A surge in gas prices triggered by the Iran war has caused a knock-on spike in the price of electricity in the UK, Italy and many other European markets.

This is because gas almost always sets the price of power in these countries, even though a significant share of their electricity comes from cheaper sources.

This “coupling”, which is part of what UK energy secretary Ed Miliband calls the “fossil-fuel rollercoaster”, is due to the “marginal pricing” system used in most electricity markets globally.

After another fossil-fuel price shock, just four years after Russia’s invasion of Ukraine, this coupling between gas and electricity prices is once again under the spotlight, in the UK and the EU.

There are various alternatives that have been put forward as ways to break – or “decouple” – the link between gas and electricity prices.

Electricity prices could be “decoupled” from gas prices by changing the way the market works, but ideas for doing this either have not been tested or have problems of their own.

Some people have implied that the UK could insulate itself from high and volatile international gas prices by extracting more gas from the North Sea.

However, contrary to false claims by, for example, the hard-right climate-sceptic Reform UK party, this would not be expected to cut energy bills, because gas prices are set on international markets.

Finally, electricity prices can be “decoupled” from gas by burning less of it, a shift that is nearly complete in Spain and that is already having an impact in the UK.

- Why does gas set the price of electricity?

- What is the impact of gas setting the electricity price?

- What market reforms have been proposed?

- Why is ‘marginal pricing’ in the news again?

- Would it help if more gas were extracted domestically?

- Would burning less gas stop it setting electricity prices?

Why does gas set the price of electricity?

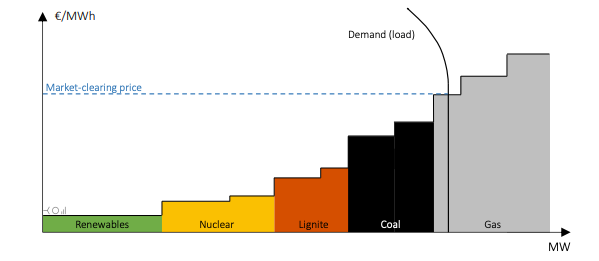

In liberalised economies, electricity is bought and sold via market trading. The market uses a system called “marginal pricing” to match buyers with enough supply to meet their demand.

(The same system is used in most commodity markets, including for oil, gas or food products.)

All of the power plants that are available to generate make “bids” to sell electricity at a particular price. The bids are arranged in a “merit order stack”, from the cheapest to the most expensive, shown in the illustrative schematic below.

This means that the price of gas sets the price of electricity, whenever gas plants are at the margin.

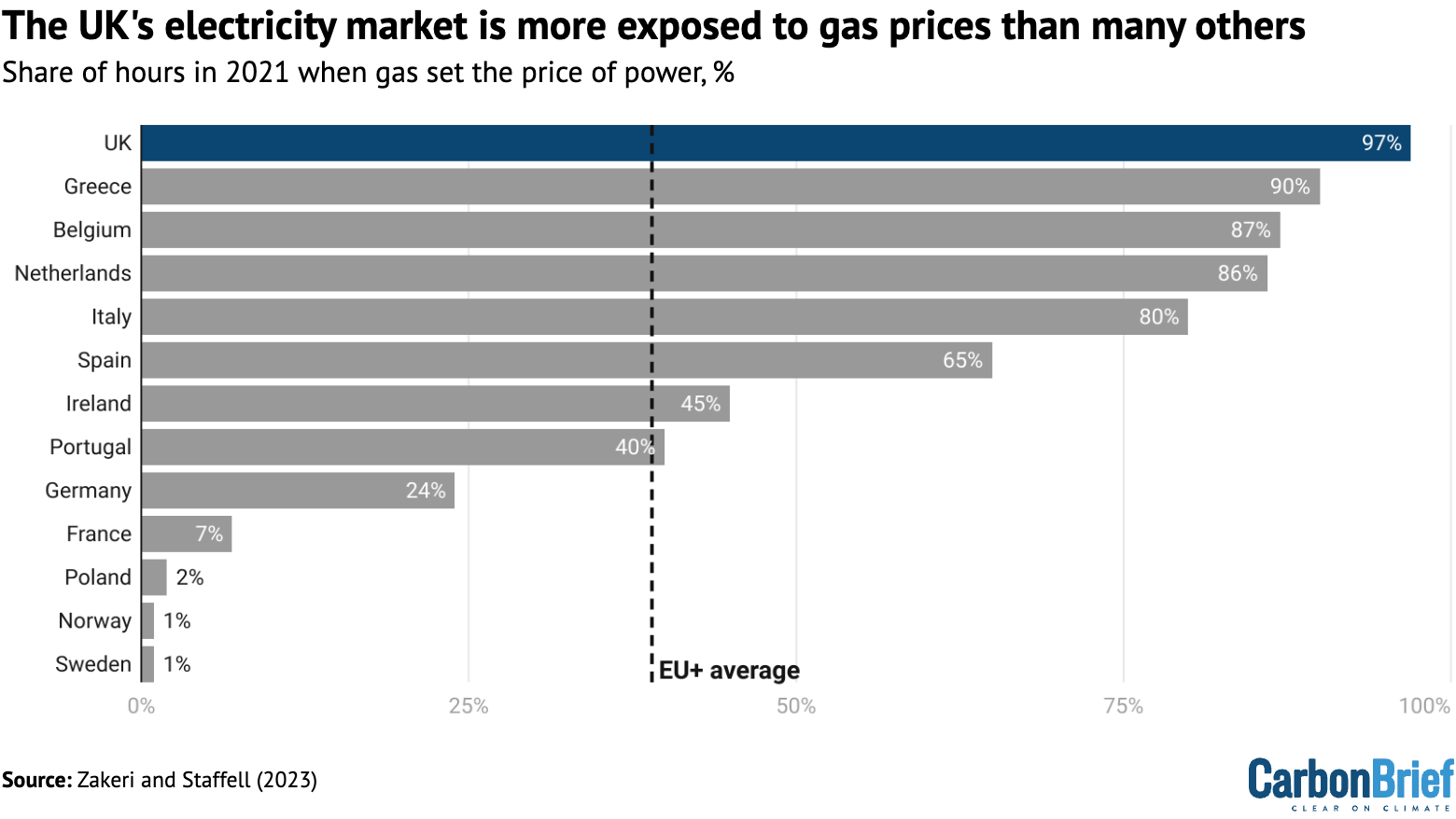

In the UK, the marginal unit is almost always a gas-fired power plant. As a result, one widely cited academic analysis found that gas set the price of power 97% of the time in the UK in 2021.

In contrast, the analysis found that gas only sets the price of power 7% of the time in France, as shown in the figure below. This is because the French market is dominated by nuclear power.

The “pay as clear” marginal-pricing system means that gas sets the price of power more often than might be expected, given its share of electricity generation overall.

For example, gas set the price of power 97% of the time in 2021, even though it only accounted for 37% of electricity generation that year. Equally, even though renewables now make up around half of UK electricity supplies, gas still usually sets the price of power in the UK.

(There are some important subtleties to this, due to the fact that not all gas-fired power plants are equally expensive to run. This is discussed further below.)

Overall, the fact that gas hardly ever sets the price of power in some European markets hints at the potential to decouple electricity prices from gas, by shifting towards alternative sources.

What is the impact of gas setting the electricity price?

The tight coupling of gas and electricity prices in the UK and other markets is the source of significant political debate, particularly during periods when the price of gas soars.

When gas prices hit record highs after Russia’s invasion of Ukraine in 2022, politicians, commentators and the media rushed to understand why this also spiked electricity bills.

The same dynamic is playing out in 2026, following the attacks on Iran by the US and Israel, the closure of the Strait of Hormuz and the resulting surge in international gas prices.

An editorial in the Financial Times published earlier this month is headlined: “The déjà vu of Europe’s energy shock.” It says the crisis is once again raising questions over electricity pricing:

“In Britain, in particular, questions remain on how to reform its electricity pricing, which currently leaves it highly exposed to volatile wholesale gas prices.”

This exposure is illustrated in the figure below, which shows the tight link between prices on the “day-ahead” markets for gas and electricity.

Indeed, recent analysis from the UK Energy Research Centre (UKERC), published before the Iran war, found that high gas prices were still the biggest driver of high UK electricity bills.

The UK is not the only market being hit by high electricity prices after the outbreak of war in the Middle East. Italy is also suffering, at a time when it was already in the midst of a major debate over how to cut electricity prices, which are also high due to its heavy reliance on gas power.

What market reforms have been proposed?

Historically, some governments set the price of electricity themselves. However, this is increasingly rare and most countries now have “liberalised” electricity markets to determine prices.

These markets use the “pay as clear” system of marginal pricing, described above, to balance supply and demand in each hour of the day.

Alternative models include “pay as bid”, where each power plant is only paid the amount that it bid to supply electricity, rather than the higher price of the marginal unit.

However, this “would not provide cheaper prices”, according to the European Commission, because bidders would seek to maximise their profits by guessing the clearing price:

“In the pay-as-bid model, producers (including cheap renewables) would simply bid at the price they expect the market to clear, not at zero or at their generation costs.”

Another option would be to create two separate markets, one “green power pool” for renewables and another for conventional sources of electricity.

One proponent of this idea is Prof Michael Grubb at University College London. In a March 2026 post on LinkedIn he says:

“The impact of surging gas prices on electricity will again highlight the oddities of our current electricity market – which make sense to many economists, but to hardly anyone else.”

Explaining his rationale for creating separate power markets, he continues:

“The crisis again emphasises that gas-generated power and renewables are not really the same commodity and deserve distinct and tailored market structures to also enhance transparency. Unless and until that occurs, no amount of policy tinkering can overcome the volatility imposed by geopolitical events outside our control.”

However, the UK government concluded in 2024 that it “[did] not consider [a green power pool] to be deliverable”, adding that, even if it were possible, it “would not provide additional benefits”.

This was part of the UK government “review of electricity market arrangements” (REMA), which considered – and then rejected – a series of alternative ways to structure the market.

Similarly, it is less than two years since the European Commission also considered – and then rejected – alternatives to the marginal pricing system, notes Jon Ferris, head of flexibility and storage at consultancy LCP Delta, in a LinkedIn post. The commission explains:

“This model provides efficiency, transparency and incentives to keep costs as low as possible. There is general consensus that the marginal model is the most efficient for liberalised electricity markets.”

In the UK, a debate in parliament in early March 2026 saw Labour MP Toby Perkins questioning the marginal pricing system, which he said was now “far less robust”. He said:

“Because renewables are cheaper, should we not look to benefit from that, rather than having a system that allows gas to set the price, even if it accounts for only 1% of our energy?”

Ultimately, however, marginal pricing is the “worst approach to clearing markets apart from all the others”, Ferris tells Carbon Brief.

The Iran crisis has also been used to resurface a more radical option, put forward last year by consultancy Stonehaven and NGO Greenpeace, of taking gas out of the market completely.

The idea would effectively see gas plants being taken into a strategic reserve, where they would receive a regulated return for remaining open. They would be managed centrally and called on to generate power as needed outside of the market, which would continue to use marginal pricing.

Adam Bell, partner at Stonehaven and the government’s former head of energy policy, tells Carbon Brief that it would be possible to implement within 18 months, but only if moving at a pace that the civil service might describe as “brave”.

Why is ‘marginal pricing’ in the news again?

Despite the decisions at UK and EU level to reject the alternatives, interest in moving away from marginal pricing has recently been reignited – even before the shock of the Iran war.

For example, in a speech in February, European Commission president Ursula von der Leyen said a recent meeting of member states had seen “intense discussion” over marginal pricing:

“We did not come to a conclusion. I want to be very clear on this one. But to the next European Council, I will bring different options and findings on whether it is time to move forward on the market design or whether we are still good on this market design.”

A subsequent leak from the commission, seen by Carbon Brief, also implies that marginal pricing is up for debate, as part of ongoing discussions on how to tackle high energy prices.

Subsequently, Philippe Lamberts, climate advisor to von der Leyen, made comments implying that the marginal pricing system was problematic.

In response, ahead of a meeting of EU governments in the week beginning 16 March, a group of seven member states wrote to the commission warning against market reform.

Their letter says that “no satisfactory alternative model has been identified” and that “all other options discussed would introduce inefficiencies”, compared with sticking to marginal pricing.

Industry group Eurelectric makes similar comments in its own letter, as well as warning about the uncertainty that would be created by market reform. It says:

“Delivering massive investments in clean power generation is the structural answer to reduce our dependence on fossil fuels. Reopening the fundamental principles of market design risks increasing uncertainty, delaying investment decisions and, ultimately, raising system costs.”

Another element to the debate has come from Italian government proposals to subsidise gas plants, in an effort to reduce electricity prices in the country.

The proposal has drawn comparisons with the so-called “Iberian mechanism”, under which the governments of Spain and Portugal subsidised gas power during the 2022 energy crisis.

This support did yield “short-term price relief”, says Chris Rosslowe, senior analyst at thinktank Ember in a post on LinkedIn. However, he says it also had “perverse consequences”, including increasing demand for gas “in the middle of a gas supply crisis”.

These sorts of ideas “would cause a lot of collateral damage” in terms of market efficiency, investor confidence and other areas, says Prof Lion Hirth at the Hertie School in Berlin, in a LinkedIn post.

Jean-Paul Harreman, director at consultancy Montel Analytics, writes in an article on LinkedIn:

“[R]eplacing transparent marginal pricing with political price formation is often like replacing a thermometer because you dislike the temperature reading. It may feel satisfying. It does not change the weather.”

Would it help if more gas were extracted domestically?

In the UK, there has also been intense pressure from opposition politicians and some sections of the media to expand gas production in the North Sea.

Nigel Farage, the climate-sceptic head of Reform UK, was recently quoted by Bloomberg as claiming: “Producing our own gas would reduce everybody’s electricity bills significantly.”

There is no evidence to support this claim.

While the opposition Conservatives have also been loudly calling for an expansion of North Sea drilling, they have been more circumspect about any impact on bills.

Writing in the Daily Telegraph, Conservative leader Kemi Badenoch only indirectly links such an expansion in domestic gas production with lower bills. She writes:

“[P]art of the reason we’re being hit so hard by [the Iran war] is because we are not drilling our own oil and gas thanks to [the government’s] net-zero madness.”

Badenoch’s own shadow energy secretary Claire Coutinho contradicted this idea in 2023, when she was in government. She said at the time that awarding new oil and gas licensing “wouldn’t necessarily bring energy bills down”.

This is because, as the UK’s energy minister Michael Shanks said at a recent event: “We will always be a price taker in international fossil-fuel markets, not a price maker.”

What he is saying is that UK gas production is small relative to the size of the European and global market for the fuel. As such, any increases in UK production would not materially affect prices.

Moreover, North Sea gas production has been in decline for decades and this is set to continue, whether or not the government allows new drilling to take place. This is because much of the gas it once contained has already been extracted and burned.

Would burning less gas stop it setting electricity prices?

The final idea for breaking the link between gas and electricity prices is simply to burn less gas.

This is one of the key motivations behind the UK government’s “clean power 2030” plan, which aims to largely decarbonise electricity supplies by 2030.

The government said when launching its plan:

“These investments will protect electricity consumers from volatile gas prices and be the foundation of a UK energy system that can bring down consumer bills for good.”

In 2026, however, UK electricity prices are still largely dictated by gas prices, as described above.

Yet this does not mean that the expansion of renewables has had no impact. Indeed, analysis by thinktank the Energy and Climate Intelligence Unit (ECIU) suggests that renewables have already reduced UK wholesale electricity prices by a third in 2025.

As more renewable generation is added to the system, the most expensive gas plants in the merit order “stack” are knocked out of the market. Even though another gas plant may still be setting power prices, it will be a cheaper and more efficient unit.

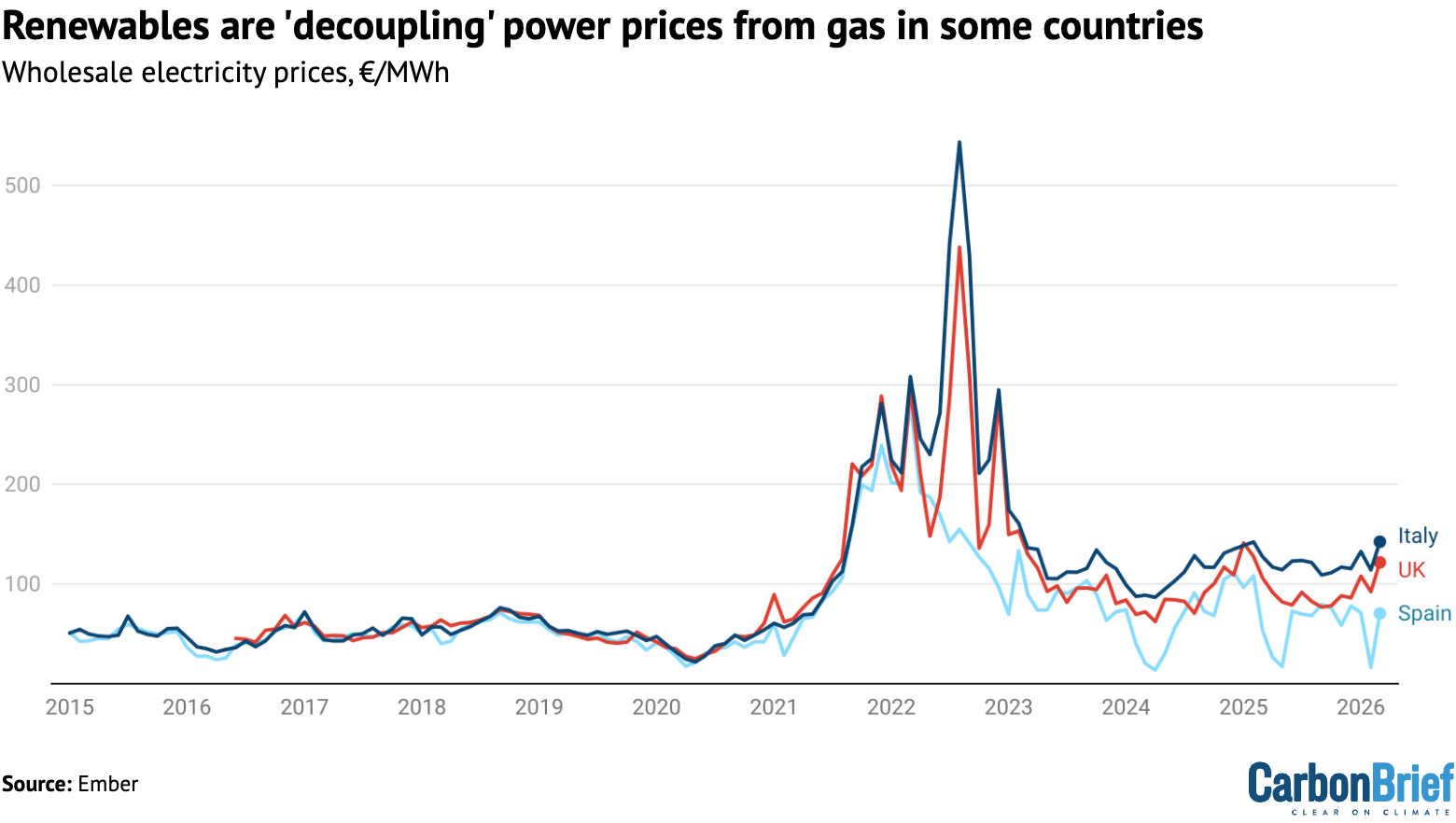

This intermediate impact of renewables is already visible when comparing electricity prices in the UK with those in Italy and Spain, as shown in the figure below.

The figure shows that UK wholesale electricity prices have been lower than those in Italy, as a result of the expansion of renewable sources over the past decade. (Prior to this, wholesale prices were similar in both countries.)

The contrast with prices in Spain is even larger , where Ember says “strong solar and wind growth [has] reduced the influence of expensive coal and gas power on the electricity market”.

The UK is already seeing electricity prices that are “decoupled” from gas prices on windy days. In addition, an increasing amount of electricity is set to be generated by renewable sources that hold “contracts for difference” (CfDs).

CfD projects are paid a fixed price for the electricity they generate, regardless of the price on the “day-ahead” wholesale market. As such, they dilute the impact of gas on consumer bills.

In 2022, when the last energy crisis hit, only 7% of UK generation was covered by CfDs, according to freelance “energy geek” Ben Watts. As of 2026, he says this has climbed to 13%.

By 2030, CfD projects will make up as much as half of total electricity supplies in the UK.

Callum McIver, research fellow at the University of Strathclyde and a member of the UKERC, tells Carbon Brief that CfDs are a “mechanism to decouple bills from the cost of gas”. He adds:

“With significant volumes of new and lower cost renewables on CfDs expected to connect to the system over the next few years, the impact of the scheme on price decoupling should accelerate…This provides an ever increasing hedge against future price shocks.”

Power-purchase agreements (PPAs) can have a similar effect. Here, large users such as industrial sites sign a contract with a power plant to buy the electricity they generate at a fixed price. Again, this takes some electricity out of the wholesale market, diluting the impact of gas prices.

Increases in UK renewable generation are yet to unseat gas from its role in determining electricity prices in most hours of the year, but this shift is starting to have an impact.

Analysis by consultancy Modo Energy suggests that electricity prices in the UK were above the price of gas power in nearly 90% of hours in 2018, a figure that had fallen to below 80% in 2024. Modo’s director Ed Porter said on Twitter: “The link between gas and power prices is weakening.”

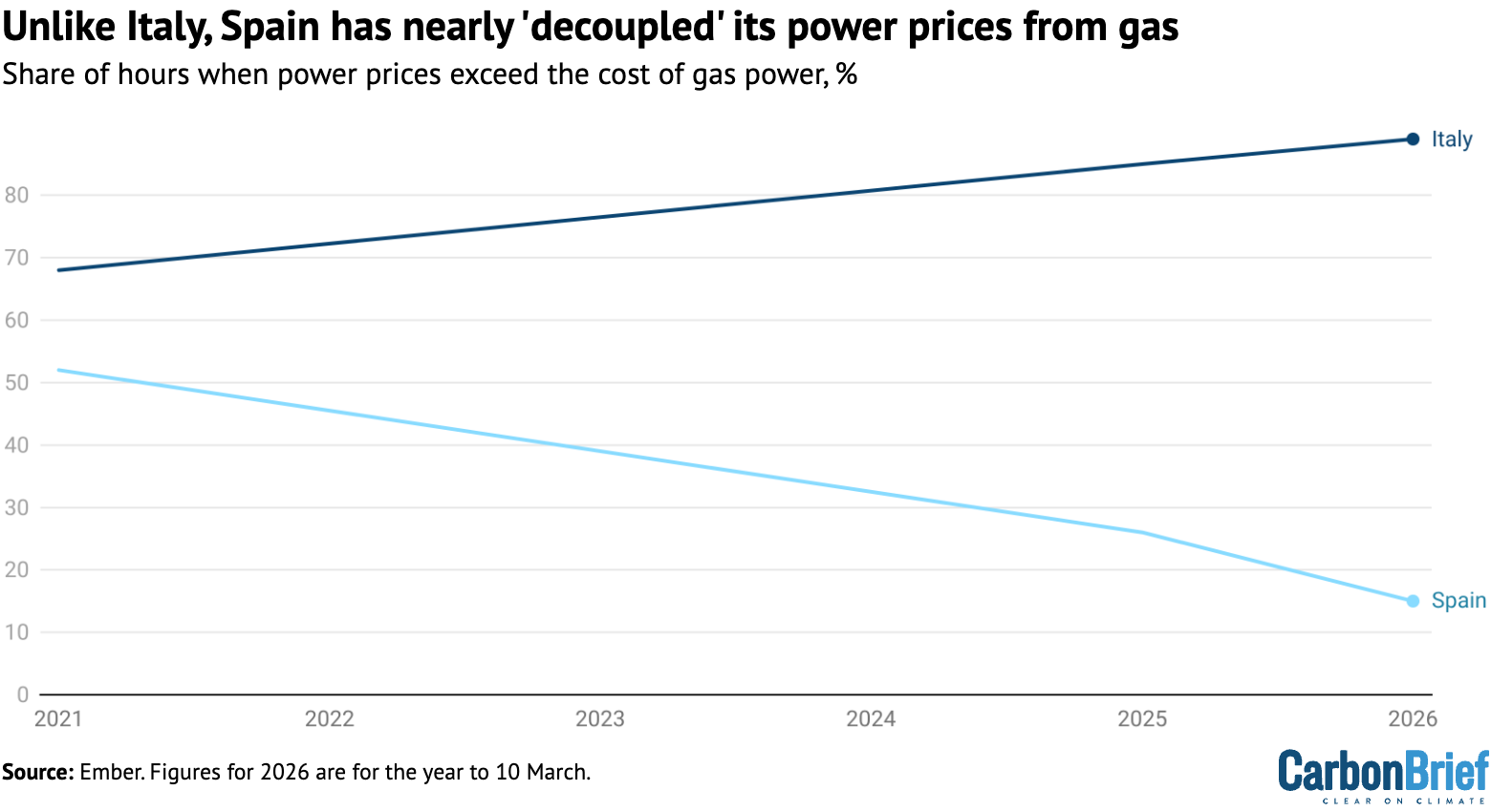

In Spain, analysis by Ember shows that the link is well on the way to being completely broken. Ember data shared with Carbon Brief shows that power prices were above the cost of gas power in 52% of hours in 2021, but this had fallen to 15% of hours in 2026 to date.

This data, shown in the figure below, is in stark contrast with Italy, where the influence of gas on electricity prices has actually increased in recent years.

A similar effect would be possible for the UK. Recent analysis from LCP Delta shows that the UK electricity system would be “almost entirely insulated from gas price shocks”, if it reaches the government’s clean-power 2030 targets.

Posting on LinkedIn, Sam Hollister, principal and head of UK market strategy, writes that a spike in gas prices similar to current levels would only increase household bills by 8%, if the 2030 targets are met. In contrast, bills would rise by 45%, if no CfD-backed renewables were on the system.

In his LinkedIn article, Montel’s Harreman concludes:

“The real structural solution to high power prices is not to mute marginal pricing, but to reduce exposure to fossil fuels and accelerate clean capacity, grids and flexibility. That lowers marginal costs structurally rather than cosmetically.”

“Marginal pricing is uncomfortable in volatile times. But discomfort is not evidence of failure. It is often evidence that the system is telling the truth. And, in energy markets, obscuring the truth is usually more expensive than confronting it.”

The post Q&A: Why does gas set the price of electricity – and is there an alternative? appeared first on Carbon Brief.

Q&A: Why does gas set the price of electricity – and is there an alternative?

Climate Change

DeBriefed 2 April 2026: Countries ‘revive’ energy-crisis measures | Record UK renewables | Plug-in solar savings

Welcome to Carbon Brief’s DeBriefed.

An essential guide to the week’s key developments relating to climate change.

This week

Crisis responses

OIL SUPPLIES: The International Energy Agency (IEA) warned that oil supply disruptions will worsen in April due to the Iran war, reported CNBC. The outlet added that the IEA was considering another release of strategic oil reserves. Meanwhile, US exports of liquefied natural gas (LNG) reached an “all-time high” in March, with shipments to Asia more than doubling from the previous month, said Reuters.

‘SLOWER GROWTH’: The International Monetary Foundation (IMF) warned that “all roads lead to higher prices and slower growth worldwide” if the war continues to choke oil, gas and fertiliser supplies, reported the Guardian. The IMF said the UK and Italy were “especially exposed by their reliance on gas-fired power”, the newspaper added.

EU PREPARES: The EU is considering “reviving energy-crisis measures” it used at the start of the Ukraine war, including “grid tariffs and taxes on electricity”, according to Reuters. France is considering new actions to electrify its economy and cut dependence on fossil imports, said Le Monde. Elsewhere, BBC News rounded up crisis responses from around the world – including fuel rationing, fuel tax cuts, home working and free public transport.

COAL ‘SHORT-LIVED’: Some countries announced plans to delay coal-plant shutdowns. Italy plans to push back its coal-power phaseout to 2038, according to Reuters. Germany will review whether to reactivate reserve plants, reported Bloomberg. South Korea also extended three plants set to close this year, said the Korea Times. However, a separate Bloomberg comment piece stated that “any shift to burn more coal in 2026 will be short-lived”

Around the world

- GAS SCRAPPED?: New Zealand’s government cast doubt over plans to build an LNG import terminal as rising gas prices have worsened the economics, said the New Zealand Herald. Separately, plans for Vietnam’s largest LNG power plant may be scrapped in favour of a new renewable energy project, according to Reuters.

- PHASEOUT SUMMIT: Climate Home News reported that 46 countries – including major oil producers – have confirmed they will attend the fossil-fuel phaseout summit being held in Colombia later this month.

- INDIAN SUMMER: India is “forecast to experience higher than normal heatwave days through June, raising the risk of power shortages” as the Middle East conflict worsens energy strains, reported Bloomberg.

- AFGHANISTAN FLOODS: Heavy rainfall and floods across Afghanistan have killed at least 48 people and damaged communities, following years of drought, said Kabul Now.

- WIND BUYOUTS: In an effort to halt remaining US offshore wind projects, the Trump administration is offering buyouts to developers in exchange for fossil-fuel investments, according to the Financial Times.

66%

The annual increase in forest loss in Indonesia in 2025, according to Indonesian biodiversity thinktank Auriga Nusantara, reported by Reuters.

Latest climate research

- New research explores “patterns of distributional justice” in the mitigation scenarios used in the IPCC’s sixth assessment | npj Climate Action

- Antarctic surface melt will expand by more than 10% by 2100, if future greenhouse gas emissions continue to be high | Nature Communications

- The evolution of the urban heat island effect in Chinese cities is “not unidirectional, but depends on localised urbanisation and greening dynamics” | PNAS Nexus

(For more, see Carbon Brief’s in-depth daily summaries of the top climate news stories on Monday, Tuesday, Wednesday and Thursday.)

Captured

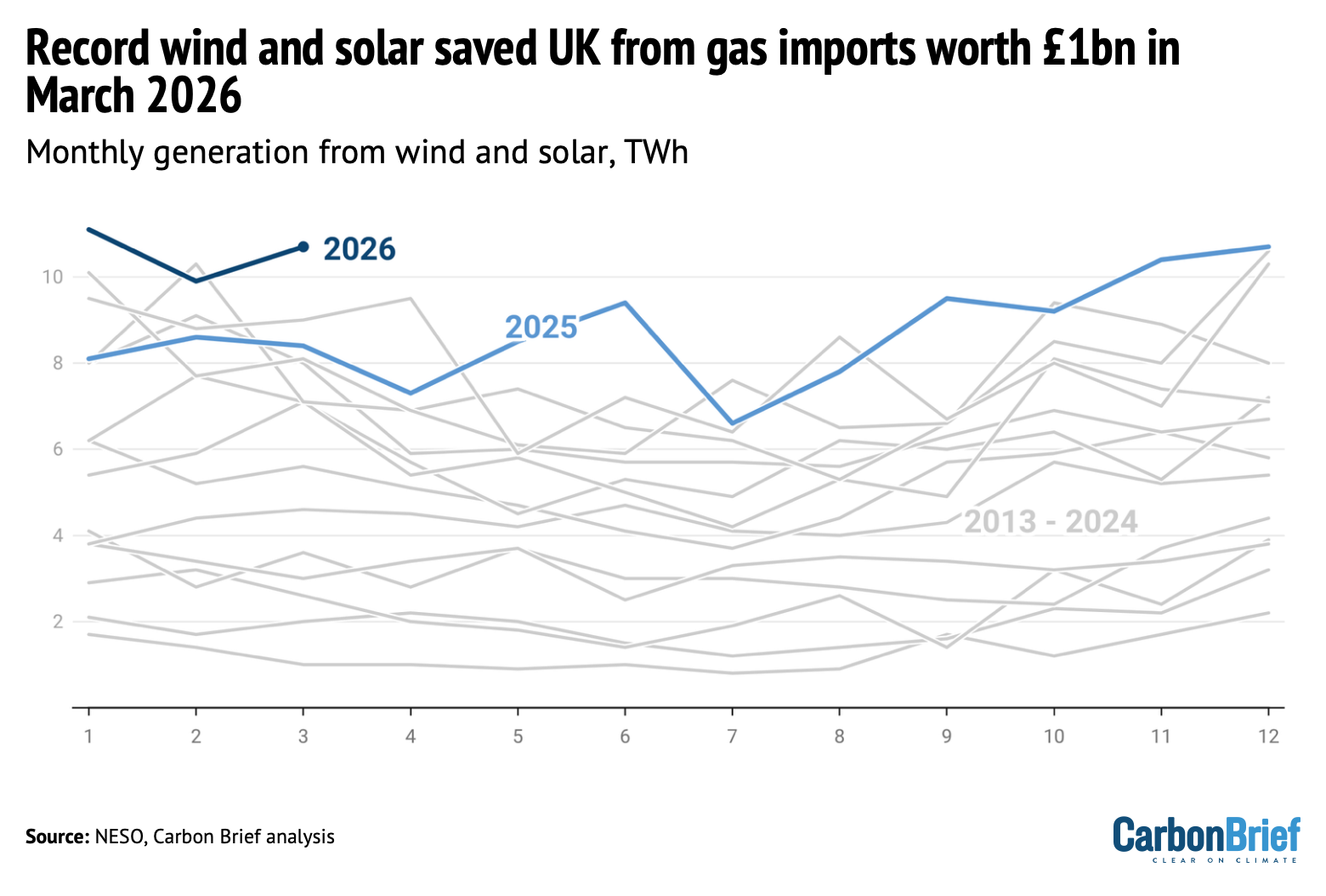

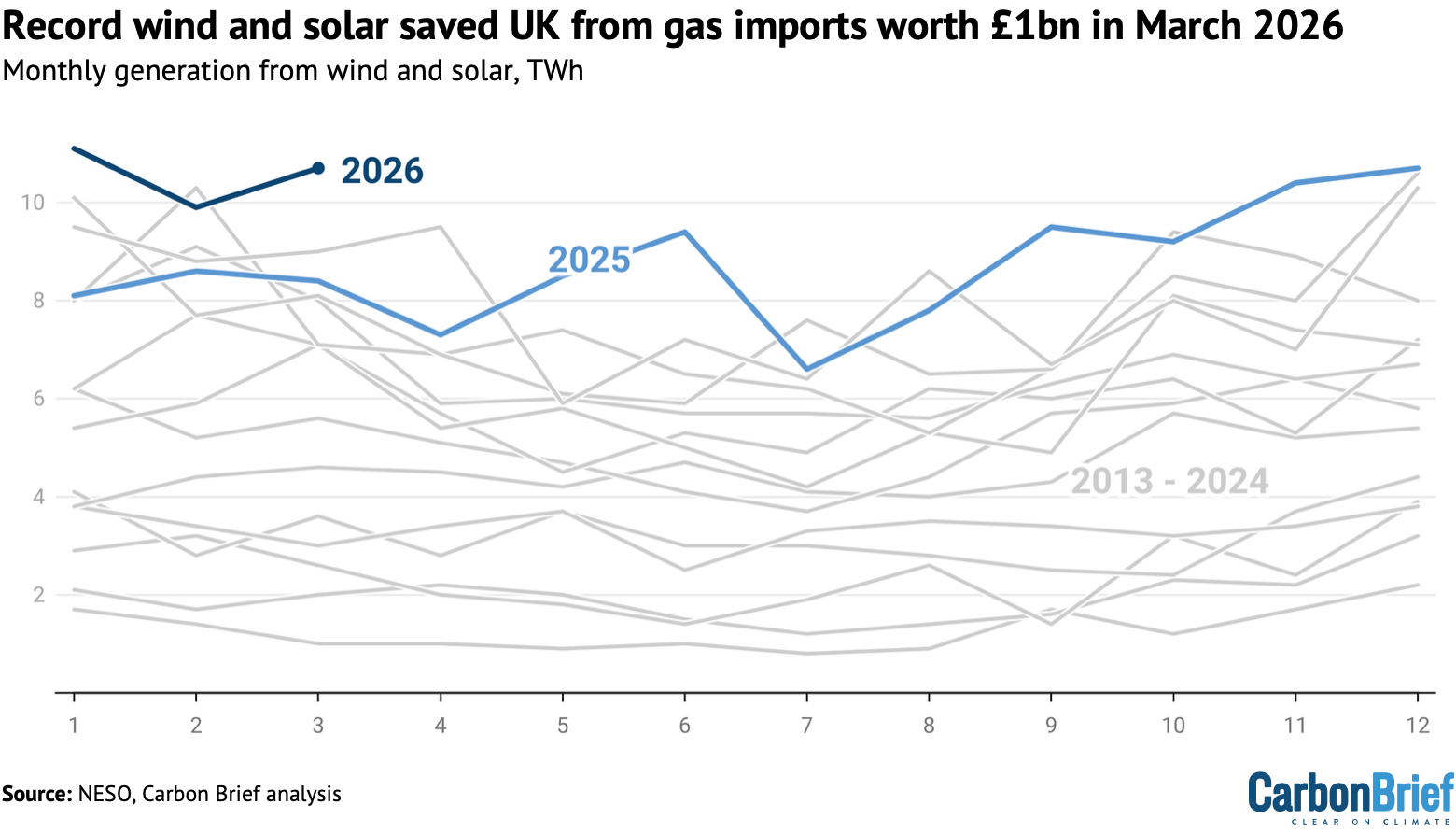

Carbon Brief analysis found that Great Britain has generated record levels of combined wind and solar output so far this year. The chart above shows monthly wind and solar output, which reached 11 terawatt hours (TWh) in March 2026. At current high gas prices, this saved the UK nearly £1bn worth of gas imports for the month, according to the analysis.

Spotlight

How ‘plug-in’ solar could reduce bills

This week, Carbon Brief analysis finds that plug-in solar panels could save a typical household £1,100 over a 15-year lifetime.

In response to the ongoing energy crisis, the UK government announced on 15 March a package of clean-energy measures to “boost” energy security. Among these was the introduction of “plug-in” solar panels to the UK.

Plug-in panels

Compared to rooftop solar, smaller plug-in solar systems consisting of one to two panels can be easily installed on balconies, in gardens and other outdoor spaces. They can be plugged directly into home sockets without the need for additional wiring, reducing electricity taken from the grid and thereby cutting bills.

Plug-in solar has already taken off in Germany, with official registrations already exceeding 1m installations (the actual number could be up to 4m). Other growing markets include France, Spain, the Netherlands and the US.

Panels could be available in the UK “within months” at retailers, such as Lidl and Sainsbury’s, according to the government. (Many of the products from EcoFlow, one of the main providers of plug-in solar in the UK, are already sold out online.)

The government said it will work with relevant bodies to update electrical regulations to allow the use of plug-in solar. The Institution of Engineering and Technology (IET) has advised homes to get their wiring checked before installing.

Costs and benefits

To assess the potential impact of plug-in solar, Carbon Brief conducted a cost-benefit analysis for an 800-watt (W) installation in a typical two-to-three bedroom home in London. The assumptions are approximate and will vary for different locations and set-ups.

Optimally placed panels – south-facing and tilted at around 40 degrees – would generate around 820 kilowatt hours (kWh) each year in London – at a “load factor” of 12% – according to the EU’s PVGIS database.

Actual output is likely to be lower, due to sub-optimal placement – such as vertically on balconies – as well as orientation and shading.

A report by trade body Solar Power Europe noted these factors could cut 30-60% from optimal output. This analysis assumes a 45% reduction from optimal output.

If a household is able to use 90% of the output – typical for such installations – then the panels would provide 400kWh of electricity each year, enough to meet 15% of typical demand.

This will vary on the household usage patterns, but running appliances such as washing machines during peak daylight hours could improve capture rates.

This could save £110 on electricity bills each year, meaning the upfront cost of around £500 could be paid back within 5 years, according to Carbon Brief’s analysis.

Assuming the panels last 15 years, total net savings over their lifetime could reach £1,100.

These savings assume a fixed unit cost of 27p/kWh, based on predictions for July 2026.

If electricity prices surged to 34p/kWh for a prolonged period – as they did during the 2022 gas price crisis – then annual savings could increase to around £140, further reducing the payback time.

If module costs fall over time as more suppliers enter the market, this could reduce the upfront cost and payback time.

If 3m households take up plug-in solar – comparable to Germany’s current deployment – this would generate 1.2 terawatt hours (TWh), less than 1% of UK demand.

While this would not significantly cut UK emissions overall, it could still save the households more than £330m in total and avoid around two tankers’ worth of imported liquified natural gas (LNG) each year, according to Carbon Brief’s analysis.

Unlocking participation

Aside from its economic benefits, plug-in solar could unlock participation in the clean-energy transition for a wider percentage of the population.

For example, renters make up around one-third of UK households and lack control over the installation of rooftop solar and heat pumps. Plug-in solar would enable them to engage in and benefit from clean energy in their homes.

This spotlight was also published on Carbon Brief’s website.

Watch, read, listen

HEAT HEADS: The BBC’s Climate Question podcast spoke to two women from Sierra Leone and Mexico about their role as “chief heat officers” for their cities.

OYSTER DIE-OFF: A feature in the Guardian explored how warming seas are causing mass die-offs of Japan’s oysters, threatening the shellfish trade.

SOLAR SWITCH: Climate Home News examined how Nigerian homes and businesses are increasingly switching from backup generators to solar power.

Coming up

- 8 April: International Energy Agency rare earth special report launch, Paris

- 10 April: Djibouti presidential election

Pick of the jobs

- Grantham Institute for Climate Change, research fellow | Salary: £49,017-£57,472. Location: London (hybrid)

- Stop Climate Chaos Scotland, advocacy lead | Salary: £35,000. Location: Scotland (remote)

- The 19th News,contract climate reporter | Salary: $50 per hour. Location: US (remote)

DeBriefed is edited by Daisy Dunne. Please send any tips or feedback to debriefed@carbonbrief.org.

This is an online version of Carbon Brief’s weekly DeBriefed email newsletter. Subscribe for free here.

The post DeBriefed 2 April 2026: Countries ‘revive’ energy-crisis measures | Record UK renewables | Plug-in solar savings appeared first on Carbon Brief.

The Intergovernmental Panel on Climate Change’s (IPCC) latest assessment cycle has been beset by disagreements between nations over the timeline for publishing its next landmark report.

During the UN climate science body’s last five “sessions” – biannual meetings where governments discuss matters related to the IPCC’s work – governments have been unable to sign off on the delivery date of the “working group” reports.

The deadlock over the delivery plan for the seventh assessment cycle (AR7) has been described as “unprecedented”.

Some countries have pushed for reports to be approved in 2028, in time to inform the “second global stocktake”, which is due to conclude at COP33 that year and is designed to inform the next round of national climate goals under the Paris Agreement.

Other nations have argued that developing countries need more time to review and approve the reports – meaning that one, or more, would not be published until after the stocktake.

The next IPCC meeting – due to take place in Addis Ababa in October – is likely the last moment where a timeline could be agreed that would see the reports synchronised with the stocktake.

One expert tells Carbon Brief that the failure to align the IPCC’s reports with the stocktake would be a “major historical break [that] would be used to weaken the international climate process and Paris Agreement”.

In this Q&A, Carbon Brief explores the ongoing disagreements over the AR7 timeline.

- How does the IPCC assessment report cycle work?

- How have timeline negotiations been different for AR7?

- Why have negotiations over the timeline of AR7 faltered?

- Why are some countries calling for a slower timeline for AR7 reports?

- How is the IPCC managing the impasse?

- Is delivering the reports in time for the global stocktake still possible?

- What could be the implications of an extended timeline for AR7?

How does the IPCC assessment report cycle work?

For almost 40 years, the IPCC has been one of the most visible examples of a “science-policy interface” – an institution that helps science to inform policy.

The UN General Assembly resolution that established the IPCC in December 1988 states that the panel will “provide internationally coordinated scientific assessments of the magnitude, timing and potential environmental and socioeconomic impact of climate change and realistic response strategies”.

Four years later, the UN Framework Convention on Climate Change (UNFCCC) was created, with an objective of “stabilising greenhouse gas concentrations at a level that would prevent dangerous anthropogenic [human-caused] interference with the climate system”.

The IPCC’s official rulebook, last updated in 2013, highlights the IPCC’s role in producing comprehensive assessments of the state of human-caused climate change. It stipulates that its assessments must provide “relevant” information – and that reports should be “neutral with respect to policy”.

The IPCC’s work has long helped inform the work of the UNFCCC, which meets annually for its “conference of the parties” (COP).

For example, the reports of the fifth assessment cycle (AR5), published over 2013-14, have been credited for informing the Paris Agreement’s headline goal to hold global temperature rise at “well below 2C” and “pursue efforts” to limit increases to 1.5C.

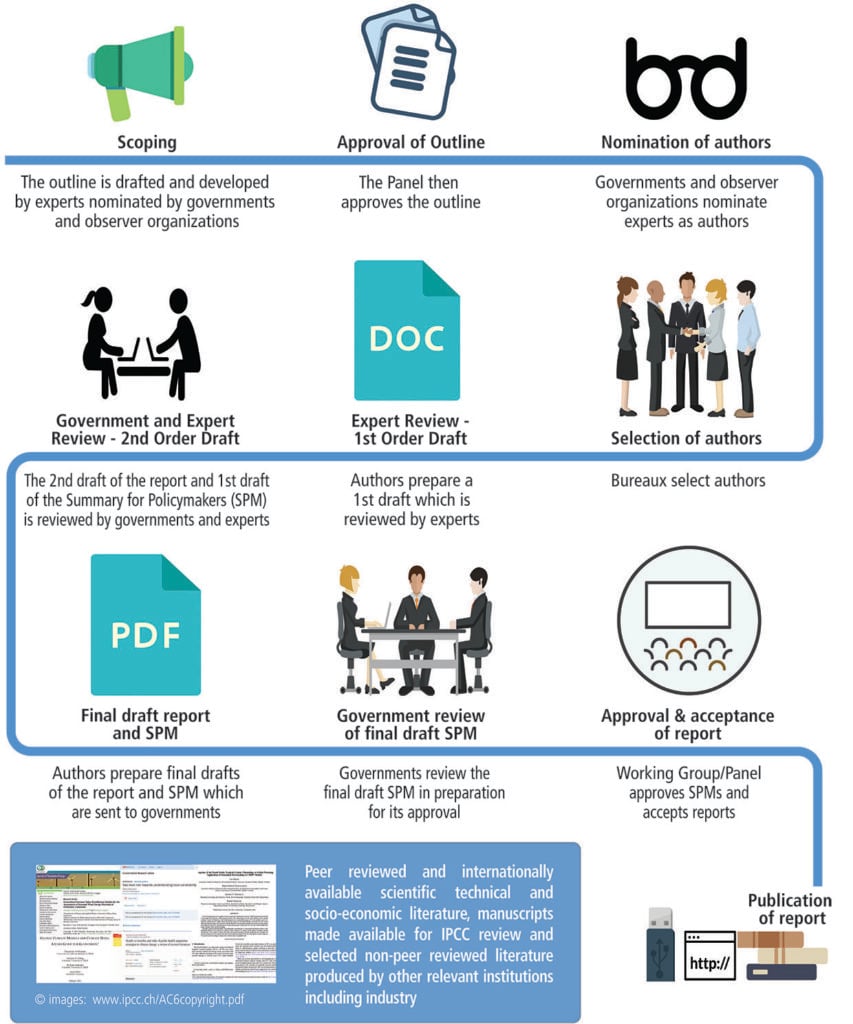

During each assessment cycle, the IPCC produces three “working group” (WG) reports on physical science (WG1), impacts and adaptation (WG2) and mitigation (WG3). These are summarised in a “synthesis” report (SYR). It also produces special reports and methodology reports.

There are a number of stages to the creation of an IPCC working group report, as shown in the graphic below.

How have timeline negotiations been different for AR7?

The current assessment cycle – AR7 – formally began in July 2023, at the IPCC’s 59th session (IPCC-59) in Nairobi.

In January 2024, governments agreed to publish the AR7 synthesis report in 2029.

However, governments are yet to ratify a timeline for publication of the working group reports that will precede it, after negotiations on the issue ended in deadlock in Istanbul, Sofia, Hangzhou, Lima and Bangkok.

This puts AR7 at odds with the previous assessment cycles, where timelines were agreed more quickly. This is shown in the table below.

| Assessment cycle | Start date | Report timeline agreed* | Time until decision | WG1 | WG2 |

WG3 | SYR |

|---|---|---|---|---|---|---|---|

| First | IPCC-1, Nov 1988 | IPCC-2, Jun 1989 | 7 months | Aug 1990 | Jun 1990 | Jun 1990 | Aug 1990 |

| Second | IPCC-7, Feb 1992 | IPCC-9, Jun 1993 | 1 year, 4 months | Dec 1995 | Oct 1995 | Oct 1995 | Dec 1995 |

| Third | IPCC-13, Sep 1997 |

IPCC-14, Oct 1998 | 1 year, 1 months | Jan 2001 | Feb 2001 | Mar 2001 | Sep 2001 |

| Fourth | IPCC-19, Apr 2002 | IPCC-21, Nov 2003 | 1 year, 8 months | Feb 2007 | Apr 2007 | May 2007 | Nov 2007 |

| Fifth | IPCC-28, Apr 2008 |

IPCC-31, Oct 2009 | 1 year, 5 months | Sep 2013 | Mar 2014 | Apr 2014 | Nov 2014 |

| Sixth | IPCC-42, Oct 2015 |

IPCC-46, Sep 2017 | 1 year, 11 months | Aug 2021 | Feb 2022 | Apr 2022 | Mar 2023 |

| Seventh | IPCC-59, Jul 2023 |

– | 2 years, 9 months and counting | – | – | – | 2029 |

“Report timeline agreed” refers to when delivery timeline of working group reports was agreed. WG = working group and SYR = synthesis report. Analysis by Carbon Brief.

Why have negotiations over the timeline of AR7 faltered?

Part of the disagreement over the AR7 timeline centres on the question of whether the IPCC’s seventh assessment cycle should align with the second global stocktake, a process that is due to culminate in the autumn of 2028 at COP33.

While a number of different timelines have been proposed, there are, broadly speaking, two camps in the AR7 timeline debate.

The first group has argued that all three working group reports should be published in 2028, so that they can inform the second global stocktake.

The other faction has advocated for a longer timeline, which would mean WG2 and WG3 would be finished after the stocktake is completed.

Established in 2015 under the Paris Agreement, the global stocktake is a five-yearly assessment of the world’s collective progress on tackling climate change. Under the terms of the treaty, countries pledged to consider the “best available science” during the process.

The first global stocktake concluded at COP29 in Dubai in 2023. Its outcomes informed national 2035 climate goals, which were due to the UN in 2025.

In the outcome decision of the first global stocktake, the UNFCCC officially invited the IPCC to consider how to “best align” with the “second and subsequent global stocktakes”.

The document also invited the IPCC to “provide relevant and timely information for the next global stocktake”.

Dr Bill Hare, CEO and senior scientist of Climate Analytics, tells Carbon Brief the stocktake is “at the guts, or heart, or the Paris Agreement’s ambition mechanism”.

He explains that the IPCC’s sixth assessment reports (AR6) – published over 2021-23 – were a “critical element” in the first global stocktake process:

“You had the IPCC reports there. You’ve had the IPCC co-chairs, or authors, in the discussions [and] workshops, pushing back on arguments from [countries]…They were able to anchor the fact that the world hasn’t done enough, that the NDCs [“nationally determined contributions”, or climate pledges] haven’t met the 1.5C goal by a wide margin – and that the cost of doing stuff is relatively cheap, which was a critical output of the WG3 report last time.”

Dozens of counties have advocated for a global stocktake-aligned timeline for AR7 reports, arguing that it is critical that findings from all working groups inform the exercise.

For example, the small-island state of Vanuatu said at IPCC-63 in Lima that delaying the reports would deprive countries of important scientific information ahead of key international meetings, according to the Earth Negotiations Bulletin (ENB), reporting from inside the meeting.

Meanwhile, the Netherlands said at IPCC-64 in Bangkok that the delivery of reports after the stocktake would “significantly lower the policy relevance of AR7”, according to ENB.

A timeline where the reports are published ahead of the stocktake has been backed by co-chairs of IPCC reports. (See: How is the IPCC managing the impasse?)

Hare says that, in his analysis, a timeline where the AR7 reports align with the stocktake is supported by the “majority of countries, across geographies and levels of development, including least developed countries and small-island developing states”.

However, a number of emerging-economy nations have argued that a timeline where all reports are delivered by 2028 is too tight.

Why are some countries calling for a slower timeline for AR7 reports?

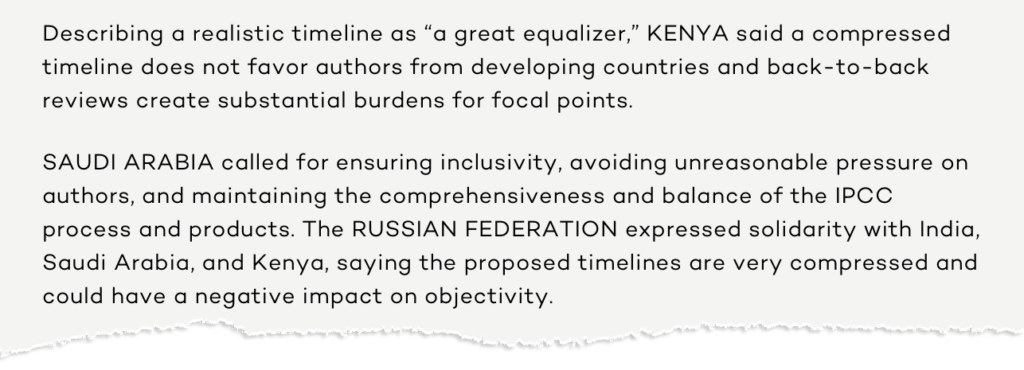

Among the most vocal proponents for the WG2 and WG3 reports being delivered after the stocktake, according to the ENB’s write-ups of negotiations in Bangkok and Lima, are India, Kenya, Russia and Saudi Arabia.

These countries have argued that authors, experts and governments from developing nations with fewer resources need more time to prepare, review and approve working group reports.

Some of the arguments in favour for a slower timeline are captured below in an excerpt from the ENB’s write-up of last October’s IPCC-63 in Lima.

An article published in 2025 in Africa Climate Insights summarised some of the arguments in favour of a slower timeline. It says a stocktake-aligned timeline would have overlapping review periods for different working group reports that would place more pressure on governments and experts.

It also notes that researchers from the global south – who face greater institutional barriers to publishing research in academic journals – would benefit from a later cut-off date for scientific literature for the AR7 reports. It quotes Dr Patricia Nying’uro – Kenya’s IPCC “focal point” – saying:

“The current timeline does not provide adequate time for developing countries to conduct research, publish their findings and have meaningful input.”

On top of citing inclusivity concerns, countries have also argued that aligning reports with the global stocktake is not an IPCC priority.

For instance, ENB reported at IPCC-64 that Saudi Arabia said “compressing” the cycle to meet “external timelines” would be “improper” because the IPCC “serves a broader mandate than just providing inputs to the global stocktake”.

Meanwhile, Russia said inputs to the global stocktake were “not the key to IPCC success”.

These arguments have faced significant pushback.

At IPCC-63 in Lima, IPCC co-chairs pointed out that overlapping reviews of assessment reports were “intentional” and would allow experts to see both drafts at once, according to ENB.

At the meeting, IPCC chair Prof Jim Skea also pointed to the IPCC rulebook, which states that panel and working group sessions should be scheduled to coordinate “to the extent possible, with other related international meetings”.

Some have contested the framing of a stocktake-aligned timeline as “compressed”.

At IPCC-61 in Sofia, the delegation from Saint Kitts and Nevis argued that the proposed schedule for AR7 was “neither compressed nor rushed”, because, while it was shorter than the schedule for AR6, it would contain fewer special reports.

Meanwhile, at IPCC-62 in Hangzhou, representatives from Luxembourg reminded the conference that AR6 was produced under “global pandemic conditions and was, therefore, delayed”, reported ENB. As such, they said the “proper comparison of the timeline would be to AR5, relative to which the proposed timetable was not rushed”.

(AR6’s seven-year run has been attributed in IPCC documents to the Covid-19 pandemic interrupting workflows and an unprecedented number of reports.)

There have been accusations in some quarters that delegations advocating in favour of a slower timeline are deliberately stalling the process.

For example, in a statement released after the meeting, the French government expressed its “deep concern over attempts to arbitrarily slow down and postpone the publication schedule”.

It said that “any delay in taking into account the relevant scientific data to respond to the climate emergency would seriously compromise climate action on a global scale”.

Some observers have argued that dynamics playing out at the IPCC replicate those in UN climate negotiations. Yao Zhe from Greenpeace East Asia tells Carbon Brief:

“The group of countries that opposed the proposed AR7 timelines is similar to the group that tactically slowed down or blocked negotiations regarding mitigation ambition under the UNFCCC. And they are gaining more influence as global climate governance faces a leadership vacuum.”

Dr Kari de Pryck, a lecturer at the Institute for Environmental Sciences at the University of Geneva, tells Carbon Brief that, “clearly, there is obstruction”. She continues:

“It is in the interest of some countries to ensure that the IPCC reports are not published on time. But there are also interesting and legitimate comments on inclusivity and diversity.”

How is the IPCC managing the impasse?

Despite no formal timeline for report delivery being agreed, report production has continued undeterred, IPCC chair Prof Jim Skea tells Carbon Brief.

He says that, so far, the science “has not been held up” by the report timeline issue, with lead author meetings and drafting of the various working group, special and methodological reports underway.

However, he warns that a final decision will need to be made by the end of 2026 on a timeline. He explains:

“There are multiple proposals that have been made [on timelines] and they start to diverge during 2027 due to the scheduling of specific events, like lead author meetings and review periods. Because we need to establish a budget for 2027, we need to make a decision before the end of 2626 to have some certainty about the entire cycle.

“So far, we’ve operated by taking year by year decisions – you just take the decision for the next year and carry on. That’s been okay so far, because there has not been a divergence [between timeline proposals] at the earlier stages of the cycle. But we will see divergences coming up.”

At IPCC-63 last October, WG1 co-chair Dr Robert Vautard noted that reports production was currently aligned with a schedule that had been “considered” in the previous meeting in Hangzhou. He said this timeline would allow final approval sessions for WG1, WG2 and WG3 to take place in May 2028, June 2028 and July 2028, respectively.

After this timeline failed to garner consensus, WG1 co-chair Dr Xiaoye Zhang and WG2 co-chair Dr Bart Van den Hurk then presented a new “compromise” timeline to delegates.

This extended the expert and government review periods for draft reports and pushed final approval sessions for WG2 and WG3 to July 2028 and September 2028. Discussions about this updated timeline ended in deadlock.

At IPCC-64 in Bangkok in March 2026, the timeline for reports was initially not slated for discussion.

However, an item on “progress on AR7 reports” was added to the agenda on the first day of the conference, after some countries said the issue required structured discussion. In the end, no agreement was reached on how resolution could be reached.

Negotiations have been pushed – alongside a number of other unresolved decisions – to IPCC-65, scheduled to take place in Addis Ababa, Ethiopia, in October 2026.

Skea says the lack of agreement on a way forward in Bangkok leaves the secretariat with the “responsibility to try and figure out the process that will move us in the right direction”. He adds:

“Is there a bridging proposal, some kind of scheme that would help to bring the sides together? That’s what we need to work on over the next few months.”

A key issue the secretariat will need to consider is how to address a “loss of trust between different groups of countries”, as well as the “technicalities of how the timeline is constructed”, he says.

Is delivering the reports in time for the global stocktake still possible?

The IPCC maintains that delivering reports in time for the next global stocktake remains possible, if a decision is made by the end of this year.

Speaking to Carbon Brief, Skea says all timeline options in contention are still feasible “in principle”, if countries show flexibility. He counts four different proposals – two of which would see all reports produced before the stocktake in 2028 and two where WG2 and WG3 would be published in 2029.

He says, though, that he is optimistic a “constructive” result can be delivered in Addis Ababa – but stresses it will only be possible with “a lot of hard work”.

Experts have noted that, even if reports are published in 2028, they will come later in the stocktake process.

Dr Matti Goldberg, director of international climate policy at the Woodwell Climate Research Center and former staffer at the UNFCCC secretariat, explains:

“It is already kind of late. If you want to have a meaningful consideration of the IPCC reports in the global stocktake, they need to be there now or at the beginning of the information collection stage. Otherwise, you’ll have a bunch of parties saying: ‘No, can’t do it. It is too short a timeframe, too big a report.’”

The global stocktake is a process that is split into three phases: an information collection phase to gather inputs; a technical assessment of inputs and other evidence; and a “consideration of outputs” phase where countries decide what to collectively take away from the process.

The information phase of the second global stocktake is due to kick off at COP31 in Antalya, Turkey in November 2026. The technical assessment phase will take place from June 2027 to June 2028, giving way to the final political phase that culminates at COP33 in November 2028.

Under the revised AR7 timeline proposed by IPCC co-chairs in Lima, WG1 would be ready during the technical phase of the second global stocktake and WG2 and WG3 would be able to inform its final, political phase.

Goldberg emphasises that the publication of the reports – and their respective summaries for policymakers – in 2028 would mean countries would face “much higher pressure to deliver stronger messages of ambition” in the second global stocktake.

However, he adds that a faster timeline for the reports will not change the “fundamental calculations of interest” that shape international climate politics:

“There are a series of negotiations: first, over the summary of policymakers and then throughout the whole global stocktake. In the end, that is the process that determines a lot of the result.”

De Pryck from the University of Geneva similarly notes that scientific input is not “the only input” to the stocktake:

“It is a political process. So, at the end of the day, science and expertise is very important – but it’s not going to translate directly into the global stocktake.”

What could be the implications of an extended timeline for AR7?

If AR7 reports are not published until after the global stocktake, governments would likely turn to other sources of science in their submissions, experts tell Carbon Brief.

De Pryck explains that a broad range of science was submitted by governments to the first global stocktake. She says this includes the UN Environment Programme’s annual adaptation and emissions gap reports; updates from the International Energy Agency and climate-finance analysis from Oxfam:

“There are quite a lot of other academic and epistemic reports that could be used by countries in the negotiations that, in a way, could support what the IPCC is doing.”

Greenpeace Asia’s Yao Zhe notes that AR7’s special report on climate change and cities, due to be published in 2027, could play a “good scientific basis” for policy discussions around climate mitigation in the absence of the WG3 report from the stocktake.

Climate Analytics’ Bill Hare warns that a failure to align the the IPCC cycle with the global stocktake could result in less robust science being considered:

“There’s a general consensus that the IPCC is the best available science. It is the formal science, if you like, delivered to the Paris Agreement and climate convention. So, if that doesn’t happen, then it opens the space for other sources of so-called science to come in.”

He adds that any disconnect between the global stocktake cycle and the IPCC assessment cycle would be a “major historical break and one which would be used to weaken the international climate process and Paris Agreement”.

The impacts would also be felt within the climate science community, Hare continues. The IPCC’s role in advising the UNFCCC has long provided a “really strong sense of relevance” to many climate scientists, he says:

“That relevance is a very strong motivator for what [scientists] do. I wonder whether the failure of the IPCC to agree timetable alignment would have a negative impact on that. And that wouldn’t be just for this global stocktake cycle, it would be for subsequent ones.”

The post Q&A: Why the standoff between nations over the next IPCC reports matters appeared first on Carbon Brief.

Q&A: Why the standoff between nations over the next IPCC reports matters

The UK avoided the need for gas imports worth £1bn in March 2026 thanks to record electricity generation from wind and solar, reveals Carbon Brief analysis.

Wind generation hit a new record for the month of March on the island of Great Britain, up 38% year-on-year, while solar nearly matched the output of last year’s exceptionally sunny spring.

Together, wind and solar generated 11 terawatt hours (TWh) of electricity in March 2026, up a combined 28% and setting a new record for the month, as shown in the figure below.

This record wind and solar output avoided the need to import 21TWh of gas – roughly 18 fully loaded tankers of liquified natural gas (LNG) – which would have cost around £1bn at current high prices due to the Iran war.

(This is based on gas costing 130p per therm, or £44 per megawatt hour, compared with the range of 120-170p per therm seen over the past month.)

At the same time, the record output from wind and solar saw electricity generation from gas falling 25% year-on-year in March 2026 to the lowest level ever recorded for the month.

This meant that gas was setting the price of electricity roughly 25% less often in March 2026 than in the same month in 2022, when fossil-fuel prices spiked after Russia’s invasion of Ukraine.

The post Analysis: Record wind and solar saved UK from gas imports worth £1bn in March 2026 appeared first on Carbon Brief.

Analysis: Record wind and solar saved UK from gas imports worth £1bn in March 2026

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Renewable Energy5 months ago

Renewable Energy5 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits