Nuclear fusion energy is clean, safe, and sustainable. It combines lighter atoms to release vast energy without high-level radioactive waste. Commonwealth Fusion Systems (CFS), the Massachusetts-based fusion giant aims to revolutionize the clean-energy space by generating infinite carbon-free power with its flagship fusion project SPARC. Since its inception in 2018, the company has secured over $2 billion in funding, which makes it the world’s largest private fusion company.

Recently CFS announced that it has built and tested a groundbreaking electromagnet, the Central Solenoid Model Coil (CSMC). This scientific innovation brings the company closer to using clean fusion energy for the grid.

Commonwealth Fusion Systems’ Mighty Magnet Makes Fusion Feasible

The CSMC test, combined with the already tested (in 2021) and successfully existing Toroidal Field Model Coil (TFMC), proves the functionality of two essential high-temperature superconducting (HTS) magnets. These magnets are crucial for SPARC, the tokamak machine which is designed to demonstrate net fusion energy.

Additionally, the TFMC validated magnets for steady electrical currents, while the CSMC confirmed the capability for pulsed electrical currents.

Brandon Sorbom, Co-Founder and Chief Science Officer noted,

“This is an important milestone on the road to commercialization. When we hit the button and put current through the magnet, it performed like a champ and hit all its major test objectives. The fact that our team was able to develop this technology from benchtop to a fully integrated, at-scale superconducting magnet in just a couple of years is huge.”

The press release also mentioned that CFS developed PIT VIPER which is an advanced HTS cable technology. It aids in powering SPARC’s central solenoid (CS) and poloidal field (PF) magnets. PIT VIPER’s innovative design minimizes heating during rapid current changes, enabling high-performance magnets.

The CSMC Model

source: CFS

Key test results from the Central Solenoid Model Coil include:

- Handling electrical currents up to 50,000 amps, enough to power 250 modern homes.

- Generating a magnetic field of 5.7 teslas—100,000 times Earth’s magnetic strength.

- Releasing energy rapidly at 4 teslas per second, validating SPARC magnet behavior.

- Storing a record 3.7 megajoules of energy, equivalent to five pickup trucks traveling at 60 mph.

- Using fiber optics to detect overheating events, ensuring magnet safety.

CFS and MIT: Partners in Fusion Progress

The successful CSMC test showcases CFS’ leadership in magnet technology. The company scaled up PIT VIPER cable production and demonstrated its ability to design and operate magnets under SPARC-like conditions.

Experts from CFS and the Massachusetts Institute of Technology (MIT) collaborated on this project and conducted the tests at MIT’s Plasma Science & Fusion Center (PSFC). Moving on, CFS plans to produce the first plasma with SPARC in 2026 and achieve net energy soon after. The company’s first power plant, ARC, is expected to deliver electricity to the grid in the early 2030s.

Ted Golfinopoulos, one of the principal investigators at MIT for the CSMC project said,

“Where the mission of the TFMC was to demonstrate a steady strength, the CSMC needed to demonstrate speed.”

He also hailed the collective effort of the amazing team by remarking,

“Hundreds of hands have touched this coil, from its inception on the drafting board to its long and complicated test program. The ingenuity, perseverance, and heart shown by this close-knit team was as impressive as the coil that sprang from their labors.”

Notably, the U.S. Department of Energy’s Advanced Research Projects Agency–Energy (ARPA–E) and Fusion Energy Sciences (FES) programs supported the innovation.

Commonwealth Fusion Systems Aims to Transform Coal Plants with Nuclear Fusion

From a recent Bloomberg report, we discovered that Tokamak designs were first developed in the 1950s and they already demonstrated the ability to trigger fusion reactions. However, their practical and commercial viability is still questionable. This is because these traditional electromagnets require a humongous amount of power to shift them from scientific experiments to practical energy solutions.

CFS’s blueprint electromagnets that we described earlier can keep the plasma under control and maintain the continuity of the fusion reaction. This is why Bob Mumgaard, CEO of Commonwealth Fusion Systems expressed his satisfaction, saying that this was the last major technology hurdle they needed to clear.

The report further highlighted CFS’s plans to replace fossil fuel boilers with fusion power by harnessing the same energy source as the sun. The company is already assessing old coal and natural gas plant sites as potential locations for building its first commercial fusion systems. However, their demonstration device is still in the developmental phase.

Nonetheless, CFS is confident of its success and the shift from fossil fuels to clean, carbon-free energy using fusion.

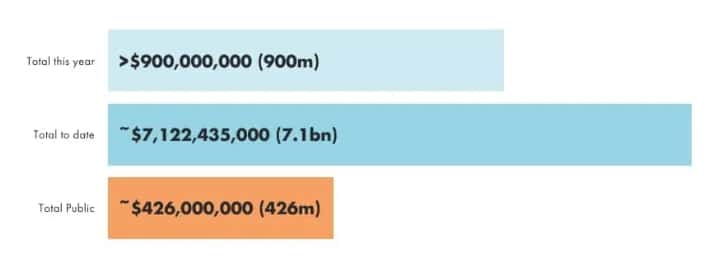

The recently published Global Fusion Industry Report reveals a rapidly intensifying race to commercialize fusion energy. Currently, 45 companies are advancing diverse technologies and have collectively raised over $7 billion. Public-private partnerships are playing a pivotal role in the fusion development process and have brought a remarkable 50% increase in funding.

The investment figures are shown below:

Source: 2024 Global Fusion Industry Report

Industry reports and expert opinions confirm that the fusion industry is still in its development phase. Building commercial nuclear fusion systems will take time, but progress is accelerating with increased investments and scientific breakthroughs. In this space, Commonwealth Fusion Systems is driving the transition toward a global clean energy future with its groundbreaking innovations.

Sources:

- Commonwealth Fusion Systems Magnet Success Propels Fusion Energy Toward the Grid | Commonwealth Fusion Systems

- Nuclear Fusion Leader Wants to Build on Site of Old Coal Plants – BNN Bloomberg

The post Commonwealth Fusion Systems’ Innovative Magnet Powers Fusion to the Grid appeared first on Carbon Credits.

Key takeaways

- SBTi is the default reference point for corporate climate action: 51% of Fortune Global 500 companies now hold net-zero targets, up from 8% in 2020, and over 11,000 organizations worldwide have SBTi-validated targets.

- Net Zero Standard V2 redefines climate leadership as reducing emissions and mitigating ongoing emissions, not reduction alone.

- The new standard adds flexibility through five-year cycles, a “best efforts” standard, and an Asset Transition Method for companies whose path to net-zero doesn’t fit a straight-line trajectory.

- Voluntary carbon credits are formally recognized for the first time, with reduction and removal credits accepted from 2027, and removals required from 2035.

- Companies with 2030 targets keep using V1 for their current cycle and move to V2 in 2028; companies without targets can start using V2 on February 1, 2027.

Why every business needs to understand the SBTi Net-Zero Standard revision

The Science Based Targets initiative (SBTi) has become the default reference point for credible corporate climate action. Net-zero targets are now held by 51% of Fortune Global 500 (FG500) companies, up dramatically from just 8% in 2020, and more than 11,000 organizations worldwide have set SBTi-validated targets.

However, SBTi’s influence extends well beyond the companies formally participating in the program. Every business in the value chain of an SBTi participant will have to reduce its own carbon emissions, and businesses that aren’t SBTi participants themselves still look to the program for guidance on climate action.

In short, SBTi gives every business a credible blueprint for climate action, and companies that follow its principles can pursue climate action with confidence, whether or not they’re formally part of the program.

How will the Net Zero Standard revision affect business climate action?

SBTi participation is expected to grow. Despite strong target-setting participation among the F500, only 17% of companies use the SBTi Net Zero Standard V1 beyond target setting, largely because its rules have been seen as too rigid to apply in practice. Much of the Net Zero Standard revision has focused on creating more flexibility to enable higher participation. Medium and small businesses will also increasingly feel pressure for climate action, since SBTi mandates that its participants reduce carbon emissions across their value chains.

Net Zero Standard V2 also redefines climate leadership: leading climate action now means reducing emissions and mitigating ongoing emissions. Reducing your own emissions while ignoring the emissions you continue to release along the way is no longer considered leadership. Supporting voluntary carbon projects with high-integrity carbon credits is now backed by the leading authority on corporate climate action.

What lessons shaped the Net Zero Standard V2 revision?

The revision reflects a few learnings about what actually drives climate progress, and how SBTi built those lessons into the new standard.

| Net Zero Standard V1 Learnings | Net Zero Standard V2 Implementation |

|---|---|

| Making real short-term progress is more important and more difficult than making big long-term promises | Focus on short-term climate progress |

| Every company has a different path to net zero that doesn’t always fit generalized net-zero rules | Create asset transition plans based on each company’s unique asset lifecycles and capital planning |

| We need to mitigate our ongoing emissions to keep global carbon emissions in check | Reduce global carbon emissions by financing voluntary carbon projects with high-integrity carbon credits |

What are the key changes between the old and new Net Zero Standard?

Both versions of the standard are grounded in net-zero by 2050. However, the old standard treated climate leadership as simply reducing emissions, expected a long-term commitment to net zero, based emission reduction targets on generalized net-zero goals, revoked status from companies that fell behind on targets, and ignored voluntary carbon projects entirely.

The new standard treats climate leadership as reducing emissions and mitigating ongoing emissions. It shifts the focus to short-term progress through five-year cycles, and it bases emission reduction targets on both the net-zero goal and a company’s own asset decarbonization plan. A new Asset Transition Method lets companies set decarbonization targets through asset plans with committed, verifiable steps; an ambitious but achievable path based on a company’s starting point, financial resources, and technology, with multiple pathways to reflect the unique opportunities and constraints of different industries and companies.

Crucially, the new standard moves to a “best efforts” basis that creates real flexibility on progress against targets. Businesses that miss their targets can keep their status if they’ve used “every lever” within their control, and minimum progress rules will be set out in the SBTi Assurance Manual.

Finally, the new standard formally uses voluntary carbon projects to mitigate ongoing emissions. From 2027 through 2034, this mitigation is recognized, and both carbon reduction and removal credits are accepted. From 2035 forward, mitigation with carbon removal credits becomes required, with durability matching between the removal and the emission it offsets.

| Old Net Zero Standard | New Net Zero Standard |

|---|---|

| Grounded in net-zero by 2050 | Grounded in net-zero by 2050 |

| Climate leadership is reducing emissions | Climate leadership is reducing emissions and mitigating ongoing emissions |

| Make a long-term commitment to net-zero | Focus on short-term progress in 5-year cycles |

| Emission reduction targets are based on net-zero goal |

|

| Businesses who fall behind targets lose status |

|

| Ignores voluntary carbon projects |

|

When does the new Net Zero Standard take effect?

Companies with existing 2030 targets should continue using the old Net Zero Standard for their current cycle, and start using the new Net Zero Standard in 2028 to set targets for the next cycle (2030–2035).

Companies that don’t yet have targets can use the new Net Zero Standard starting February 1, 2027.

What are SBTi’s Category A and Category B companies?

The new Net Zero Standard splits companies into two categories, with different requirements attached to each.

Category A covers large companies from all countries and medium-sized companies from high-income countries. A company from any country qualifies if it meets at least one of: net turnover of €450 million or more, or 1,000 or more full-time employees. A company from a high-income country qualifies if its Scope 1 and 2 emissions are 10,000 tCO2e or more, or if it meets at least two of: balance sheet of €25 million or more, net turnover of €50 million or more, or 250 or more full-time employees.

Category B covers small companies from all countries and medium-sized companies from lower-income countries.

How do Scope 1 targets work under Net Zero Standard V2?

Scope 1 targets aim to transition companies to net-zero direct emissions by 2050 or sooner, and companies can choose from three approaches.

- Absolute emissions reduction follows a straight-line emissions trajectory from the target base year to the net-zero year.

- Emissions intensity reduction lets companies follow sector-specific pathways designed to reflect the reduction opportunities available in sectors like steel, cement, or chemicals.

- Asset transition is designed for companies whose capital stock turnover doesn’t follow a linear or sector pathway. These companies design a transition plan to operate existing assets efficiently and replace them with low-carbon assets, using predetermined milestones.

How do Scope 2 targets work under Net Zero Standard V2?

Scope 2 targets address emissions from purchased electricity through three pathways:

- Reducing electricity consumption,

- Reducing grid consumption by installing onsite or direct-line offsite clean energy generation, and

- Cleaning up the regional grid using market-based tools like PPAs, RECs, and GOs that drive clean energy development.

V2 introduces a dual Scope 2 framework requiring two separate targets, with an overall goal of 100% low-carbon electricity by 2040.

The location-based target addresses the carbon intensity of a company’s physical power use, and requires companies to show that their grid consumption is falling and/or that their physical grid use is getting cleaner; in other words, that their market-based solutions are actually making the grid cleaner.

The market-based (or zero-carbon electricity) target tracks a company’s use of low-carbon power generation contracts and Energy Attribute Certificates. It requires geographical matching of these certificates with electricity consumption based on deliverability regions (grid regions); annual matching is allowed, though hourly matching is encouraged. Category A companies with large electricity loads must report the percentage of their Scope 2 electricity consumption matched with low-carbon attributes on an hourly basis, and there’s an optional recognition framework for companies that meet hourly matching thresholds.

How do Scope 3 targets work under Net Zero Standard V2?

Scope 3 targets share the same 2050-or-sooner net-zero goal, but companies set near-term targets only for material emissions sources in their value chain and areas where they have real influence. Long-term Scope 3 targets are generally not required.

Limited, justified exclusions are allowed for near-term targets, including categories that individually account for less than 5% of total Scope 3 emissions, and activities where a company lacks practical influence, like leased assets it doesn’t operationally control, or the processing of sold products. Optional exclusions are also available in specific categories.

Companies can choose from three approaches to near-term Scope 3 targets:

- An overarching emissions reduction target, which follows a linear contraction of emissions from the base year to residual emissions of 10% or less by 2050 or sooner;

- An overarching supplier/customer alignment target, benchmarked against a growing share of tier 1 suppliers and customers reaching net-zero by 2050 or sooner; or

- A category- or activity-specific target, tailored for companies with concentrated emissions in particular Scope 3 categories or high-emitting activities.

What is “ongoing emissions mitigation” under the new SBTi standard?

This is one of the most significant additions in Net Zero Standard V2. Accelerated climate contributions are needed to help the world achieve climate objectives, limit temperature overshoot, mitigate transition risks, and support the scale-up of climate solutions, and V2 formally recognizes that. Ongoing emissions mitigation runs as a parallel track to companies also reducing their own emissions.

The framework is initially voluntary, with recognition available at three contribution levels to encourage early action.

- Engaged companies address more than 1% of total Scope 1, 2, and 3 emissions.

- Advanced companies address more than 10% of total Scope 1, 2, and 3 emissions, including 100% of Scope 1 and 2 emissions.

- Leadership companies address 100% of total Scope 1, 2, and 3 emissions with a contribution budget of $80/tCO2e.

Carbon credits used for this purpose have to meet certain quality standards. They must be ex-post (issued after the mitigation has actually occurred), independently third-party-assured, emissions reductions or removals, measured in tCO2e, that occur within five years prior to the reporting year. They must be sourced from outside the company’s own value chain. Further minimum criteria will be set to align with high-integrity frameworks, with additional details on the recognition program expected in the second half of 2026.

Starting in 2035, carbon removals become mandatory for Category A companies. From that point, the carbon removal coverage requirement rises linearly from 1% of Scope 1–3 emissions to 100% by a company’s net-zero year. Within that, 10% of long-lived GHG emissions must specifically be covered by durable removals, also rising linearly to 100% by the net-zero year.

How must companies neutralize residual emissions?

At a company’s net-zero target year and thereafter, it must reduce its Scope 1, 2, and 3 emissions to zero or to residual levels, and neutralize all residual emissions using eligible carbon removals. Those removals have to meet two conditions: they must occur within the same reporting period as the residual emissions they’re neutralizing, and long-lived GHGs must be neutralized with long-lived removals, matching the durability of the removal to the atmospheric lifetime of the emission being addressed.

What is the SBTi implementation hierarchy?

Net Zero Standard V2 also lays out how companies should prioritize their actions for credible target delivery, in three tiers.

- Direct actions, at the activity level, are actions that reduce emissions at the source within a company’s own operations and value chain; things like efficiency improvements, fuel switching, and engaging suppliers and customers to reduce their emissions.

- Actions within shared systems, or activity pools that reduce the emissions of shared systems like electricity or gas grids. This includes market instruments that convey low-carbon attributes, such as PPAs, RECs, and GOs, all of which must meet minimum integrity criteria that SBTi will elaborate on in future guidance.

- Sector-level actions relate to the same type of activity occurring in a relevant geography or system, in a way that meaningfully reduces the emissions a company is responsible for.

How Terrapass helps businesses meet the new SBTi standard

As the rules around carbon credits become more rigorous, the quality of the credits behind them matters more than ever. Terrapass has expanded our global network of carbon projects: more project types, locations, prices, ICVCM CCPs, and UN SDGs, spanning super-pollutant destruction, nature-based solutions, and durable removals. We offer Green-e® Climate Certification and we only source from third-party-verified projects on ICVCM-Eligible registries.

We also help clients with impact beyond carbon: EACs, RECs, and GOs including Green-e® Certified credits that support leading renewable energy projects; water credits that support water restoration projects; and custom environmental product needs like RNG and SAF. Wherever your organization is on its sustainability journey, we help clients around the world address climate risk, advance their environmental and social goals, and get the most out of their sustainability budgets.

FAQ: SBTi Net-Zero Standard revision

What is the SBTi Net-Zero Standard?

It’s the framework the Science Based Targets initiative publishes for companies that want validated, credible net-zero targets tied to limiting global warming.

What is changing in the SBTi Net Zero Standard V2 revision?

The biggest changes are more flexibility (five-year cycles and a “best efforts” standard), a new Asset Transition Method for companies whose emissions don’t follow a straight-line path, and formal recognition of voluntary carbon credits for mitigating ongoing emissions.

When do companies need to switch to the new SBTi standard?

If your company already has 2030 targets, you keep using V1 for your current cycle and move to V2 in 2028. If you don’t have targets yet, you can start using V2 as of February 1, 2027.

Can companies use carbon credits to meet SBTi targets?

They can. Under V2, high-integrity carbon reduction and removal credits count toward mitigating ongoing emissions from 2027 through 2034. Starting in 2035, only removal credits count, and they need to be durability-matched to the emissions they offset.

What’s the difference between Category A and Category B companies under SBTi?

Category A is large companies everywhere plus medium-sized companies in high-income countries, based on thresholds like revenue, headcount, or emissions. Category B is small companies everywhere and medium-sized companies in lower-income countries.

What happens if a company misses its SBTi target?

Under the old standard, falling behind could cost a company its SBTi status. Under V2’s “best efforts” approach, a company can hold onto its status as long as it’s used every lever within its control, with minimum progress rules coming in the SBTi Assurance Manual.

Sources: This post is based on Terrapass’s internal analysis of the SBTi Corporate Net-Zero Standard V2.0. Facts and figures were checked against SBTi’s official V2.0 announcement, SBTi’s Corporate Net-Zero Standard V2.0 — Chapter 6: Ongoing Emissions Responsibility, Trellis’s coverage of the standard, Trellis’s reporting on Ongoing Emissions Recognition costs, Sylvera’s analysis of what comes next, Anthesis Group’s Fortune 500 net-zero commitments research, and Climate Impact Partners’ seventh annual FG500 analysis, as reported by CarbonUnits.com.

The post SBTi Net-Zero Standard V2: What the Revision Means for Every Business appeared first on Terrapass.

For most businesses, the emissions that matter most sit outside their own walls. Scope 3 emissions, everything generated across your value chain, from the suppliers who make your inputs to the customers who use your products, typically make up the majority of a company’s total carbon footprint. Under the Corporate Sustainability Reporting Directive (CSRD), those value-chain emissions now have to be measured and disclosed with a rigour that spend-based estimates alone struggle to satisfy. This guide sets out how to improve Scope 3 data accuracy for CSRD: the calculation methods open to you, how to move from estimates to verified supplier data, and how to govern that data so it holds up to audit.

![]()

A carbon credit is a commitment that extends well into the future. The tonne of CO₂ compensated for today from a nature-based carbon project must remain out of the atmosphere for good, which means the forest behind the credit has to remain standing long after the transaction is complete. For any buyer, this raises a defining question: What ensures that the forest endures?

![]()

-

Climate Change12 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases12 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Renewable Energy10 months ago

Renewable Energy10 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits

-

Greenhouse Gases1 year ago

嘉宾来稿:探究火山喷发如何影响气候预测