China and India accounted for 87% of the new coal-power capacity put into operation in the first half of 2025, whereas other regions continued to move away from coal.

These developments, highlighting a growing global divide between many countries phasing out coal power and a handful continuing to expand new capacity, are revealed in Global Energy Monitor’s latest Global Coal Plant Tracker results and reported here for the first time.

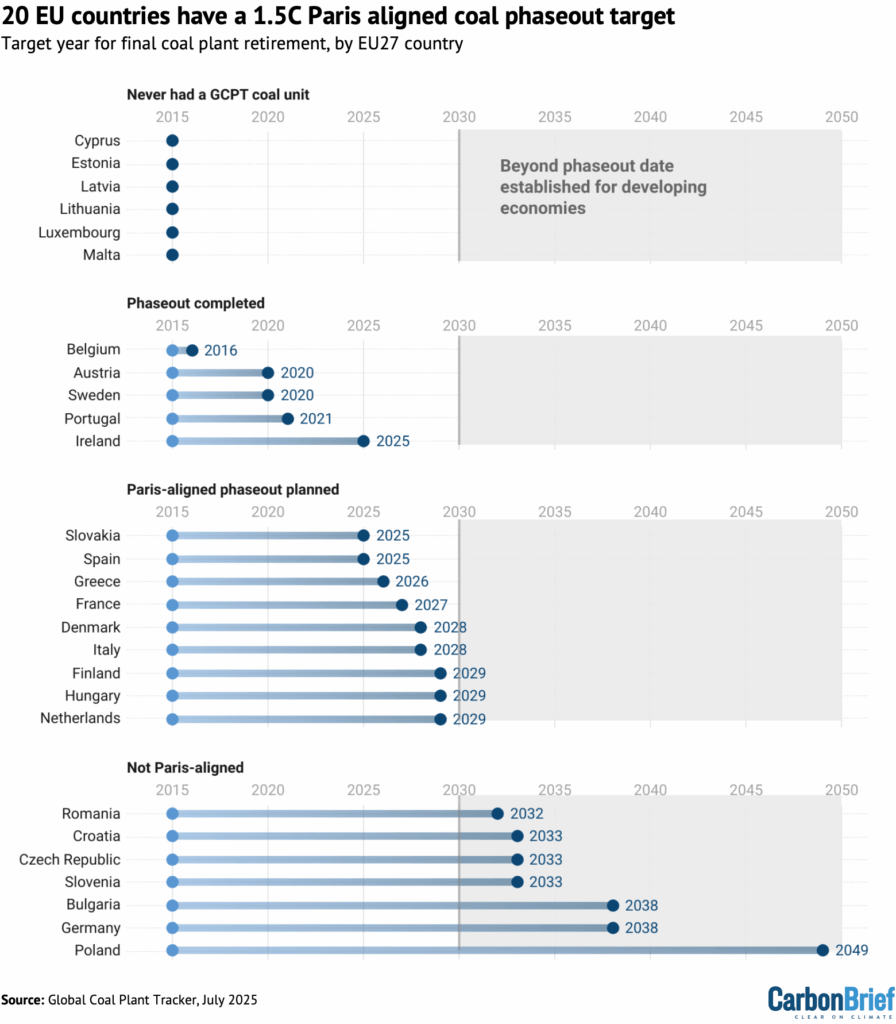

The results include Ireland becoming the fifth EU country to phase out coal power and Latin America becoming a region with zero active proposals for new coal capacity.

Meanwhile, the results show the US is on track to retire more coal capacity in 2025 than it did under the Biden administration last year, despite the efforts of the Trump White House.

Moreover, rather than follow the US in turning away from clean-energy leadership, other countries have continued their efforts to phase down coal power, with “just energy transition partnerships” (JETPs) advancing in Vietnam, Indonesia and South Africa during 2025 to date.

EU and Latin America pave the way for coal phaseout

The EU and Latin America are emerging as the global leaders in phasing out coal power, according to GEM’s analysis.

On the heels of the UK coal phaseout in 2024, Ireland stopped the use of coal power in June 2025, with nine EU countries expected to follow suit through 2029, including Spain, France and the Netherlands.

In total, all but three EU countries are planning to phase out coal by 2033, as shown in the chart below.

According to the International Energy Agency (IEA), coal power should be virtually phased out in advanced economies by 2030 and the rest of the world by 2040 to keep warming below 1.5C, as the Paris Agreement targets.

Development has also ceased in the region. No new coal plants have been proposed in the EU since 2018 and no coal plants have entered construction since 2019.

The coal phaseout in the EU and UK has been driven by a combination of country commitments and supporting policies and regulations, including air and carbon pollution limits on power plants, carbon pricing and policy support for clean-energy deployment.

Coal-power capacity retirements in the EU stalled for two years, following gas shortage concerns in the wake of Russia’s invasion of Ukraine, but they have since accelerated.

Coal capacity retired in the first half of 2025 (2.5GW) has already nearly exceeded all of 2023 (2.7GW) – with another 11GW planned for retirement in the EU by the end of the year.

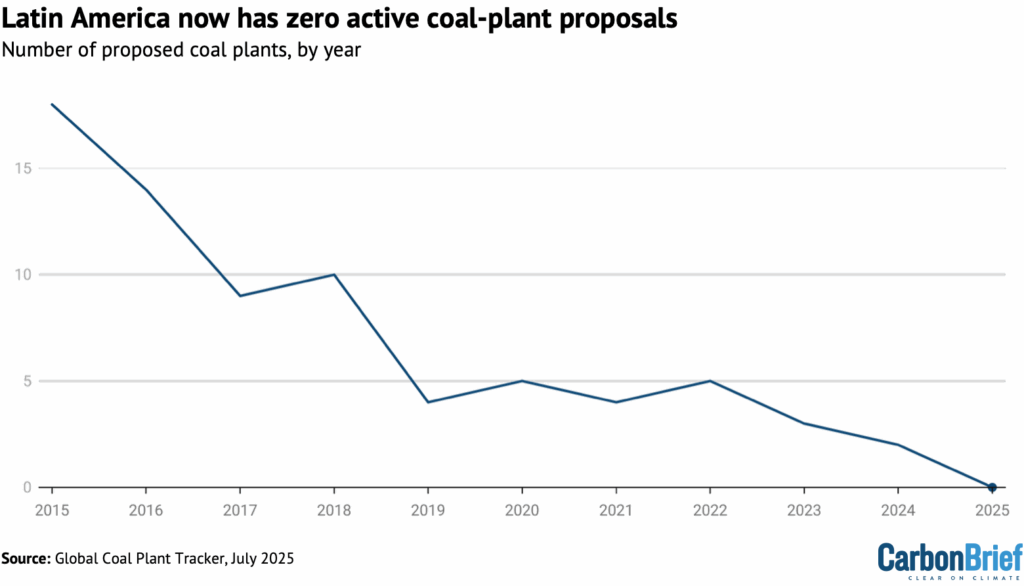

GEM data shows that, in Latin America, the shelving of two coal-plant proposals in Honduras and Brazil in 2025 has left the region with no new coal plants actively proposed, as shown in the chart below – a collapse of the 18 plants totalling 7.3GW of capacity proposed in 2015.

This followed the entry of Honduras into the Powering Past Coal Alliance (PPCA) in May and the lack of new coal plants proposed in Brazil’s 2025 national energy auctions, with a decrease in coal-power generation projected through 2034 in Brazil’s most recent 10-year energy plan.

Latin America is also nearly on track for a coal-power pathway that would be aligned with the 1.5C target of the Paris Agreement. More than 60% (10GW) of its 16.3GW of operating coal-power capacity is scheduled to come offline by 2040.

China and India continue to dominate

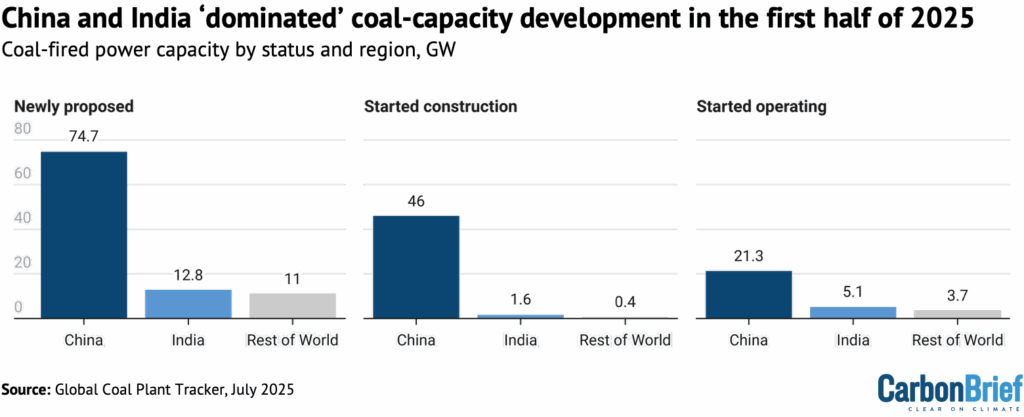

China and India dominated coal development in the first half of 2025, as the two countries had more new proposals, construction starts and coal plants commissioned than the rest of the world combined, GEM’s tracker shows.

As the chart below shows, there were 74.7GW and 12.8GW of newly proposed coal projects in China and India, respectively, in the first half of 2025, compared to just 11GW in the rest of the world.

Construction starts and restarts in China also reached 46GW, putting the country on track to match the record levels of 2024, when more than 97GW of coal-power plants began construction.

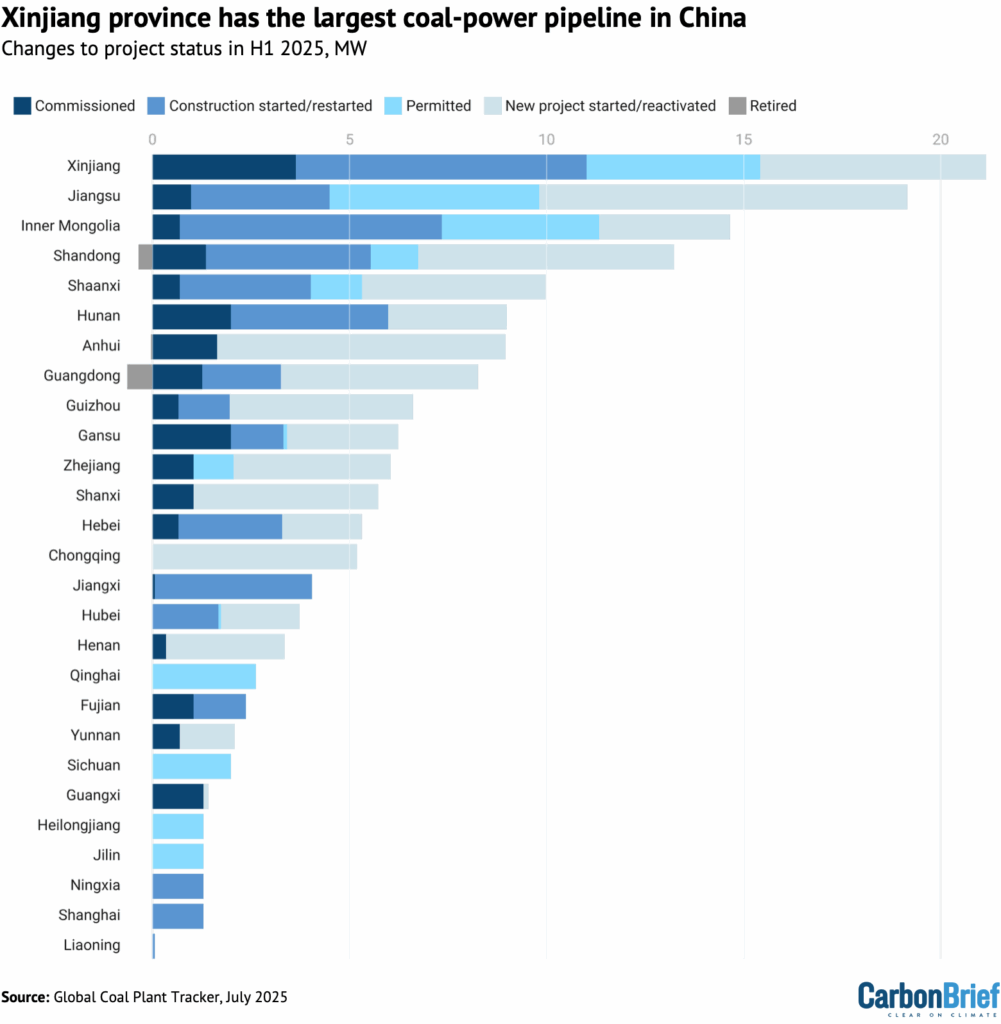

As discussed in GEM’s recent joint report with the Centre for Research on Energy and Clean Air (CREA), major coal-producing provinces, including Xinjiang, Inner Mongolia, Shandong and Shaanxi, are among the provinces commissioning and building the most new coal power, as shown in the chart below.

This expansion is backed by established permitting pathways, strong local power companies and a reliable flow of investment.

Yet, China has also been installing record amounts of clean energy, with more than 500GW of solar and wind power expected to come online in 2025. The increased generation from solar and wind power exceeded the increase in power demand in the first half of 2025, helping drive down China’s CO2 emissions by 1% compared to last year.

As clean energy has gained growing significance in China’s energy mix, more attention is being placed on renewables’ role in energy security and on coal power’s future as a flexible, supporting resource rather than as a primary generator.

Despite this narrative shift, coal remains deeply embedded in China’s power system, with little public discussion of its phasedown or eventual exit.

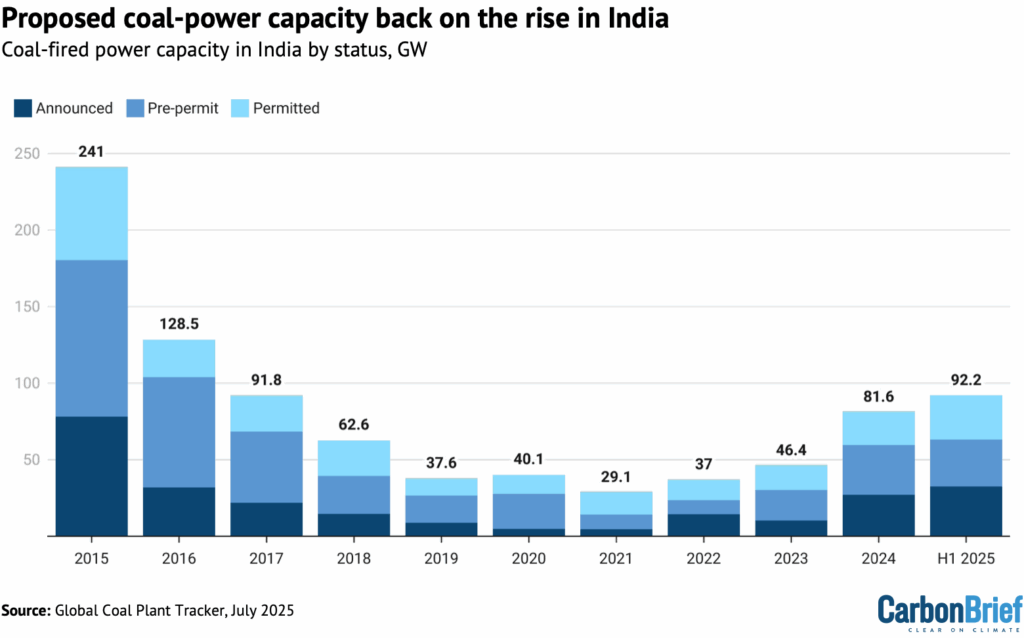

Coal-plant development is also on the rise in India, GEM’s tracker shows.

Commissioning of new coal plants in the country in H1 2025 (5.1GW) has already exceeded all of last year (4.2GW), as shown in the chart below.

Proposed coal-power capacity in India has also been on the rise, led by a record 38.4GW of coal-plant proposals in 2024 – driving up proposed coal capacity to over 92GW as of July 2025.

Retirements also remained sluggish in India, with 0.8GW retired in H1 2025 and just 0.2GW retired in 2024 and 2023, according to GEM’s tracker.

The decline follows 2023 guidance by India’s Central Electricity Authority (CEA) advising power utilities not to retire any thermal power capacity until 2030. In 2025, the country’s environment ministry again delayed long-pending sulfur dioxide regulations on coal plants.

Yet India also added more than 28GW of wind and solar power in 2025, a nearly 50% increase over the previous year. Despite the growth, the Indian government has stated that it is planning a coal expansion, with coal use not projected to peak until 2040, according to India’s Ministry of Coal.

In both China and India, coal retains its policy support, with clean energy framed, not as a replacement, but as a supplement – reinforcing a dual-track energy strategy that postpones difficult decisions on coal phaseout.

The US goes big on ageing coal plants

Like China and India, the US under President Donald Trump is also supporting coal power. Unlike China and India, however, the US has reversed course on clean energy in the first half of 2025.

During his tenure, former US president Joe Biden reached an agreement with other G7 nations to phase out coal power by 2035, offered incentives for clean energy under the Inflation Reduction Act (IRA) and moved to finalise pending power plant regulations – effectively helping replace the nation’s ageing coal plants with lower-cost solar and wind power while boosting domestic cleantech manufacturing.

The Trump administration has moved to derail Biden’s agenda by phasing out the clean energy tax credits, repealing coal plant regulations and slowing or halting solar and wind power permitting and financing.

It has also been using “emergency powers” to keep coal plants online, racking up $29m in costs to extend the life of Michigan’s Campbell plant through the summer – costs the utility is seeking to pass on to ratepayers for power the grid operator said was not needed.

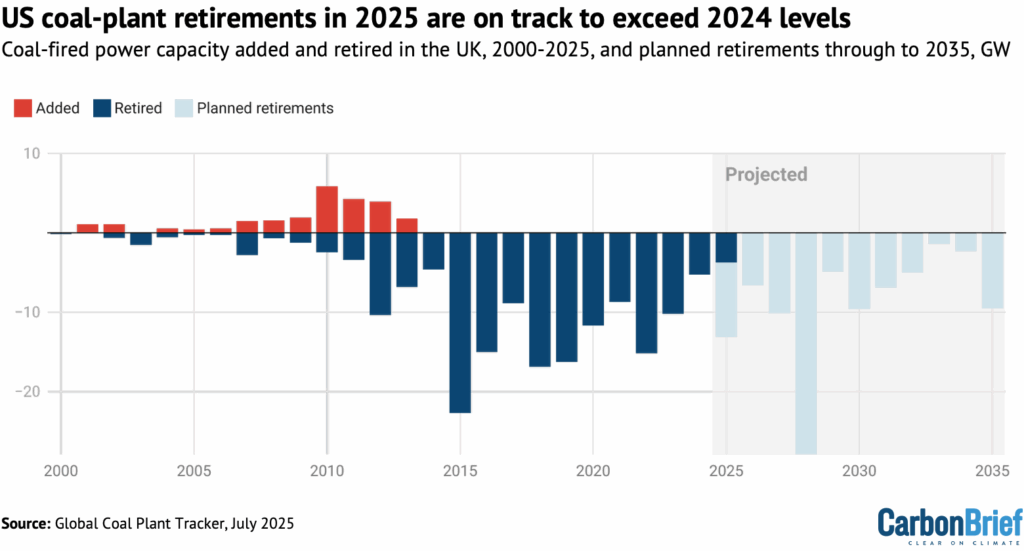

Despite the political support for coal, the US remains on track to retire more coal power in 2025 than in 2024, with 3.7GW retired as of July.

Whether this trend continues in an increasingly uncertain environment for clean energy remains to be seen, as plant closures are often part of long-term plans and economic considerations, usually extensively negotiated with state regulators and based on broader considerations than just current federal policy.

In all, US utilities are slated to close nearly 100GW of coal capacity by 2035, as shown in the chart below. By then, the average age of a US coal plant will be 55 years.

The US also saw a new coal plant proposal in H1 2025, bringing the total to three proposals according to GEM’s tracker, the most of any OECD country. All three plan to incorporate carbon capture and storage, although none have the necessary permits for construction.

Just energy transition partnerships advance despite hurdles

Despite delayed documentation, ongoing negotiations and the withdrawal of the US from International Partner Group participation, JETP agreements in Vietnam, Indonesia and South Africa are all continuing to progress.

In Vietnam, three clean-energy investment projects have officially penned financing agreements as of July 2025, getting the country one step closer to mobilising JETP capital.

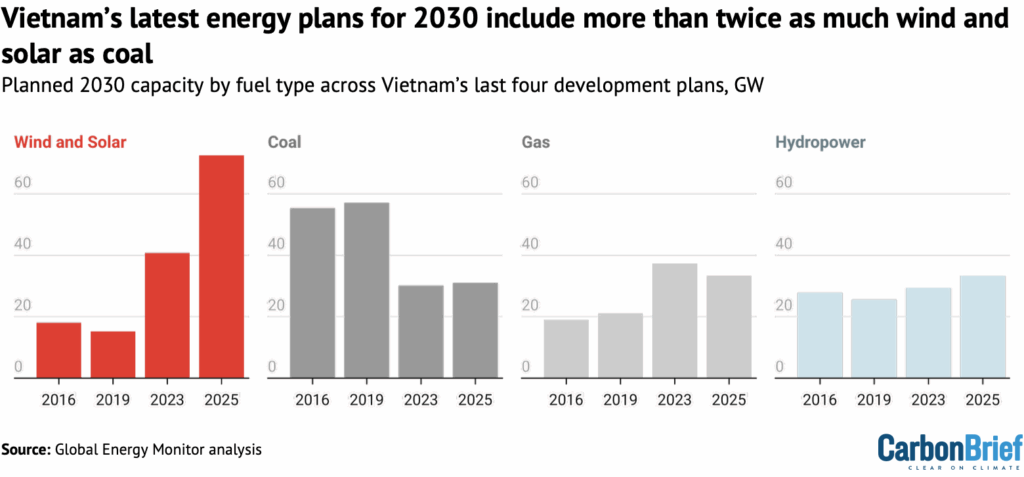

Just a few months prior, Vietnam released an adjustment to its latest power development plan, which featured substantial increases in projected wind and solar capacity and a modest increase in projected hydropower capacity.

However, the plan also includes a 1GW increase in projected coal power by 2030, as shown in the chart below.

The new figure for peak coal, 31.1GW, coincides with the interest from state-owned utility EVN to revive a coal plant previously considered to be cancelled.

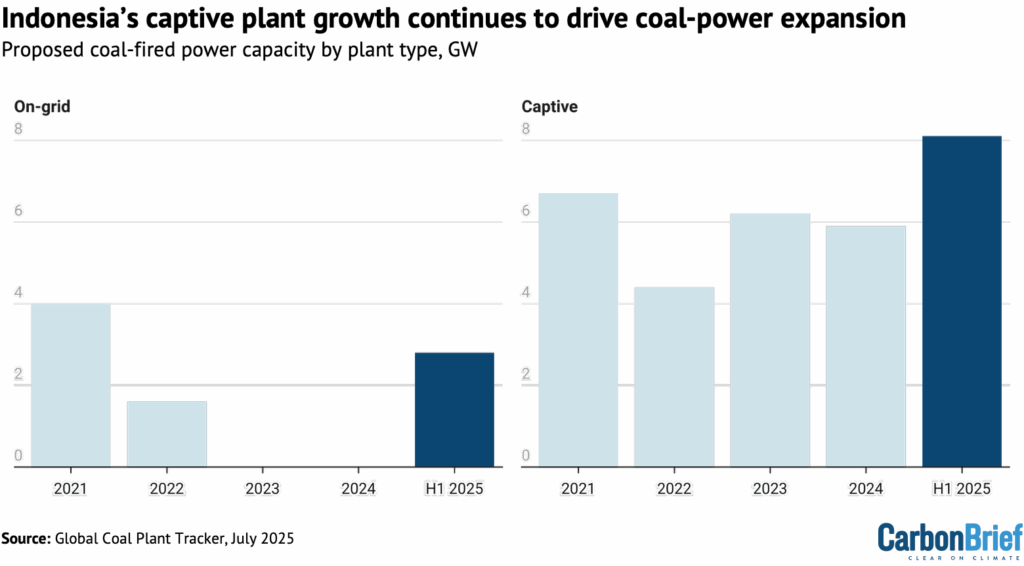

In Indonesia, the release of the latest electricity supply business plan (RUPTL 2025–2034) in May 2025 resulted in a spike in new and revived proposals for on-grid coal capacity. This was alongside the continued growth of off-grid, captive-coal plant proposals to power industrial areas, as GEM’s tracker shows.

Accounting for these captive-coal plants in Indonesia’s JETP documentation has presented a challenge, but Indonesia’s JETP secretariat has reiterated that updates to the country’s JETP comprehensive investment and policy plan are ongoing through the first six months of 2025 to address emissions from captive plants and incorporate efficiency targets.

Disparity remains between the government’s stated renewable energy ambitions and the reality of present advancements at the project level. Presidential regulation 112/2022 targets a 2050 national coal phaseout date in Indonesia and President Prabowo Subianto has more recently made overtures to an even faster 2040 coal phaseout.

Meanwhile, Indonesia’s proposed coal-power capacity grew by 5.1GW in H1 2025, to 17.1GW overall, as shown in the chart below.

In South Africa, the government has also reiterated its commitment to its JETP agreement. While Vietnam and Indonesia have substantial numbers of recently built coal plants and plants in continued development, South Africa operates a fleet of old, unreliable coal plants.

World Bank-linked funding for South Africa’s energy transition was approved in June 2025. While solidifying a climate investment fund, the plan also included the delayed closure of three coal plants that already average more than 50 years of age (Camden, Hendrina and Grootvlei).

All three countries are continuing down the dual paths of simultaneously extending coal’s lifetime and maintaining just energy transition commitments, banking on “all of the above” approaches and, ultimately, causing misalignment with JETP principles.

Yet, the continued progress of their just energy transition programs, despite global political and economic volatility, is a strong indicator that policy and planning priorities could soon align towards the phaseout of coal.

The post Guest post: China and India account for 87% of new coal-power capacity so far in 2025 appeared first on Carbon Brief.

Guest post: China and India account for 87% of new coal-power capacity so far in 2025

Farmers and fishermen in the Maldives have long relied on an ancient calendar to guide their daily lives.

The Nakaiy system divides the year into 27 distinct periods, each named after a star or constellation in the night sky.

Any one period in the calendar tells you about expected weather and tidal patterns, navigational routes, and fishing conditions. The Nakaiy was created through centuries of careful observation and local knowledge, passed down through families as an essential tool for survival.

But things are now changing. The climate crisis is leading to more extreme weather events across the Indian Ocean island nation and upending the Nakaiy calendar.

“When you go and speak to communities and ask them what kind of impacts they are facing, a lot of elders will tell you that the weather, it doesn’t follow the calendar anymore,” explained Aishath Reesha Suhail, a programme officer in the Maldives’ Ministry of Tourism and Environment.

As the effects of climate change worsen, it is a real prospect that the Nakaiy may be abandoned by local people, representing a major cultural loss to the Maldives.

‘Systemic and growing threat’

With extreme weather becoming the norm, communities are observing a domino effect of consequences in their everyday lives. The slow onset of heritage loss is now being seen across continents, but notably among small islands in remote parts of the ocean.

“Climate change represents a systemic and growing threat to cultural heritage worldwide,” a UNESCO spokesperson told Climate Home, adding that the World Heritage Committee has identified climate change as “one of the most significant long-term risks affecting properties across all regions.”

UNESCO, the UN body for education, science and culture, defines the loss of cultural heritage as “the erosion of traditional knowledge systems, craftsmanship, social practices and identity, particularly where communities are displaced or livelihoods disrupted”. A clear example is historical sites and even entire islands washed into the ocean as a result of rising sea levels and coastal erosion.

The Maldives is dealing with such a situation now. The Koagannu Cemetery is a 900-year-old resting place, located on the country’s southernmost atoll, a mere 50 metres from the shoreline. The monument’s intricate coral gravestones are being actively threatened by the encroaching Indian Ocean.

The government and local community have responded to this challenge with emergency protection measures. Sandbags and concrete structures have been installed along the coastline, complemented by large numbers of palm trees to create a seawall. A wider solution is ‘beach nourishment’, a common practice in the Maldives where sand from elsewhere is brought in to replace what has been lost through erosion. Taken together, these solutions have so far protected the cemetery.

Among the many issues climate change creates, cultural heritage is not always front of mind. In the Maldives, one of the main barriers people face is awareness. “Most of what we are dealing with relates to the erosion of our islands along with areas such as fisheries… but we are quite limited in our capacity to do something about it,“ Suhail said.

“We don’t understand the full breadth of the issue at present because we haven’t been able to do extensive research on the matter,” she added. However, assessing the extent of the damage – and how to respond effectively – is a key priority for the government, outlined in its latest climate plan, known as a Nationally Determined Contribution, and as part of its National Adaptation Plan process.

Fishing is at the core of the country’s culture and identity, employing thousands of people. Most dishes include fish – “we have it for breakfast, lunch and dinner,” Suhail noted – but the climate crisis and overfishing are shifting how and when communities can fish. Tuna makes up 98% of all fish caught in the Maldives, but warmer ocean temperatures are changing migratory patterns, pushing the species into deeper, colder waters.

As a critical economic and cultural resource, the government has outlined a range of solutions to protect the fisheries sector in its first Biennial Transparency Report to the UN. These include using real-time tracking data to improve the efficiency of fishing operations; investing in canneries to increase fish storage; and diversifying away from tuna through marine farming.

Culture and nature go hand-in-hand

The same pattern is playing out elsewhere.

Palau and the Maldives are not close to one another. The two states are separated by around 4,000 miles and sit in different corners of the ocean. But both are experiencing very similar climate challenges, based on their position as a set of scattered, low-lying islands surrounded by an imposing body of blue water.

In the same way as the Maldives, Palau’s cultural heritage is closely tied to “land, coastlines and traditional food systems,” according to Toni Soalabla, at the Palau Office of Climate Change.

“Many of the places that hold stories, history and identity of our communities are located along the coast and are increasingly exposed to erosion and sea level rise,” she said.

One of these places is Ngerutechei village, reportedly the oldest in Palau, and home to ancient stone paths and carvings. The village provides a glimpse into the past social values and culture of the people in this western Pacific nation.

As part of the development of Palau’s National Adaptation Plan, the government has worked with local leaders to identify similar sites of cultural significance. The plan encourages communities to use their own knowledge to create protective measures for these sites.

Climate change is also prompting communities to take up traditional land and food practices again. These include cultivating taro, a stable food source that has historically supported water, soil and food security on the islands.

“These systems developed over generations in response to local environmental conditions, so strengthening them today is both a climate adaptation measure and a way of maintaining cultural knowledge that might otherwise fade,” said Soalabla.

Cultural practices in Palau have developed alongside the natural ecosystems that people rely on to survive. It is within this context that researchers believe adaptation policies should be created. Recognising this relationship “can strengthen both community identity and environmental resilience at the same time”, according to Soalabla.

Heritage on the global stage

The issue of cultural loss has not gone unnoticed in international climate negotiations.

Small island states such as the Maldives have used their role at the UN to push for greater awareness and action, with some key successes.

In 2015, the Paris Agreement established a Global Goal on Adaptation (GGA) which recognised that countries needed to do something about climate change now and not later. However, it took six years before a framework and a set of adaptation targets were agreed at the UN climate summit in Glasgow to pursue this goal.

From this came the establishment of seven overall themes – from poverty eradication to access to health – to guide adaptation action and a set of around 60 indicators to measure progress against the targets.

World leaders invited to see Pacific climate destruction before COP31

Emilie Beauchamp, an adaptation specialist at the International Institute for Sustainable Development (IISD), said that “cultural heritage was highlighted as one of the global priorities [of the GGA Framework] and is one of the seven themes, so it is considered very important by the international community.”

The much-debated set of indicators, only finalised in Belém at last year’s COP30, include five related to cultural heritage with a focus on preserving cultural practices and important sites that are “guided by traditional knowledge, Indigenous Peoples’ knowledge and local knowledge systems”. A spokesperson for UNESCO said the inclusion of heritage indicators “marks an important recognition that climate impacts extend beyond economic losses”.

While critics said the set of final indicators was rushed through by the Brazilian presidency, they now serve as guidance for national governments that wish to implement plans to protect their common heritage. The missing piece of the puzzle remains how to finance these plans – something notably absent from the Belém text, which made clear that the adaptation indicators “do not create new financial obligations or commitments, nor liability or compensation”.

The lack of financial commitments proved disappointing for many small states grappling with how to prevent their cultural history from being entirely forgotten, especially at a time when adaptation finance remains below requirements. A recent UNEP report found that developing nations would need an estimated US$310 billion per year in 2035 to adapt to climate change, while current public financing was around $26 billion.

At these low levels “only a small percentage of what the framework outlines could be implemented,” according to Beauchamp.

The challenge of cultural heritage

When looking at low-lying islands on a map, they can appear as specks of land amid a vast ocean. Many of the stories from these remote places go unnoticed. But the specks represent millennia of human culture that is slowly being lost to the ocean.

While the international community has now recognised the problem and solutions exist, the recurring issue of scarce finance may prevent governments from taking sustained action. Island communities have already been forced to move home as sea levels rise, leaving behind their cultural connections to a place.

The value of any cultural asset, or of human heritage, can be judged by how it is engaged with over generations. Without human intervention, many historical sites, language, cuisine and other local customs would become a forgotten part of history. The rapid onset of climate change brings the role of cultural heritage into sharp relief, challenging communities to decide in real time what they value, what deserves saving, and how to achieve that.

Stories of cultural loss are not confined to small islands but it is here where the challenge is presenting most acutely. The experiences of these vulnerable nations in protecting their heritage will provide the litmus test for effective adaptation responses elsewhere.

Adam Wentworth is a freelance writer based in Brighton, UK.

(Main image: The Isdhoo Havitha is an ancient Buddhist monastery in the Maldives, located moments from the shoreline. Photo: Ashwa Faheem)

The post Island nations fight to save cultural heritage from climate change appeared first on Climate Home News.

Island nations fight to save cultural heritage from climate change

The invasive emerald ash borer, native to northeast Asia, has spread to 37 states over the past quarter century, killing nearly all of the ash trees it infests. But in Maine, a coalition of basketmakers, scientists and government officials are plotting a future for their trees.

Each strip of wood in Richard Silliboy’s hands started as a year of an ash tree’s life.

Climate Change

Toxic Ocean Crisis in Papua New Guinea Sparks Mass Marine Die-Off and Public Health Emergency

Thousands of dead fish are washing ashore and people are falling ill too, as officials investigate possible sources of contamination.

It started in December, when dead fish began washing ashore New Ireland—a mountainous island in Papua New Guinea’s New Ireland Province, flanked by the Pacific Ocean and the Bismarck Sea.

Toxic Ocean Crisis in Papua New Guinea Sparks Mass Marine Die-Off and Public Health Emergency

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Renewable Energy5 months ago

Renewable Energy5 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits