract. Looking ahead, forecasts show strong growth:

- The market could reach $40 billion to $80 billion per year by 2030.

- By 2050, it could expand from $300 billion to $1.2 trillion annually.

However, supply remains a key constraint. Less than 1 million tonnes of durable carbon removal credits have been issued globally, far below demand.

This gap is pushing companies to secure long-term contracts early. It also supports higher prices for high-quality credits, especially those with long-term storage like biochar.

Carbon Removal Becomes Essential for Net Zero

Carbon removal is now seen as essential for climate goals. Reducing emissions alone is not enough. Some emissions are hard to eliminate, especially in sectors like agriculture, aviation, and heavy industry.

Carbon removal helps address these residual emissions. It removes CO₂ directly from the atmosphere and stores it in a durable way.

Experts note that carbon removal is what makes “net-zero” possible. Without it, many climate targets would be difficult to achieve at scale. This is why companies like Microsoft are investing heavily in the sector. They are building portfolios that include:

- Nature-based solutions like forests and soil,

- Engineered solutions like DAC and BECCS, and

- Hybrid approaches like biochar.

This diversified strategy reduces risk and supports multiple technologies at once.

A New Phase for Carbon Markets Emerges

The Liferaft agreement may seem small compared to Microsoft’s larger deals. But it reflects an important shift in the market.

First, it shows that demand is spreading across more suppliers. This helps build a broader and more competitive market.

Second, it highlights the growing role of biochar. As one of the most mature carbon removal methods, it is likely to remain a key part of early market growth.

Third, it reinforces the importance of long-term contracts. These agreements are becoming the main way to scale carbon removal globally.

With all these, the broader trend is clear. Carbon removal is moving from pilot projects to large-scale deployment. Companies are no longer testing the market. They are actively building it.

For now, Microsoft remains the dominant buyer. But its strategy is also creating space for others to follow. By securing supply early, the tech giant is helping to unlock a new phase of growth in climate technology.

The post Microsoft Inks Biggest-Ever U.S. Biochar Deal with Liferaft appeared first on Carbon Credits.

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Renewable Energy5 months ago

Renewable Energy5 months agoSending Progressive Philanthropist George Soros to Prison?