Oklo, the California-based nuclear technology company recently announced that it has received clearance from the U.S. Department of Energy (DOE) and Idaho National Laboratory (INL) to proceed with site characterization for its first commercial fission power plant in Idaho.

The completion of the environmental compliance process is a significant milestone for Oklo as it can now initiate work for its fission power plant.

Jacob DeWitte, CEO and Co-Founder of Oklo noted,

“These approvals represent pivotal steps forward as we advance toward deploying the first commercial advanced fission plant. With this process complete, we can begin site characterization. Our unique business model of selling power directly to customers rather than power plants, combined with our early mover advantage, positions us to respond to a growing order book effectively and meet diverse energy needs across data centers, industrial processes, defense, and off-grid communities.”

Oklo Signed MOA with DOE for its Advanced Fission Power Plant

Oklo is dedicated to delivering clean, reliable, and affordable energy at a large scale. The company secured a site use permit in September through a Memorandum of Agreement with the DOE. This paved the way for its first commercial advanced fission power plant in Idaho, U.S. Interestingly, it’s the only advanced commercial fission company in the U.S. with a DOE site use permit.

The MOA will enable Oklo to conduct key site evaluations, including geotechnical studies, environmental surveys, and infrastructure planning. Additionally, it will also help maintain a schedule, manage costs, and support timely deployment.

On October 15, the company’s press release explained that they had also received DOE approval for its Conceptual Safety Design Report for the Aurora Fuel Fabrication Facility, which will recycle nuclear fuel material at Idaho National Laboratory (INL).

Subsequently, the Aurora Fuel Fabrication Facility will produce fuel for Oklo’s Aurora power plant at the Idaho National Laboratory (INL). It will essentially deploy high assay low enriched uranium recovered from spent Experimental Breeder Reactor-II fuel.

With a secured fuel supply, site use permit, and strong regulatory progress, Oklo is ready to launch its Aurora reactor. Its developed supply chain will further support the first deployment.

Now that the final clearance is approved by both the DOE and INL, CEO Jacob DeWitte is confident in the collaboration. He expects to bring Oklo’s first commercial nuclear fission plant online within the next few years.

From Waste to Power: Oklo’s Aurora Reactor Sets New Standards in Clean Energy

We discovered from World Nuclear News some unique features of the Aurora powerhouse, which are illustrated below:

- It is a fast neutron reactor that generates electricity by moving heat from its core to a supercritical carbon dioxide power conversion system.

- Designed to run on either fresh HALEU or recycled nuclear fuel, Oklo’s reactors can transform used nuclear fuel into clean energy.

- It can generate 15 MWe, scale up to 50 MWe, and operate for over a decade before needing refueling.

The fission pioneer also explained that they use advanced recycling techniques to keep transuranic materials together as fuel. This avoids the need to create pure material streams, which is a unique feature of fast reactors.

________________________________________________________________________

Uranium Royalty Corp.: Powering Decarbonization with Nuclear Efficiency

The only pure-play uranium royalty company is focused on capturing value from uranium price shifts through strategic investments. These include royalties, streams, debt, equity in uranium companies, and even physical uranium holdings. Notably, the company is growing with the rising demand for uranium.

- IEA revealed that in the U.S. alone, nuclear energy supplied roughly 19% of total electricity in 2022 and accounted for 55% of the nation’s carbon-free electricity.

- This nuclear output mitigated around 482 MMT of CO₂ emissions, which is equivalent to taking 107 million gasoline-powered vehicles off the roads.

More Power per Punch: Nuclear Energy Outshines Fossil Fuels

________________________________________________________________________

Why Oklo’s Advanced Nuclear Fission is Just One of A Kind

Oklo’s advanced fission powerhouse has unique advantages over traditional power generation technologies. In short clean, resilient, reliable, and affordable are the four features that truly make it one of a kind.

The reactors produce zero carbon emissions which makes them an environmentally friendly option. Oklo has stressed the fact that the energy density of nuclear fuel is a million times more than fossil fuels, hence it requires less land for mining. This attribute is significant for environmental preservation.

Moreover, unlike coal and gas plants that require frequent refueling, Oklo’s reactors can run for decades on a single load. This is how the nuclear company ensures long-term fuel reliability and independence.

Check out the landscape view of Oklo’s preferred site in Idaho

Image Source: Oklo Inc

Image Source: Oklo Inc

Talking about the cost-effective factor, the immense energy density of its fuel makes it an economical alternative to fossil fuels. Also, nuclear fuel has fewer resource requirements and lower operational costs.

Most importantly Oklo’s reactors deliver consistent, clean energy, and heat with minimal refueling—sometimes as infrequently as every 20 years. This long-term reliability supports steady power output that’s ideal for critical energy needs.

Thus, starting with Aurora, Oklo is developing unique kinds of next-generation reactors. Furthermore, with the collaboration with DOE and INL, the company is just on the right path to establishing nuclear fission as an abundant, affordable, and clean energy source across the world.

The post U.S. DOE Greenlights Oklo’s First Commercial Nuclear Fission Plant at Idaho appeared first on Carbon Credits.

Japan has taken a major step in clean shipping. A consortium led by Japan Engine Corporation and Kawasaki Heavy Industries has successfully tested the world’s first hydrogen-fueled main engine for a large commercial vessel.

This engine is designed for deep-sea cargo ships, not just small vessels. That makes it a key milestone. Most earlier hydrogen ship projects focused on ferries or short routes.

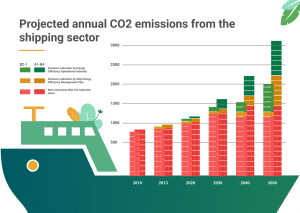

The 3% Problem: Shipping’s Emissions Challenge

The engine is a low-speed, two-stroke design. This is the standard for large ocean-going ships. It can run mainly on hydrogen fuel. In tests, it achieved about 95% hydrogen use at full load, showing stable performance.

The engine will be installed on a 17,500-deadweight-ton multipurpose vessel. The ship is expected to be delivered in 2027. It will then undergo a three-year demonstration period starting in 2028.

Shipping is a major source of global emissions. The sector produces about 2–3% of global greenhouse gas emissions, based on data from the International Maritime Organization (IMO).

Most ships today use heavy fuel oil or marine diesel. These fuels produce high emissions. As global trade grows, shipping emissions could increase without new solutions.

Hydrogen is one option. When used as a fuel, it produces no carbon dioxide at the point of use. This makes it attractive for long-term decarbonization.

However, scaling hydrogen for large ships has been difficult. Key challenges include fuel storage, engine design, and safety. Japan’s latest engine test shows that progress is being made.

How Hydrogen Engines Work in Large Vessels

Hydrogen-powered ships can use fuel cells or combustion engines. Japan’s new system uses combustion. This means hydrogen burns inside the engine, similar to diesel. This approach allows easier integration with existing ship systems. It also reduces the need for full redesigns of vessels.

The engine uses liquid hydrogen fuel and advanced injection systems. Engineers have focused on stable combustion and material strength. Hydrogen burns faster than traditional fuels, so precision is critical.

The project includes partners such as Mitsui O.S.K. Lines (MOL), Onomichi Dockyard, and ClassNK. These groups support design, safety checks, and future operations.

The move is part of Japan’s Green Innovation Fund. The Ministry of Economy, Trade, and Industry has funded the program with about 2 trillion yen to help the country reach carbon neutrality by 2050.

Japan’s Net Zero Strategy and Hydrogen Push

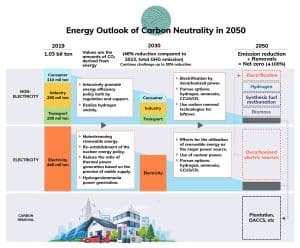

This hydrogen engine project fits into Japan’s broader climate strategy. The country has pledged to reach net-zero greenhouse gas emissions by 2050. This goal was announced by former Prime Minister Yoshihide Suga in 2020.

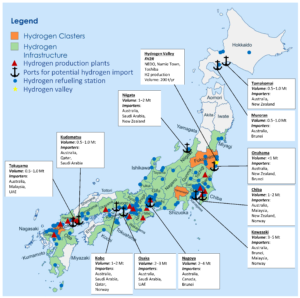

Japan sees hydrogen as a key part of its energy transition. Under its Basic Hydrogen Strategy, the government aims to expand hydrogen use across power, transport, and industry.

Japan plans to increase its hydrogen supply to 20 million tonnes per year by 2050, up from much lower current levels. The country is also investing in hydrogen imports, storage, and infrastructure.

Shipping plays a major role in this plan. Japan depends heavily on imports of energy and raw materials. Decarbonizing shipping is important for both climate and energy security.

- RELATED: Maritime Decarbonization: Japanese Shipping Giant NYK Partners with 1PointFive for DAC Credits

Projects like the hydrogen engine help link domestic policy with global action. They support Japan’s goal to build a full hydrogen value chain, from production to transport and end use.

Current Hydrogen Ferries in Operation

Japan has already started using hydrogen-powered ferries on real routes. One example is the Hanaria. This hybrid ship uses hydrogen fuel cells, lithium-ion batteries, and biodiesel. It began service in Kitakyushu in April 2024.

The ship can cut carbon dioxide emissions by 53% to 100% compared to regular vessels. It was built for a unit of Mitsui O.S.K. Lines and uses fuel cell technology developed with parts from Toyota.

Another example is the Mahoroba, built by Iwatani Corporation. This is a zero-emission hydrogen catamaran that can carry up to 150 passengers. It started commercial service in April 2025, transporting visitors to the Osaka-Kansai Expo.

In October 2025, the Tokyo Metropolitan Government agreed to bring the vessel to Tokyo Bay. It is expected to start operating there in fiscal year 2026. It will support environmental education and international events.

Japan has also invested in hydrogen transport systems. One example is the Suiso Frontier, which was launched to carry liquefied hydrogen across long distances. These efforts show that Japan is not only testing technology but also building the systems needed to scale hydrogen use globally.

From Ferries to Freighters: Scaling Hydrogen at Sea

Japan is part of a wider global shift. Many countries are testing hydrogen and other clean fuels for shipping.

For example, Norway launched the MF Hydra in 2023. Belgium introduced the Hydrotug 1 in 2024.

However, most of these vessels are small or operate on short routes. Japan’s project targets large cargo ships, which are more complex and more impactful for emissions.

Governments are also exploring hydrogen shipping corridors. These are planned routes where hydrogen-powered vessels can operate with proper fueling infrastructure. This global activity shows that hydrogen is moving from early testing to larger applications.

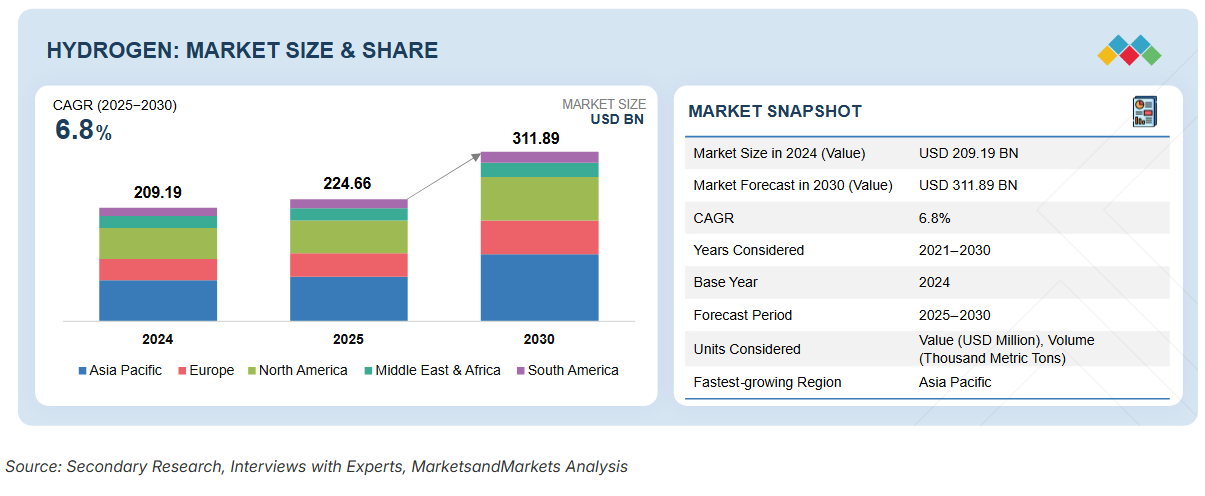

A $300B Hydrogen Market Meets Maritime Demand

The hydrogen economy is expanding quickly. Global demand is rising as industries look for low-carbon solutions.

Industry estimates suggest the global hydrogen market could exceed US$300 billion by 2030. Growth is driven by energy, transport, and industrial use.

In shipping, hydrogen competes with other fuels like ammonia and methanol. Each has strengths and challenges. Hydrogen stands out for its zero carbon emissions at the point of use.

Cost, Storage, and Infrastructure Barriers

Still, hydrogen has limits. Several barriers remain before hydrogen ships become common:

- High costs compared to traditional fuels,

- Limited supply of green hydrogen,

- Lack of port infrastructure, and

- Strict safety requirements.

Despite these issues, investment is growing. Governments and companies are funding research, pilot projects, and infrastructure.

Japan’s demonstration project will help address those gaps. The planned three-year trial will provide real-world data on performance, safety, and costs. If successful, hydrogen engines could become a practical option for large vessels. This would help reduce emissions from global shipping.

Can Hydrogen Power the Future of Global Trade?

Japan’s hydrogen engine test marks a key moment for the shipping industry. It shows that hydrogen can power not only small vessels but also large commercial ships.

The link to Japan’s net-zero strategy makes this development even more important. It connects national policy with global climate goals.

The coming years will shape how fast hydrogen shipping grows. With strong policy support and continued innovation, hydrogen could play a major role in building a low-carbon maritime sector.

The post Japan Unveils First Hydrogen Engine for Large Ships appeared first on Carbon Credits.

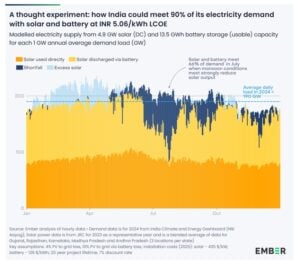

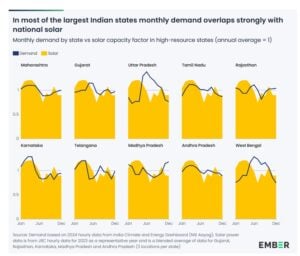

The post Solar Plus Batteries Can Meet 90% of India’s Electricity Needs, Says Ember appeared first on Carbon Credits.

Carbon Footprint

Bioleaching Breakthrough in Canada: How MIRARCO’s Pilot Facility Turns Mine Waste into Critical Minerals

A new wave of innovation is reshaping how the mining industry approaches waste. CBC News, Canada, reported that researchers in Sudbury, northern Ontario, are developing a bacteria-based technology called bioleaching, which uses naturally occurring microbes to extract valuable metals such as nickel, cobalt, and copper from old mine tailings.

Led by MIRARCO Mining Innovation, the team recently opened a pilot facility in October 2025 to scale up this process, aiming to transform mining waste into a source of critical minerals while cutting emissions, reducing environmental risks, and unlocking billions of dollars in untapped resources.

Sudbury Moves Toward Commercial Bioleaching

Sudbury has a long history of mining, leaving behind massive piles of tailings—the leftover rock and sediment from ore extraction. These materials still hold billions of dollars’ worth of metals, but until now, recovering them was difficult, energy-intensive, and expensive. The bioleaching technology changes that. By using bacteria that naturally digest minerals, scientists can release metals from waste rock without relying on harsh chemicals or high temperatures.

According to Nadia Mykytczuk, CEO of MIRARCO, the new pilot facility represents a shift toward sustainable mining. She precisely mentioned that,

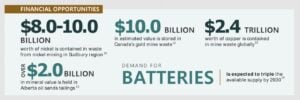

In Sudbury alone, the tailings contain $8 billion to $10 billion worth of nickel. With this facility, we are shaping a new era of mining innovation—one that focuses on clean technology, critical minerals, and preparing the workforce of tomorrow.

The facility connects research, industry, and community partners, creating a hub for applied research in bioleaching and bioprocessing.

Before moving to the new facility, MIRARCO operated within Laurentian University, and the long-standing partnership continues. The pilot center allows researchers to handle larger samples of mine waste and test how bioleaching works at a scale closer to industrial operations. This is essential for proving that the process can be commercially viable in Canada.

Bioleaching Breakthrough: Turning Tailings into Critical Minerals

- The process starts by grinding the mine tailings and mixing them with a nutrient-rich liquid. Scientists then introduce specialized bacteria into the mixture.

- These microbes feed on the minerals, producing chemical reactions that dissolve metals into the liquid.

- The resulting slurry moves through a series of reactors, where the process continues, and metals are eventually collected in a liquid form.

Early experiments are promising. Scientists at MIRARCO have noted that the process can recover 98–99 percent of nickel from the tested tailings. The value surpasses traditional methods that often leave large amounts of valuable minerals behind.

In separate research, scientists are growing and refining the bacteria. Different microbes target specific minerals. Some thrive in acidic conditions, ideal for breaking down sulfide tailings, while others focus on iron oxides or silicate rocks.

This flexibility allows scientists to extract not only common metals like nickel and copper but also rare earth elements and lithium, which are critical for batteries and renewable energy technology.

Environmental and Carbon Benefits

Traditional metal extraction uses energy-intensive methods, including high-temperature processing, chemical treatments, and heavy machinery. This approach produces substantial carbon emissions and generates more waste. Bioleaching operates at ambient temperature and pressure, reducing energy use by an estimated 30–40 percent.

It also tackles the challenge of storing mining waste. Canada produces around 650 million tons of mine tailings every year. Much of this material sits in ponds behind dams, which can be unstable and pose long-term environmental risks.

Significantly, tailings may generate acid or release metals into the environment, and dam failures can have serious consequences. The 2014 Mount Polley mine tailings dam failure incident in British Columbia is a stark reminder of these dangers.

By turning tailings into a source of metals, bioleaching reduces the volume of waste requiring storage, cutting both environmental risk and the legacy costs of old mining sites.

Overcoming Challenges

While promising, the technology is not without hurdles. Processing tailings can be costly, and the bacteria require careful monitoring and specific growth conditions. Scaling up from pilot operations to full commercial production will also need investment in infrastructure and specialized equipment.

Environmental experts, such as MiningWatch Canada, note that tailings can behave unpredictably. They may chemically react over time or shift physically, posing stability concerns. Effective containment and monitoring are critical to ensure the process remains safe at larger scales.

Despite these challenges, researchers are optimistic. Early pilot studies indicate that the bacterial method could recover 65–80 percent of minerals left behind by conventional processing. This is a significant improvement that makes further investment worthwhile.

Fueling Canada’s Clean Energy Future

The technology comes at a crucial time. Global demand for critical minerals is rising as electric vehicles, wind turbines, and solar panels become more widespread. Canada has identified 31 minerals essential for the energy transition, but many are currently imported from regions with supply risks. Bioleaching offers a way to unlock domestic resources while reducing dependence on imports.

The process could provide materials for electric vehicle batteries, grid infrastructure, and industrial applications. Lithium and cobalt can power EVs, rare earth elements like neodymium and dysprosium support wind turbines and other clean energy systems, and copper and nickel are essential for electrical grids.

By recovering these from tailings, Canada could strengthen its supply chains while reducing environmental impact.

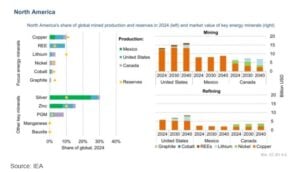

By 2040, the IEA expects the value of North America’s energy minerals to grow to around USD 30 billion for mining and USD 14 billion for refining. Mining growth will mainly come from copper in the United States and Mexico, and from lithium and nickel in Canada.

For refining, the region could make up about 4% of the global market, led by copper and lithium refining in the United States and copper and nickel refining in Canada.

Moving Toward Commercial Deployment

MIRARCO aims to transition from pilot testing to full-scale operations in the next two to three years. Globally, bioleaching is already in use at around 30 mining sites, but Canada has yet to deploy it commercially. The pilot facility in Sudbury is helping bridge that gap by testing continuous processing and demonstrating commercial viability.

Government support is also playing a key role. CBC further highlighted that funding through Canada’s Clean Technology Program and provincial innovation grants is helping advance research and development. The technology aligns with national goals to position Canada as a global leader in sustainable critical minerals production by 2030.

Overall, industry analysts predict bioextraction could become commercially viable within three to five years for specific minerals, with broader adoption following as operational experience grows.

The post Bioleaching Breakthrough in Canada: How MIRARCO’s Pilot Facility Turns Mine Waste into Critical Minerals appeared first on Carbon Credits.

Japan Unveils First Hydrogen Engine for Large Ships

Solar Plus Batteries Can Meet 90% of India’s Electricity Needs, Says Ember

Bioleaching Breakthrough in Canada: How MIRARCO’s Pilot Facility Turns Mine Waste into Critical Minerals

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Renewable Energy6 months ago

Renewable Energy6 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits