![]()

Who’s Winning the Oil Game? A Financial Face-Off

Shell: Struggling Profits, Big Promises

Shell reported Q4 2024 earnings of $1.20 per ADS (American Depository Share), missing the Zacks Consensus Estimate of $1.78 and significantly lower than $2.22 per ADS in Q4 2023. The company’s revenue dropped to $66.8 billion from $80.1 billion, falling short of expectations by 16.6%. The decline was driven by weaker realized prices, reduced trading margins, and lower LNG sales.

Shell repurchased $3.6 billion in shares and increased its dividend by 5%, with plans for another $3.5 billion in repurchases in Q1 2025. Here is the oil giant’s income per segment:

- Upstream: Profit fell to $1.7 billion from $3.1 billion, missing expectations due to lower oil and gas prices. Liquids prices fell 11%, while natural gas declined 7%.

- Chemicals & Products: Reported a $229 million loss, reversing a $29 million profit from the previous year, due to lower margins and unfavorable tax movements.

- Integrated Gas: Adjusted income dropped to $2.2 billion from $4 billion, missing the expected $2.8 billion due to a 14.3% drop in LNG sales.

- Marketing: Income rose to $839 million from $794 million, but missed expectations of $885 million.

- Renewables & Energy Solutions: Recorded a $311 million loss, down from a $173 million profit a year earlier, due to rising costs and adverse tax effects.

Chevron: A Mixed Bag of Losses and Growth

Chevron’s Q4 earnings fell below Wall Street expectations, reporting adjusted EPS of $2.06 versus the estimated $2.11. This led to a 4% drop in its stock price. The company’s downstream segment posted a $248 million loss, compared to a $1.15 billion profit in Q4 2023. This is because refining margins weakened amid declining fuel demand in the U.S. and China.

- Oil & Gas Production: Profits rose to $4.3 billion from $1.59 billion a year ago, despite a flat overall output of 3.35 million boepd (Barrels of oil equivalent per day). Permian Basin production grew 14% to a record 992,000 boepd.

- Refining: Weak jet fuel demand contributed to the company’s first refining loss since 2020.

Chevron expects global output to grow 6-8% in 2025 and 3-6% in 2026. The company raised its quarterly dividend by 5% and reaffirmed share buyback plans of $10-$20 billion annually.

Exxon: Defying Expectations Amid Industry Headwinds

Exxon announced Q4 2024 earnings of $7.6 billion, or $1.72 per share, exceeding analyst estimates of $1.56. Despite lower oil prices, higher production helped offset the weaker refining margins of this big oil company.

- Oil & Gas Production: Adjusted earnings rose to $6.28 billion from $4.15 billion a year earlier. Production increased to 4.6 million boepd, driven by low production costs in the Permian Basin and Guyana projects.

- Refining: Earnings from gasoline and diesel production dropped sharply to $323 million from $3.2 billion a year earlier due to increased refinery capacity in Asia.

Exxon reported $33.7 billion in earnings for 2024, down from $38.57 billion in 2023, but highlighted strong operational efficiency and profitability.

The three energy giants all faced challenges in Q4 2024, with weaker refining margins and lower oil prices impacting profitability. However, Exxon outperformed expectations, while Chevron and Shell struggled with underwhelming results. All three companies remain focused on capital discipline, shareholder returns, and production efficiency moving forward.

The Green Pivot: Are Big Oil’s Net Zero Pledges Enough?

Shell, Chevron, and ExxonMobil are charting distinct paths toward sustainability as the energy landscape evolves. Their climate commitments, emissions targets, and investment in renewables illustrate their vision for a lower-carbon future.

Each of the energy giants has its own roadmap to net-zero emissions, with varying approaches and strategies. To have a clearer picture of how much carbon pollution each of them emitted in 2023, look at the image below.

![]()

While some are making bolder moves in renewables, others remain focused on carbon capture and efficiency improvements. Understanding Shell, Chevron, and ExxonMobil’s strategies provides insight into the future of the oil and gas industry.

Shell’s Carbon Commitment: Big Talk or Real Action?

Shell aims to become a net-zero emissions energy business by 2050 as part of its Powering Progress strategy. This commitment includes eliminating operational emissions and reducing the emissions from the energy products it sells.

The company has set several targets to achieve this goal:

- 50% absolute emissions reduction by 2030 (Scopes 1 and 2) compared to 2016 levels.

- Eliminate routine flaring of natural gas by 2025 to curb carbon emissions.

- Reduce methane emissions intensity below 0.2% and reach near-zero methane emissions by 2030.

- 15-20% reduction in customer emissions from oil products by 2030 (Scope 3, Category 11, 2021 baseline).

Progress Achieved

By the end of 2023, Shell had cut more than 60% of its emissions goal for 2030. The company’s methane emissions intensity was 0.05% for facilities with marketed gas and 0.001% for facilities without marketed gas.

Shell tracks its emissions reductions through Net Carbon Intensity (NCI), which measures emissions per unit of energy sold. Key milestones include:

- 6-8% reduction achieved in 2023 (from 2016 levels)

- 9-12% reduction target for 2024

- 100% reduction goal by 2050

Shell’s strategy for 2030 balances energy security with sustainability. The company plans to reduce emissions by evolving its product mix and shifting towards low-carbon solutions such as biofuels, hydrogen, and renewables.

Shell has also invested heavily in carbon offset initiatives to negate its GHG emissions. However, under CEO Wael Sawan’s leadership, the oil giant is reducing its focus on nature-based projects and is considering engineered carbon removals instead.

- READ MORE: Shell and Microsoft Are The Biggest Carbon Credit Buyers in 2024: What Projects Do They Support?

Today, 70% of Shell’s cash flow comes from Integrated Gas and Upstream businesses, while 75% of its emissions come from Downstream, Renewables, and Energy Solutions. Additionally, Shell has invested heavily in offshore wind projects, with plans to expand its renewable energy portfolio across multiple continents.

Chevron’s Climate Play: Real Solutions or Greenwashing?

Chevron is investing $8 billion in lower-carbon energy projects from 2021-2028, including renewable fuels, carbon capture, hydrogen, and offsets. An additional $2 billion is allocated to reducing emissions within its operations.

The company is also developing new partnerships with tech firms to enhance energy efficiency and reduce its environmental impact.

Chevron targets net-zero upstream Scope 1 and 2 emissions by 2050 but acknowledges that achieving this goal depends on technological advances, regulatory support, and viable carbon capture and offset mechanisms.

2028 Carbon Intensity Targets

Chevron’s plans to lower carbon intensity include:

- 71 g CO₂e/MJ portfolio carbon intensity (Scope 1, 2, and 3)

- 24 kg CO₂e/boe oil carbon intensity (Scope 1 and 2)

- 24 kg CO₂e/boe gas carbon intensity (Scope 1 and 2)

- 36 kg CO₂e/boe refining carbon intensity (Scope 1 and 2)

GHG Reduction Initiatives

Chevron uses the Marginal Abatement Cost Curve (MACC) to optimize carbon reduction. The company has identified 150+ GHG abatement projects, with over $600 million in investments planned for 2024.

Between 2021-2028, Chevron expects $2 billion in GHG reduction investments, targeting 4 million metric tons (mt) of annual emissions reductions. Here are the company’s other sustainability plans and strategies to achieve its ambitious 2050 net zero goal.

Methane and Renewable Energy Expansion

- Methane emissions goal of 2.0 kg CO₂e/boe by 2028

- Advanced methane detection programs, including satellite monitoring

- Growing renewable fuels capacity to 100 mbd by 2030, including renewable diesel and sustainable aviation fuel

- Significant CCUS investments, including Bayou Bend (Texas) and Gorgon (Australia)

- Expanding hydrogen production to 150 mtpa by 2030

- Developing advanced geothermal energy projects to enhance clean energy production

SEE MORE: Chevron Reports Lower Q2 Earnings! What About Its Emissions?

ExxonMobil’s Bold Bet on Decarbonization

ExxonMobil has cut 23% of nitrogen oxides, sulfur oxides, and volatile organic compounds emissions since 2016. In 2023, its GHG emissions stood at 111 MMTCO₂e, marking a 2 MMT reduction from the previous year. The company is also exploring new ways to enhance energy efficiency across its global operations.

ExxonMobil aims for a 20% absolute reduction in GHG emissions by 2030, compared to 2016 levels. The company aligns its emissions reductions with the Paris Agreement while emphasizing intensity-based reductions.

Beyond burning down emissions in its own operations, Exxon is also helping other industries decarbonize. Its Low Carbon Solutions business focuses on hard-to-decarbonize sectors like heavy industry, power, and transportation. The oil giant seeks to lead in profitable, large-scale emission reduction solutions, with the following key strategies.

Key Sustainability Actions

- Investing in carbon capture, biofuels, and hydrogen

- Advancing methane management with innovative detection technologies

- Deploying CCUS projects, including the world’s largest CCUS facility at LaBarge, Wyoming

- Developing low-carbon solutions for hard-to-abate industries

- Launching a $17 billion investment plan in lower-carbon solutions through 2027

- Exploring direct air capture (DAC) technologies to remove CO₂ from the atmosphere

READ MORE: ExxonMobil’s First-of-its-Kind Carbon Capture Solution for the U.S. Data Centers

Big Oil’s Race Against Time

Shell, Chevron, and ExxonMobil are taking different approaches to sustainability and emissions reduction. While Shell focuses on reducing absolute emissions and net carbon intensity, Chevron prioritizes carbon intensity reduction and methane management. ExxonMobil, meanwhile, is expanding CCUS and methane detection efforts to lower emissions.

As global climate policies tighten, Shell, Chevron, ExxonMobil, and other energy companies should accelerate their transition strategies to meet net-zero targets.

- FURTHER READING: Shell’s Polaris Project Fuels Canada’s Carbon Capture Revolution

The post Big Oil’s Showdown: How Shell, Chevron & ExxonMobil Balance Big Profits with Net Zero? appeared first on Carbon Credits.

The U.S. Department of Energy is intensifying efforts to secure critical minerals as global supply risks rise. In a new collaboration, the DOE’s Ames National Laboratory and the Critical Materials Innovation Hub have joined hands with Amazon to recover high-value materials from waste.

The partnership focuses on extracting battery-grade graphite and key minerals from discarded textiles and electronic waste. This move reflects a broader U.S. strategy—reduce import dependence, build domestic capacity, and create a circular supply chain for critical materials.

Assistant Secretary of Energy (EERE) Audrey Robertson, leading DOE’s Office of Critical Materials and Energy Innovation, said:

“At scale, the recovery of critical minerals from end-of-life technologies and textile waste has the potential to transform our domestic critical materials supply chains. This pioneering work, made possible by an exciting new partnership with Amazon, supports the Trump Administration’s efforts to reduce our reliance on foreign imports and strengthen our national security.”

U.S. Aims for Domestic Graphite Supply

The collaboration combines materials science with artificial intelligence. Ames Lab and CMI bring decades of expertise in metals refining and advanced materials. Amazon contributes AI, logistics, and large-scale supply chain capabilities.

Ames Laboratory Director Karl Mueller also noted,

“This is an excellent match for Ames National Laboratory’s deep expertise in materials science. For decades, Ames Lab has led the nation in metals refining, purification, and critical materials research—and applying that strength to real-world challenges.”

Turning Textiles into Battery-Grade Graphite

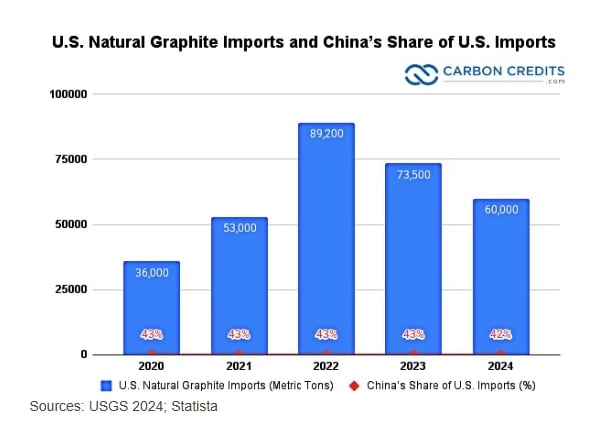

A major project aims to convert discarded textiles into battery-grade graphite. This is significant because graphite is essential for lithium-ion batteries used in electric vehicles (EVs) and energy storage systems.

Today, the U.S. remains heavily dependent on imports for graphite. In fact, more than 90% of global battery-grade graphite processing is concentrated in China, creating a major supply risk.

- As of 2024, the U.S. imported about 60,000 metric tons of natural graphite, down from roughly 84,000 tons in 2023.

- China remained the largest supplier, accounting for around 67.6% of all natural graphite imports by value.

This is worth roughly $375 million. It represents a slight decrease in volume but still a dominant share of the market.

By extracting graphite from waste, the U.S. can reduce both landfill pressure and foreign dependence. This approach aligns with the DOE’s push to secure materials from “secondary sources” such as waste streams.

AWS Powers AI-Driven Mineral Recovery

A second initiative focuses on recovering minerals like gallium from end-of-life IT hardware. Gallium is a critical input for semiconductors, power electronics, and defense technologies.

The importance of this effort is clear. In recent years, China has restricted exports of gallium and germanium, disrupting global supply. These restrictions effectively removed up to 90% of global gallium supply from international markets, exposing major vulnerabilities.

Here, Amazon Web Services will deploy AI tools to map supply chains, identify recovery opportunities, and assess economic feasibility. At the same time, CMI researchers will develop efficient extraction and refining methods.

This fusion of AI and materials science could transform recycling. Instead of being discarded, old electronics could become a reliable domestic source of critical minerals.

A Fragile Supply Chain: Why the U.S. Is Acting Now

Critical minerals are the core of modern industries—from EVs and renewable energy to semiconductors and defense systems. However, U.S. supply chains remain highly vulnerable.

According to recent industry analysis:

- The U.S. is 100% import-reliant for at least 13 critical minerals

- Over 20 additional minerals have an import dependence above 50%

- The country exports much of its raw materials for processing overseas due to limited domestic capacity

China dominates refining and processing, backed by decades of industrial policy. This concentration creates risks of supply disruptions, price spikes, and geopolitical leverage.

To address this, the U.S. government is mobilizing large-scale investments. In 2025, the DOE announced nearly $1 billion in funding to strengthen domestic critical mineral supply chains, with a strong focus on battery materials processing and recycling.

Additionally, new initiatives such as strategic stockpiles and international partnerships are being developed to secure long-term supply.

CMI Hub Leads the Shift to Circular Supply Chains

The Amazon–DOE partnership reflects a major shift in strategy. Traditionally, supply security depended on mining new resources. Now, recycling and “urban mining” are becoming equally important.

The CMI Hub is leading this transition through research in:

- Expanding material supply sources

- Developing substitutes for scarce minerals

- Recovering materials from waste

- Accelerating the commercialization of new technologies

Recycling offers several advantages. It is faster to deploy than mining, less environmentally damaging, and often more cost-effective in the long run. For example, the U.S. has already committed funding to advanced graphite recycling projects to build domestic battery supply chains.

CMI Hub Director Tom Lograsso

“This collaboration is a natural extension of the expertise that CMI Hub was created to deliver. CMI’s mission is to move breakthrough materials technologies from the laboratory into real-world applications on timelines that meet industry’s needs. Working with Amazon gives us the opportunity to apply our capabilities at scale—combining CMI’s materials science expertise with Amazon’s AI to turn innovations into practical solutions that strengthen the nation’s critical materials supply chains.”

Public–Private Partnerships Drive Scale

This collaboration also highlights a broader trend—closer ties between government research institutions and private companies.

Amazon brings AI, data analytics, and global logistics. Ames Lab and CMI contribute scientific expertise and research infrastructure. Together, they aim to move solutions from the lab to real-world deployment at scale.

Such partnerships are critical because the challenge is not just technical. It also involves economics, infrastructure, and supply chain coordination. By combining strengths, these collaborations can accelerate innovation and reduce risks.

Conclusion: A Strategic Shift With Global Impact

The U.S. is clearly redefining its critical minerals strategy. Instead of relying only on mining, it is tapping into waste as a new resource base.

This approach offers strong advantages:

- Waste streams are abundant and underutilized

- Recycling reduces environmental impact

- Domestic recovery improves supply security

However, challenges remain. Domestic processing capacity is still limited, and scaling recycling technologies will require sustained investment and policy support.

At the same time, AI is emerging as a key enabler. It can optimize recovery processes, improve efficiency, and reduce costs. As adoption grows, it could become a critical tool in securing mineral supply chains.

And the partnership between the DOE, Ames Lab, CMI, and Amazon marks a turning point in how the U.S. approaches critical minerals.

- READ MORE: DOE Launches $500M Funding Drive to Strengthen U.S. Battery Supply Chains and Critical Minerals Processing

- LATEST: AI Solutions from Microsoft and NVIDIA Power DOE’s Nuclear Energy Genesis Mission • Carbon Credits

The post DOE and Amazon Partner to Secure Critical Minerals Through AI-Driven Recycling appeared first on Carbon Credits.

Carbon Footprint

Google Expands SAF Strategy with Amex GBT and Shell Aviation to Cut Aviation Emissions

Google is stepping up its climate strategy with a deeper commitment to sustainable aviation fuel (SAF). In a new long-term agreement with American Express Global Business Travel and Shell Aviation, the tech giant will source SAF environmental attribute data through the Avelia registry.

This move highlights a bigger trend. Corporations are no longer just offsetting emissions—they are actively shaping clean fuel markets. For Google, SAF is becoming a critical tool to cut emissions from business travel, one of the hardest sectors to decarbonize.

Vrushali Gaud, Global Director of Climate Operations, Google, said:

“Sustainable aviation fuel represents a critical unlock for decarbonizing the hard-to-abate aviation sector and we recognize the importance of long-term agreements to increase demand and expand its availability. We view this as a key opportunity to support the broader ecosystem through this book and claim effort, while making progress towards reducing our own aviation emissions.”

How “Book and Claim” Is Changing the Future of Aviation Fuel

SAF offers a clear advantage. It can reduce lifecycle greenhouse gas emissions by up to 80% compared to traditional jet fuel. That makes it one of the most promising solutions for aviation, a sector with limited low-carbon alternatives.

Google’s participation in the Avelia platform shows how corporate demand can drive supply. Avelia uses a “book and claim” system, allowing companies to claim emissions reductions even if SAF is not physically used on their specific flight. Instead, SAF is added elsewhere in the fuel network, and the environmental benefits are tracked digitally using blockchain.

This system solves a major problem—limited fuel availability. SAF supply is still concentrated in a few locations, while demand is global. By separating physical fuel use from emissions accounting, Avelia expands access and encourages broader adoption.

The platform has already made measurable progress:

- Over 64 million gallons of SAF have been supplied globally

- More than 590,000 tonnes of CO₂ emissions avoided

- Participation from 66 companies and airlines

These numbers signal growing momentum. More importantly, they show how digital infrastructure can accelerate climate solutions in traditional industries.

Beyond Flights: Google’s Broader Transport Strategy to Achieve Carbon-Neutral by 2030

Google’s SAF investment is only one part of a larger plan to cut transport emissions. The company is actively reducing the carbon footprint of both employee commuting and logistics.

Low-Carbon Commutes with EVs

It promotes low-carbon commuting by offering shuttle services, encouraging carpooling, and supporting public transit, cycling, and walking. At its campuses, Google is also investing heavily in electric mobility. By 2024, it had installed over 6,000 EV charging ports across the U.S. and Canada. In India, electric vehicles already make up nearly a quarter of its internal commuter fleet.

At the same time, Google is investing directly in SAF production. In 2024, it joined the United Airlines Ventures Sustainable Flight Fund, a $200+ million initiative supporting next-generation fuel technologies. The fund backs companies like Viridos and Svante, which are working on advanced fuel and carbon capture solutions.

Google is also a member of the Sustainable Aviation Buyers Alliance, further strengthening its role in shaping demand for cleaner aviation fuels.

The Reality Check: SAF Growth Faces Real Barriers

Despite strong corporate interest, SAF still faces significant challenges. Global production is rising fast, but not fast enough.

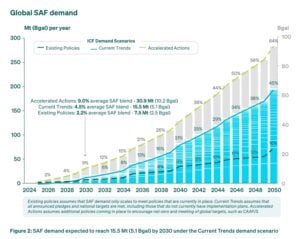

Production increased 24 times since 2021 and is expected to reach around 713 million gallons by the end of 2025. However, this still represents less than 1% of total jet fuel demand.

Even more concerning, growth may slow in 2026. According to the International Air Transport Association (IATA), production is expected to rise only modestly, reaching about 2.4 million metric tons. At the same time, costs remain high—SAF can be two to five times more expensive than conventional fuel.

This price gap creates a major burden for airlines. In 2025 alone, SAF-related costs could reach $3.6 billion globally. Without stronger policy support, scaling production will remain difficult.

Policy and Market Shifts: A Fragmented Landscape

Policy support plays a crucial role in SAF growth, but global approaches remain uneven.

In the U.S., incentives are weakening. The Clean Fuel Production Tax Credit (45Z) will drop significantly in 2026, reducing financial support for SAF producers. This could slow investment and limit supply growth.

In contrast, Europe is pushing ahead. The ReFuelEU Aviation mandate requires a 2% SAF blend, while countries in Asia, including Singapore and Thailand, are introducing their own mandates starting in 2026.

This divergence creates uncertainty. Companies and producers must navigate different regulations across regions, making long-term planning more complex.

The Feedstock Challenge: The Biggest Bottleneck

Analysts say technology is not the main constraint for SAF—feedstock is.

SAF relies on low-carbon raw materials such as waste oils, agricultural residues, and synthetic fuels. These resources are limited and already in demand from other sectors like renewable diesel and bioenergy.

As competition intensifies, sustainability standards are also becoming stricter. Producers must prove that their feedstocks are traceable and truly low-carbon. This means rapid expansion is unlikely in the short term. Instead, companies are expected to focus on gradual capacity growth and flexible production strategies.

Considering all the above factors, 2026 will not deliver a breakthrough but it will test the foundation of the SAF market. Three factors will define progress:

- Policy credibility: Governments must provide stable, long-term incentives

- Feedstock strategy: Companies need reliable and sustainable supply chains

- Procurement innovation: Airlines and corporations must adopt smarter purchasing models

Momentum is building, but it remains selective. Only companies that align these elements will succeed as the market evolves.

Looking Ahead: Strong Demand Signals for 2030 and Beyond

Despite the challenges, SkyNRG’s SAF Market Outlook gives optimistic long-term projections. It highlights that the demand could reach 15.5 million metric tons by 2030 under current trends.

These numbers highlight one key point: demand is not the problem. The challenge lies in scaling supply efficiently and affordably. Nonetheless, sustainable aviation fuel holds real promise. It offers one of the few viable paths to reduce emissions in aviation without redesigning aircraft.

Google’s latest move shows how large corporations can accelerate this transition. But the road ahead remains complex. High costs, limited supply, and policy uncertainty continue to slow progress.

The bottom line is clear: SAF is not scaling overnight. But with the right mix of corporate demand, policy support, and innovation, it could become a cornerstone of clean aviation in the decades ahead.

- ALSO READ: Greening the Aviation: Lufthansa and Airbus Team Up to Cut Business Travel Emissions Using SAF

The post Google Expands SAF Strategy with Amex GBT and Shell Aviation to Cut Aviation Emissions appeared first on Carbon Credits.

Carbon Footprint

History Repeating Itself: Why Middle East Conflict at the Pump Should Be a Wake-Up Call for North America

Disseminated on behalf of Surge Battery Metals.

Every time instability erupts in the Middle East, North Americans feel it where it hurts most—at the gas pump. It happened in 1979, when the Iranian Revolution sent shockwaves through global energy markets. Oil supplies tightened. Prices surged, and inflation followed. Entire economies slowed under the pressure.

For millions of households, the crisis’s impact was personal. It showed up in longer lines at gas stations and rising costs across daily life.

Nearly five decades later, the pattern is repeating.

Renewed tensions across key oil-producing regions are once again tightening global supply. Prices are rising. Consumers are feeling the impact. And once again, events unfolding thousands of miles away are shaping the cost of energy at home.

This pattern suggests a persistent structural vulnerability in North America’s exposure to global oil‑supply shocks. The region still depends heavily on global oil markets. That means supply disruptions, no matter where they occur, can quickly ripple through the system.

The result is a familiar cycle: geopolitical instability leads to supply concerns, which drive up prices, which then feed directly into the cost of living.

A Cycle Consumers Know All Too Well

When prices spike, households adjust. Commuters rethink travel. Businesses absorb higher costs or pass them on. Inflation pressures build. The impact spreads far beyond the energy sector.

With average gasoline prices currently around $4 per gallon in the US ($5.50 in California), or roughly $1.05 US per liter ($1.45 in California), the connection between global events and local fuel prices is no longer theoretical – it is a lived experience. This is why energy security is increasingly framed as both a policy concern and a kitchen‑table issue.

The events of 1979 were a warning. Today’s rising prices are another. The difference is that North America now has more options than it did back then.

Electric vehicles, battery storage, and renewable power systems are no longer future concepts. They are already part of the energy mix. And for those who have made the shift, the experience is very different, and the transition is already complete.

Instead of watching fuel prices climb, they are plugging in.

Graham Harris, Chairman of Surge Battery Metals, has spoken openly about this shift in practical terms. While rising oil prices create uncertainty at the pump, he charges his electric vehicle at home.

The contrast between gasoline dependency and electrification is becoming more visible.

When oil prices rise, gasoline costs follow. But electricity prices tend to be more stable, especially when supported by domestic generation and renewable sources. That difference is simple but powerful. It changes how people experience energy volatility.

One system is exposed to global shocks. The other is increasingly tied to domestic infrastructure. This contrast highlights how the energy transition is reshaping exposure to global price shocks.

Some analysts increasingly frame the energy transition not only as a climate imperative but also as a strategy to reduce exposure to external risk. It relates to questions of control over where energy comes from, how it is produced, and how stable it is over time.

And at the center of that transition is one critical material: lithium.

Lithium: The Foundation of Energy Independence

Lithium is the core component of modern battery technology. It powers electric vehicles, supports grid-scale energy storage, and plays a growing role in advanced defense systems.

As electrification expands, demand for lithium is rising across multiple sectors.

But here is the challenge: much of today’s lithium supply still comes from outside the United States. This creates a familiar dynamic.

Just as oil dependency has long exposed North America to geopolitical risk, reliance on foreign lithium supply introduces a new layer of vulnerability. The commodity is different, but the structure is similar.

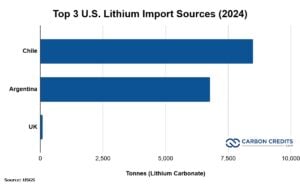

The United States imported the majority of its lithium from Chile and Argentina in 2024. Together, they accounted for roughly 98% of the total supply. Smaller volumes were sourced from the UK, France, and China.

That is why domestic production is becoming a central focus of energy and industrial policy.

In March 2025, Donald Trump signed an executive order titled “Immediate Measures to Increase American Mineral Production.” The directive called for faster permitting, expanded development, and reduced reliance on foreign supply chains for critical minerals.

The message of the order was clear: building domestic capacity is now a strategic priority.

- RELATED: Live Lithium Prices Today

A Domestic Resource Takes Shape in Nevada

Within this broader shift, projects like Surge Battery Metals’ (TSX-V: NILI | OTCQX: NILIF) Nevada North Lithium Project (NNLP) are gaining attention.

NNLP hosts a measured and indicated resource of 11.24 million tonnes of lithium carbonate equivalent (LCE) at an average grade of 3,010 ppm lithium, based on company disclosures. This makes it the highest-grade lithium clay resource identified in the United States to date.

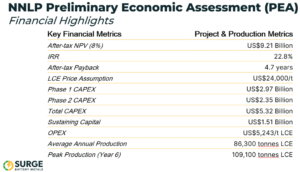

A 2025 Preliminary Economic Assessment (PEA) outlines the project’s scale:

- After-tax NPV (8%): US$9.21 billion

- Internal Rate of Return (IRR): 22.8%

- Mine life: 42 years

- Average annual production: ~86,300 tonnes LCE

- Employment: ~2,000 construction jobs and ~350 long-term operational roles

These figures indicate potential in terms of scale, longevity, and the ability to contribute to domestic supply if the project moves forward. At full production, NNLP has the potential to rank among the larger lithium-producing assets globally, based on third-party analysis.

Recent drilling results announced by Surge Battery Metals have further strengthened NNLP’s profile as a standout asset. In February 2026, step-out drilling found a 31-meter intercept with 4,196 ppm lithium from surface. This is much higher than the project’s average of 3,010 ppm Li. It also extends high-grade mineralization nearly 640 meters beyond the current resource boundary.

Infill drilling showed a steady, thick, high-grade core. It included intercepts like 116 meters at 3,752 ppm Li and 32 meters at 4,521 ppm Li. These results support future resource expansion. They also highlight the project’s scale, quality, and technical readiness as it prepares for a Pre-Feasibility Study.

Beyond the project itself, it reflects a broader policy and industry shift toward building more domestically anchored energy systems.

From Oil Dependency to Mineral Security

The connection between oil and lithium is not always obvious at first glance. Oil fuels internal combustion engines, while lithium supports batteries and energy‑storage systems, with distinct technologies and supply chains.

But the underlying issue is the same. Dependence on external sources creates exposure to external risk.

In the case of oil, that risk has played out repeatedly over decades. Supply disruptions, price shocks, and geopolitical tensions have all shaped the market.

With lithium, the industry is earlier in its development. But the stakes are rising quickly.

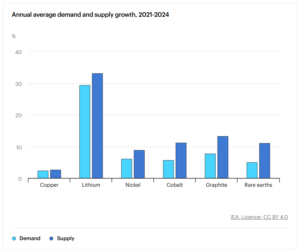

Global demand for lithium grew about 30 % in 2024, driven mainly by batteries for electric vehicles and energy storage, according to IEA data. Demand in 2025 continued at high rates, and under current policies, lithium demand is projected to grow fivefold by 2040 compared with today.

At the same time, supply growth is struggling to keep pace with demand forecasts. These trends show that ensuring a stable, secure supply is becoming just as important as expanding production.

That is where domestic projects come in, such as Surge Battery Metals’ NNLP.

They may not eliminate global market dynamics, but they can reduce exposure to them. They can provide a buffer against volatility. And they can support a more stable, self-reliant energy system.

A Turning Point – or Another Warning?

While history does not repeat in the same way, similar patterns can be observed.

The oil shocks of the 1970s revealed a vulnerability that shaped energy policy for decades. Today’s market signals are pointing to a similar challenge—this time at the intersection of oil dependency and critical mineral supply.

The difference is that the range of policy and technological options available today is broader. Electrification is already underway. Battery technology is advancing. Domestic resource development is gaining policy support. The pieces are in place.

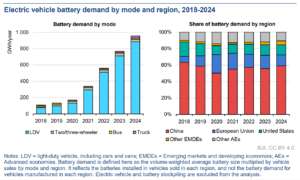

Data from the International Energy Agency’s Global EV Outlook 2025 shows that global battery demand reached a historic milestone of 1 terawatt-hour (TWh) in 2024. This surge was mainly due to the growth of electric vehicles (EVs).

By 2030, demand is expected to more than triple, exceeding 3 TWh under current policies. This reflects not only rising EV adoption but also expanding stationary storage demand. Both of which rely on critical minerals like lithium.

Electric vehicles continue to displace traditional oil use as well. The same IEA analysis shows that by 2030, EVs will replace over 5 million barrels of oil daily. This is about the size of a major country’s transport sector, highlighting how electrification is changing energy markets.

What remains uncertain is the pace at which these changes will occur.

Will rising fuel prices once again fade as markets stabilize? Or will they serve as a catalyst for deeper structural shifts?

That question matters not just for policymakers or investors, but for everyday consumers.

Because at the end of the day, energy transitions are not measured in policy papers. They are measured in daily decisions—how people power their homes, fuel their vehicles, and respond to rising costs.

DISCLAIMER

New Era Publishing Inc. and/or CarbonCredits.com (“We” or “Us”) are not securities dealers or brokers, investment advisers, or financial advisers, and you should not rely on the information herein as investment advice. Surge Battery Metals Inc. (“Company”) made a one-time payment of $75,000 to provide marketing services for a term of three months. None of the owners, members, directors, or employees of New Era Publishing Inc. and/or CarbonCredits.com currently hold, or have any beneficial ownership in, any shares, stocks, or options of the companies mentioned.

This article is informational only and is solely for use by prospective investors in determining whether to seek additional information. It does not constitute an offer to sell or a solicitation of an offer to buy any securities. Examples that we provide of share price increases pertaining to a particular issuer from one referenced date to another represent arbitrarily chosen time periods and are no indication whatsoever of future stock prices for that issuer and are of no predictive value.

Our stock profiles are intended to highlight certain companies for your further investigation; they are not stock recommendations or an offer or sale of the referenced securities. The securities issued by the companies we profile should be considered high-risk; if you do invest despite these warnings, you may lose your entire investment. Please do your own research before investing, including reviewing the companies’ SEDAR+ and SEC filings, press releases, and risk disclosures.

It is our policy that information contained in this profile was provided by the company, extracted from SEDAR+ and SEC filings, company websites, and other publicly available sources. We believe the sources and information are accurate and reliable but we cannot guarantee them.

CAUTIONARY STATEMENT AND FORWARD-LOOKING INFORMATION

Certain statements contained in this news release may constitute “forward-looking information” within the meaning of applicable securities laws. Forward-looking information generally can be identified by words such as “anticipate,” “expect,” “estimate,” “forecast,” “plan,” and similar expressions suggesting future outcomes or events. Forward-looking information is based on current expectations of management; however, it is subject to known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those anticipated.

These factors include, without limitation, statements relating to the Company’s exploration and development plans, the potential of its mineral projects, financing activities, regulatory approvals, market conditions, and future objectives. Forward-looking information involves numerous risks and uncertainties and actual results might differ materially from results suggested in any forward-looking information. These risks and uncertainties include, among other things, market volatility, the state of financial markets for the Company’s securities, fluctuations in commodity prices, operational challenges, and changes in business plans.

Forward-looking information is based on several key expectations and assumptions, including, without limitation, that the Company will continue with its stated business objectives and will be able to raise additional capital as required. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated, or intended.

There can be no assurance that such forward-looking information will prove to be accurate, as actual results and future events could differ materially. Accordingly, readers should not place undue reliance on forward-looking information. Additional information about risks and uncertainties is contained in the Company’s management’s discussion and analysis and annual information form for the year ended December 31, 2025, copies of which are available on SEDAR+ at www.sedarplus.ca.

The forward-looking information contained herein is expressly qualified in its entirety by this cautionary statement. Forward-looking information reflects management’s current beliefs and is based on information currently available to the Company. The forward-looking information is made as of the date of this news release, and the Company assumes no obligation to update or revise such information to reflect new events or circumstances except as may be required by applicable law.

The post History Repeating Itself: Why Middle East Conflict at the Pump Should Be a Wake-Up Call for North America appeared first on Carbon Credits.

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Renewable Energy5 months ago

Renewable Energy5 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits