Disseminated on behalf of SolarBank Corporation

The US solar industry began 2025 with mixed signals. Wood Mackenzie’s US Solar Market Insight Q2 2025 reported an addition of 10.8 gigawatts-direct current (GWdc) in Q1. This marks a 7% drop from last year and a steep 43% fall from Q4 2024. Rising costs, trade tensions, and changing policies have strained project development and consumer demand.

Let’s study the various segments of solar and their performance in this quarter.

Utility-Scale Solar Slows Down but Stays Resilient

Utility-scale solar added 9 GWdc, slightly down from the previous quarter and Q1 2024. Still, it remained a strong segment. Texas led with 2.7 GWdc, nearly double Florida’s numbers. Both states focused heavily on large-scale solar projects. Notably, Texas, Florida, Ohio, Indiana, and California made up 65% of utility-scale additions.

Mixed Results Across Distributed Solar Segments

Residential solar struggled, adding only 1,106 MWdc – the lowest since Q3 2021. High interest rates, economic concerns, and uncertainty about solar tax credits held back homeowners. California topped the list with 255 MWdc installed, but this was the weakest output since Q3 2020.

On a positive note, commercial solar grew by 4% year-over-year to 486 MWdc, mainly due to California’s NEM 2.0 projects. However, it saw a seasonal dip of 28% compared to Q4 2024.

Community Solar Faces Headwinds but Holds Promise

Community solar projects, which are shared local installations, added 244 MWdc in Q1 2025. This was a sharp 22% year-over-year decline and a significant drop from Q4 2024’s surge. Maine and Massachusetts saw steep declines, while New York’s output fell slightly but still represented over half of the national community solar market.

Despite this downturn, installed capacity in 2025 is expected to exceed 2023 levels, reaching about 1.5 GWdc. New York and Illinois drive growth, with a community solar pipeline nearing 5 GWdc. However, grid interconnection delays and needed infrastructure upgrades slow progress.

Encouragingly, emerging markets may expand. Proposed legislation in several states could unlock over 1.5 GWdc of extra community solar capacity. Still, without new programs, national growth might stall. Wood Mac predicts a 6% average annual decline in community solar through 2030, but future legislative successes could change that.

Amid this uncertainty, SolarBank has remained resilient. The company recently announced a 2.4 MWdc community solar project in Nova Scotia.

SolarBank’s (SUUN) Nova Scotia Project Reflects Market Momentum

SolarBank Corporation (NASDAQ: SUUN) is going forward. The company recently announced the 2.4 MWdc Sydney Project in Nova Scotia, which will produce about 2,730 MWh of clean energy annually. It can potentially power 221 homes and offset nearly 1,900 tons of CO₂. The ground-mounted community solar power project, owned by AI Renewable Flow-Through Fund (“AI Renewable”), is a major step into Canada’s clean energy market.

The news lifted SolarBank’s stock (NASDAQ:SUUN) to $1.82 on June 16, up from $1.415 on June 13. The strong investor response highlights ongoing interest in clean energy opportunities (including those in jurisdictions outside the United States where government support remains strong), even as the broader market weathers policy and economic uncertainty.

SolarBank has developed over 100 MW of renewable energy projects in North America and has a pipeline of more than 1 gigawatt.

- In the U.S., the company completed over 50 MW of community solar installations. Now, it applies that experience to the Canadian market, where demand for clean energy is rising and government support is growing.

SolarBank North American Growth Strategy

Its portfolio includes community solar, utility-scale systems, virtual net metering projects, and behind-the-meter installations. This variety keeps the company agile, maximizes returns, and fosters low-risk, high-reward partnerships.

SEE MORE:

- SolarBank Expands Community Solar in New York with 14.4 MW Project

- The 7.2 MW North Main Community Solar Project in New York

How Shifting Trade Policy Is Disrupting US Solar Growth?

The US solar market is facing a tough trade and tariff environment in 2025. Earlier this year, the Trump administration added a 25% tariff on imports from Canada and Mexico starting March 4. While most solar panels aren’t imported from these countries, key parts like inverters and trackers are, which has pushed up production costs.

On top of that, aluminum tariffs under Section 232 increased from 10% to 25%, and later to 50% by June, making trackers and module frames even more expensive.

Tariffs on Chinese goods also soared, reaching 145% at one point due to fentanyl-related measures, before settling at 30% after a rollback deal on May 12. These changes have made the solar market more expensive and unpredictable.

- The US added 8.6 GW of new solar module manufacturing capacity in Q1 2025, bringing the total to 51 GW.

Upstream production remains sluggish. Only one new domestic cell plant, i.e., ES Foundry’s 1 GW facility in South Carolina, opened this year. There were no new launches in wafer or polysilicon production.

However, in these turbulent times, SolarBank has shown resilience. A recent collaboration with Qcells, involving the use of U.S.-manufactured solar modules, is one example of how the company is preparing for multiple future scenarios.

Why Investors Are Watching Closely?

Despite the hurdles, the US solar industry remains a key player in the country’s energy transition. In Q1 2025, solar accounted for 69% of all new power capacity added, showing its continued dominance. With long-term demand rising from data centers and domestic manufacturing, the sector’s growth potential remains strong.

To keep that momentum, the industry will need stable policies, steady investment, and better solutions for grid connections and supply chain issues.

The recent rebound in NASDAQ:SUUN stock reflects growing investor confidence. It signifies that SolarBank can be a potential long-term bet. While near-term challenges exist, the outlook for solar remains promising, and smart investors are taking note.

- READ MORE: SolarBank and CIM Group Announce $100M Financing to Power 97 MW of U.S. Renewable Energy Projects

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: None.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

Please read our Full RISKS and DISCLOSURE here.

The post US Solar Market Slows in 2025 – Here’s How SolarBank (NASDAQ:SUUN) Is Still Gaining Ground appeared first on Carbon Credits.

Most businesses have a clear picture of what happens inside their own operations. They track energy consumption, manage waste, and monitor the emissions produced on-site. What they often cannot see is everything that happens before a product reaches their facility, and everything that happens after it leaves.

![]()

Carbon Footprint

Texas-Based EnergyX’s Project Lonestar™ Signals a Turning Point for U.S. Lithium Supply

Energy Exploration Technologies, Inc. (EnergyX), led by CEO Teague Egan, has moved the United States closer to building a reliable domestic lithium supply chain. The company recently commissioned its Project Lonestar™ lithium demonstration facility in Texas, marking a key milestone in scaling direct lithium extraction (DLE) technologies.

This development comes at a time when lithium demand is rising sharply due to electric vehicles and energy storage systems. At the same time, the U.S. remains heavily dependent on foreign processing, particularly from China.

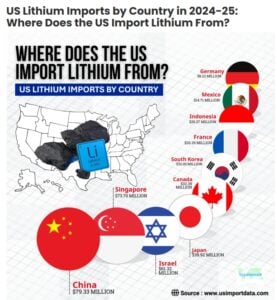

- According to the US import data and Lithium import data of the USA, the total value of US lithium imports reached $432.36 million in 2024, a 9% decline from the previous year.

- The total value of US lithium imports (cells & batteries) accounted for $205.29 million in the first 6 months of 2025.

Against this backdrop, EnergyX’s progress offers both technological validation and strategic value.

From Concept to Reality: How Project Lonestar™ Works

Project Lonestar™ is EnergyX’s first major lithium project in the United States and its second globally. The demonstration plant, located in the Smackover region spanning Texas and Arkansas, is now operational and uses industrial-grade systems rather than small pilot equipment.

- The facility produces around 250 metric tons per year of lithium carbonate equivalent (LCE).

While this output is modest compared to global supply, its importance lies in proving that EnergyX’s proprietary GET-Lit™ technology can efficiently extract lithium from brine. The plant processes locally sourced Smackover brine, a resource that has historically been underutilized despite its lithium potential.

Unlike traditional lithium production, which often relies on hard-rock mining or evaporation ponds, DLE technology directly extracts lithium from brine using advanced filtration and chemical processes. This reduces production time and may lower environmental impact.

- More importantly, the Lonestar™ plant can supply 5 to 25 tons of battery-grade lithium samples to customers.

This allows battery manufacturers to test and validate the material before committing to large-scale supply agreements.

Scaling Up: From Demonstration to Commercial Production

The demonstration plant is only the first phase of a much larger plan. EnergyX aims to scale Project Lonestar™ into a full commercial operation capable of producing 50,000 tonnes of LCE annually across two phases.

- The first phase alone targets 12,500 tonnes per year, which would already place it among the more significant lithium producers in the U.S.

- Significantly, the company has invested approximately $30 million in the demonstration facility, supported in part by a $5 million grant from the U.S. Department of Energy.

- For the full-scale project, EnergyX estimates total capital expenditure at around $1.05 billion.

Cost metrics suggest strong economic potential. The company estimates capital costs at roughly $21,000 per tonne of capacity and operating costs near $3,750 per tonne. If these figures hold at scale, the project could compete effectively with global lithium producers, particularly in a market where cost efficiency is becoming increasingly important.

Teague Egan, Founder & CEO of EnergyX, said,

“Bringing the biggest integrated DLE lithium demonstration plant online in the United States is a foundational milestone for EnergyX and for U.S. domestic lithium production in general. This facility not only validates the performance of our technology on an industrial scale under real-world conditions, but also establishes EnergyX as the lowest cost producer in the U.S. Ultimately this benefits all our customers who need large volumes of lithium for EV and ESS applications, as well as any lithium resource owners looking to implement best-in-class DLE technology whom we are happy to license to.”

Breaking the Bottleneck: Why U.S. Refining Matters

One of the biggest challenges facing the U.S. lithium sector is not resource availability but refining capacity. While lithium deposits exist across the country, most battery-grade lithium chemicals are processed overseas.

China dominates this segment, controlling roughly 70 to 75 percent of global lithium chemical conversion capacity. This concentration creates a structural dependency. Even when lithium is mined in the U.S. or allied countries, it is often shipped abroad for processing before returning as battery materials.

Project Lonestar™ directly addresses this gap. By integrating extraction and refining into a single domestic operation, EnergyX is working to build a complete “brine-to-battery” value chain within the United States. This approach could reduce reliance on foreign processing and improve supply chain resilience.

U.S. Senator Ted Cruz highlighted the project’s importance, noting that domestic lithium production supports both energy security and defense readiness, particularly for applications in advanced battery systems.

- CHECK: LIVE LITHIUM PRICES

The Current Landscape: Limited Supply, Big Ambitions

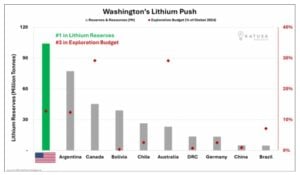

Investment is flowing into regions such as Nevada, North Carolina, and Arkansas. If even a portion of these reserves is converted into production, the U.S. could significantly reduce its reliance on imported lithium.

Active Resources and Future Potential

At present, U.S. lithium production remains relatively small. The only active large-scale operation is the Silver Peak Mine in Nevada, which produces between 5,000 and 10,000 tonnes of LCE annually, depending on market conditions.

However, several projects are in development that could significantly expand capacity. The Thacker Pass project, for example, is expected to produce around 40,000 tonnes per year in its first phase once operational later in the decade.

In addition, brine-based developments in the Smackover region aim to produce tens of thousands of tonnes annually, with long-term plans exceeding 100,000 tonnes across multiple sites.

These projects indicate a shift from a niche domestic industry to a more substantial production base. Still, timelines remain uncertain due to regulatory and financial challenges.

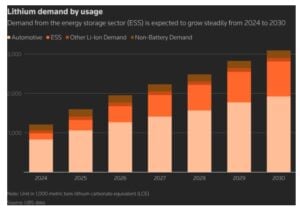

Demand Surge: Batteries Drive the Lithium Boom

The urgency to expand lithium production is driven by rapid growth in battery demand. Electric vehicles, renewable energy storage, and grid modernization are all increasing lithium consumption.

According to S&P Global, U.S. lithium demand is expected to grow at an average rate of 40 percent annually between 2024 and 2029. Canada is projected to see even faster growth, albeit from a smaller base, with demand rising by around 74 percent per year over the same period.

Globally, battery capacity is forecast to approach 4 terawatt-hours by 2030. This expansion highlights lithium’s central role in the clean energy transition. Without sufficient supply, battery production—and by extension, EV adoption—could face constraints.

Why Progress Takes Time

Turning lithium reserves into operational mines and processing facilities is not straightforward. Projects often face long permitting timelines, environmental scrutiny, and legal challenges. Financing can also be difficult, especially in a volatile commodity market.

Local opposition can further complicate development, particularly in areas with high environmental concerns. These factors can delay projects by several years, slowing the pace of expansion.

To address these barriers, the U.S. government is increasing its involvement through funding, policy support, and efforts to streamline permitting. The Department of Energy’s backing of EnergyX reflects a broader strategy to accelerate domestic critical mineral development.

Conclusion: A Strategic Shift in Motion

Project Lonestar™ represents a meaningful step toward reshaping the U.S. lithium landscape. By proving the viability of direct lithium extraction at an industrial scale, EnergyX has laid the groundwork for larger, commercially viable operations.

The project also aligns with national priorities around energy security, supply chain resilience, and clean energy transition. While challenges remain, the combination of technological innovation, government support, and rising demand creates a strong foundation for growth.

As the world moves toward electrification, lithium will remain at the center of the transition. Projects like Lonestar™ show that the United States is beginning to close the gap between resource potential and real-world production—one facility at a time.

The post Texas-Based EnergyX’s Project Lonestar™ Signals a Turning Point for U.S. Lithium Supply appeared first on Carbon Credits.

Analysis: Record wind and solar saved UK from gas imports worth £1bn in March 2026

China Briefing 2 April 2026: EV profits rise | Ming Yang rejected | Iran war

Which State Leads in Battery Energy Storage? It Depends on How You Measure.

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Renewable Energy5 months ago

Renewable Energy5 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits