Goldman Sachs Asset Management (GSAM) has launched its new Emerging Markets Green and Social Bond Active UCITS ETF, known as GEMS. This ETF focuses on green and social bonds issued by both governments and companies in emerging markets. It has an expense ratio of 0.55%. This gives investors a cost-effective way to back environmental and social projects. At the same time, they can aim for solid financial returns.

GEMS is now on major European stock exchanges. This shows GSAM’s strong move into sustainable investment solutions. Hilary Lopez at Goldman Sachs Asset Management stated:

“Our clients are showing continued demand for access to leading active capabilities, combined with the control and convenience of ETFs. Following the launch of our core active Fixed Income and Equity building blocks, we are leveraging the leading capabilities and expertise of our Green, Sustainable, Social & Impact Bonds Team to help investors diversify their fixed income exposure and drive impact across emerging markets.”

Green Gold Mines: Why Emerging Markets Are ESG Hotspots

Emerging markets face serious issues like limited infrastructure, poverty, and pollution. That’s why they are a strong focus for investors looking to make a difference. These markets often offer high-impact opportunities where green and social projects—such as clean energy or affordable housing—can create immediate change.

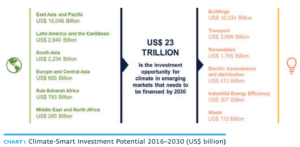

According to the International Finance Corporation, emerging markets could see up to $23 trillion in climate-focused investments by 2030. These investments not only help reduce environmental harm but also offer strong growth potential. GEMS helps investors make a real impact by focusing on these regions. This way, they can support change and enjoy long-term financial growth.

Many investors now prefer funds that consider Environmental, Social, and Governance (ESG) factors. Globally, ESG-focused investments already exceed $17 trillion. As this trend continues, products like GEMS are appealing to investors. They seek both returns and impact.

How Do Green and Social Bonds Work?

Green bonds raise funds for projects that protect the environment. These may include wind farms, solar panels, or clean transport systems. Social bonds support efforts like building schools, improving access to clean water, and offering affordable health services.

The GEMS ETF invests in both types. This approach helps the fund tackle environmental and social issues at the same time. The green bond market alone has surpassed $2 trillion, showing strong investor interest. Social bonds are also growing quickly as governments and businesses seek to address social problems more directly.

GEMS takes an active management approach, unlike many passive ETFs. The fund’s team picks and adjusts the bond portfolio. They focus on sustainability goals and future expectations. This strategy helps avoid weak projects and gives the ETF the flexibility to focus on high-quality investments.

Carbon Cuts and Climate Gains: GEMS’ Impact Strategy

Emerging markets often have large carbon footprints because of their heavy use of fossil fuels and rapid development. GEMS helps fight this by investing in clean energy, energy savings, and other projects that lower emissions. These green projects can make a big difference in reducing global carbon levels.

Goldman Sachs uses strict screening methods to make sure the bonds they include actually help the environment. This reduces the risk of “greenwashing,” where projects claim to be green without real proof.

Social investments also have climate benefits. For example, housing projects in the fund might use energy-saving designs. Better healthcare and education help communities handle extreme weather and other climate-related stresses.

Global Trends in ESG Bond Markets

As climate finance needs reach an estimated $1.3 trillion a year, markets are searching for greater accountability and measurable impact. Sustainable bond markets are expected to play a key role. Emerging markets are taking steps, like ASEAN and Latin American green taxonomies. These initiatives create new chances for different issuers.

GEMS now joins a growing asset class. It helps meet the demand for strong, impact-focused bond investments in high-growth markets. Moreover, the GEMS ETF enters the market at a time when sustainable bonds are quickly becoming mainstream investment tools.

Analysts expect that by 2025, about 30% of global bond sales may be green or social. That’s a large shift toward combining financial growth with responsibility.

In emerging markets in 2023, green bond issuance grew 45% year-over-year, totalling $135 billion. Meanwhile, broader GSSS issuance exceeded $1 trillion, reaching 2.5% of global bond issuance.

Amundi forecasts GSSS bond issuance in emerging markets to grow around 7% annually through 2025. Globally, green bonds outperformed traditional bonds by about 2% in 2024 and reached a record issuance of $447 billion, reaching another milestone in 2024.

What Sets GEMS ETF Apart

GEMS fits this trend by offering diverse exposure to sustainable bonds in fast-growing economies, backed by GSAM’s decade-long ESG and emerging market bond expertise.

GSAM brings over a decade of experience in fixed income and ESG investing. Their skilled team can spot strong projects in places that may carry more risk, such as developing countries. This gives them an edge in finding value while managing potential problems like currency shifts or political changes.

Also, GEMS being listed on major European exchanges—like the London Stock Exchange, Borsa Italiana, and Deutsche Börse—makes it easy to access. It works for both institutional investors and individuals seeking access to emerging markets and sustainable finance.

Why Active ESG Investing Matters

Emerging markets can be unpredictable. Governments may change policies quickly, and local currencies can be unstable. By using an active management strategy, GSAM’s team responds to these shifts and adjusts the fund accordingly.

This hands-on approach is vital for maintaining a strong mix of bonds that aim for both social impact and solid returns. It helps avoid poor-performing investments and directs funds into projects that truly meet ESG standards.

For investors looking for growth, social impact, and environmental gain all in one, GEMS may be worth considering. The ETF balances risk by spreading investments across different countries and sectors in the emerging world. It’s also competitive from a cost point of view, helping make sustainable investing more accessible.

As more money shifts to ESG goals, sustainability is becoming mainstream in finance. Tools like GEMS will probably have a bigger impact. Investors now have an efficient option for putting their money into the areas of the world that need it most, helping build a more sustainable future while also seeking steady financial performance.

- READ MORE: The Rise of Sustainable Investing: Why It Is Winning Over Young Investors (and Big Money)

The post Goldman Sachs Launches Green Bonds ETF for Emerging Markets appeared first on Carbon Credits.

Carbon Footprint

History Repeating Itself: Why Middle East Conflict at the Pump Should Be a Wake-Up Call for North America

Disseminated on behalf of Surge Battery Metals.

Every time instability erupts in the Middle East, North Americans feel it where it hurts most—at the gas pump. It happened in 1979, when the Iranian Revolution sent shockwaves through global energy markets. Oil supplies tightened. Prices surged, and inflation followed. Entire economies slowed under the pressure.

For millions of households, the crisis’s impact was personal. It showed up in longer lines at gas stations and rising costs across daily life.

Nearly five decades later, the pattern is repeating.

Renewed tensions across key oil-producing regions are once again tightening global supply. Prices are rising. Consumers are feeling the impact. And once again, events unfolding thousands of miles away are shaping the cost of energy at home.

This pattern suggests a persistent structural vulnerability in North America’s exposure to global oil‑supply shocks. The region still depends heavily on global oil markets. That means supply disruptions, no matter where they occur, can quickly ripple through the system.

The result is a familiar cycle: geopolitical instability leads to supply concerns, which drive up prices, which then feed directly into the cost of living.

A Cycle Consumers Know All Too Well

When prices spike, households adjust. Commuters rethink travel. Businesses absorb higher costs or pass them on. Inflation pressures build. The impact spreads far beyond the energy sector.

With average gasoline prices currently around $4 per gallon in the US ($5.50 in California), or roughly $1.05 US per liter ($1.45 in California), the connection between global events and local fuel prices is no longer theoretical – it is a lived experience. This is why energy security is increasingly framed as both a policy concern and a kitchen‑table issue.

The events of 1979 were a warning. Today’s rising prices are another. The difference is that North America now has more options than it did back then.

Electric vehicles, battery storage, and renewable power systems are no longer future concepts. They are already part of the energy mix. And for those who have made the shift, the experience is very different, and the transition is already complete.

Instead of watching fuel prices climb, they are plugging in.

Graham Harris, Chairman of Surge Battery Metals, has spoken openly about this shift in practical terms. While rising oil prices create uncertainty at the pump, he charges his electric vehicle at home.

The contrast between gasoline dependency and electrification is becoming more visible.

When oil prices rise, gasoline costs follow. But electricity prices tend to be more stable, especially when supported by domestic generation and renewable sources. That difference is simple but powerful. It changes how people experience energy volatility.

One system is exposed to global shocks. The other is increasingly tied to domestic infrastructure. This contrast highlights how the energy transition is reshaping exposure to global price shocks.

Some analysts increasingly frame the energy transition not only as a climate imperative but also as a strategy to reduce exposure to external risk. It relates to questions of control over where energy comes from, how it is produced, and how stable it is over time.

And at the center of that transition is one critical material: lithium.

Lithium: The Foundation of Energy Independence

Lithium is the core component of modern battery technology. It powers electric vehicles, supports grid-scale energy storage, and plays a growing role in advanced defense systems.

As electrification expands, demand for lithium is rising across multiple sectors.

But here is the challenge: much of today’s lithium supply still comes from outside the United States. This creates a familiar dynamic.

Just as oil dependency has long exposed North America to geopolitical risk, reliance on foreign lithium supply introduces a new layer of vulnerability. The commodity is different, but the structure is similar.

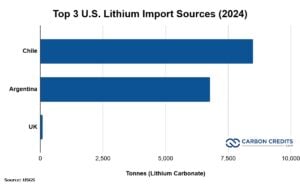

The United States imported the majority of its lithium from Chile and Argentina in 2024. Together, they accounted for roughly 98% of the total supply. Smaller volumes were sourced from the UK, France, and China.

That is why domestic production is becoming a central focus of energy and industrial policy.

In March 2025, Donald Trump signed an executive order titled “Immediate Measures to Increase American Mineral Production.” The directive called for faster permitting, expanded development, and reduced reliance on foreign supply chains for critical minerals.

The message of the order was clear: building domestic capacity is now a strategic priority.

- RELATED: Live Lithium Prices Today

A Domestic Resource Takes Shape in Nevada

Within this broader shift, projects like Surge Battery Metals’ (TSX-V: NILI | OTCQX: NILIF) Nevada North Lithium Project (NNLP) are gaining attention.

NNLP hosts a measured and indicated resource of 11.24 million tonnes of lithium carbonate equivalent (LCE) at an average grade of 3,010 ppm lithium, based on company disclosures. This makes it the highest-grade lithium clay resource identified in the United States to date.

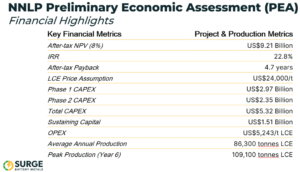

A 2025 Preliminary Economic Assessment (PEA) outlines the project’s scale:

- After-tax NPV (8%): US$9.21 billion

- Internal Rate of Return (IRR): 22.8%

- Mine life: 42 years

- Average annual production: ~86,300 tonnes LCE

- Employment: ~2,000 construction jobs and ~350 long-term operational roles

These figures indicate potential in terms of scale, longevity, and the ability to contribute to domestic supply if the project moves forward. At full production, NNLP has the potential to rank among the larger lithium-producing assets globally, based on third-party analysis.

Recent drilling results announced by Surge Battery Metals have further strengthened NNLP’s profile as a standout asset. In February 2026, step-out drilling found a 31-meter intercept with 4,196 ppm lithium from surface. This is much higher than the project’s average of 3,010 ppm Li. It also extends high-grade mineralization nearly 640 meters beyond the current resource boundary.

Infill drilling showed a steady, thick, high-grade core. It included intercepts like 116 meters at 3,752 ppm Li and 32 meters at 4,521 ppm Li. These results support future resource expansion. They also highlight the project’s scale, quality, and technical readiness as it prepares for a Pre-Feasibility Study.

Beyond the project itself, it reflects a broader policy and industry shift toward building more domestically anchored energy systems.

From Oil Dependency to Mineral Security

The connection between oil and lithium is not always obvious at first glance. Oil fuels internal combustion engines, while lithium supports batteries and energy‑storage systems, with distinct technologies and supply chains.

But the underlying issue is the same. Dependence on external sources creates exposure to external risk.

In the case of oil, that risk has played out repeatedly over decades. Supply disruptions, price shocks, and geopolitical tensions have all shaped the market.

With lithium, the industry is earlier in its development. But the stakes are rising quickly.

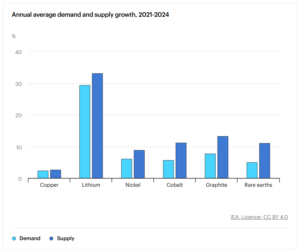

Global demand for lithium grew about 30 % in 2024, driven mainly by batteries for electric vehicles and energy storage, according to IEA data. Demand in 2025 continued at high rates, and under current policies, lithium demand is projected to grow fivefold by 2040 compared with today.

At the same time, supply growth is struggling to keep pace with demand forecasts. These trends show that ensuring a stable, secure supply is becoming just as important as expanding production.

That is where domestic projects come in, such as Surge Battery Metals’ NNLP.

They may not eliminate global market dynamics, but they can reduce exposure to them. They can provide a buffer against volatility. And they can support a more stable, self-reliant energy system.

A Turning Point – or Another Warning?

While history does not repeat in the same way, similar patterns can be observed.

The oil shocks of the 1970s revealed a vulnerability that shaped energy policy for decades. Today’s market signals are pointing to a similar challenge—this time at the intersection of oil dependency and critical mineral supply.

The difference is that the range of policy and technological options available today is broader. Electrification is already underway. Battery technology is advancing. Domestic resource development is gaining policy support. The pieces are in place.

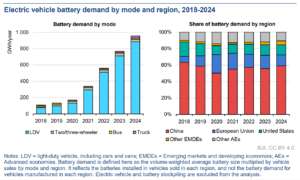

Data from the International Energy Agency’s Global EV Outlook 2025 shows that global battery demand reached a historic milestone of 1 terawatt-hour (TWh) in 2024. This surge was mainly due to the growth of electric vehicles (EVs).

By 2030, demand is expected to more than triple, exceeding 3 TWh under current policies. This reflects not only rising EV adoption but also expanding stationary storage demand. Both of which rely on critical minerals like lithium.

Electric vehicles continue to displace traditional oil use as well. The same IEA analysis shows that by 2030, EVs will replace over 5 million barrels of oil daily. This is about the size of a major country’s transport sector, highlighting how electrification is changing energy markets.

What remains uncertain is the pace at which these changes will occur.

Will rising fuel prices once again fade as markets stabilize? Or will they serve as a catalyst for deeper structural shifts?

That question matters not just for policymakers or investors, but for everyday consumers.

Because at the end of the day, energy transitions are not measured in policy papers. They are measured in daily decisions—how people power their homes, fuel their vehicles, and respond to rising costs.

DISCLAIMER

New Era Publishing Inc. and/or CarbonCredits.com (“We” or “Us”) are not securities dealers or brokers, investment advisers, or financial advisers, and you should not rely on the information herein as investment advice. Surge Battery Metals Inc. (“Company”) made a one-time payment of $75,000 to provide marketing services for a term of three months. None of the owners, members, directors, or employees of New Era Publishing Inc. and/or CarbonCredits.com currently hold, or have any beneficial ownership in, any shares, stocks, or options of the companies mentioned.

This article is informational only and is solely for use by prospective investors in determining whether to seek additional information. It does not constitute an offer to sell or a solicitation of an offer to buy any securities. Examples that we provide of share price increases pertaining to a particular issuer from one referenced date to another represent arbitrarily chosen time periods and are no indication whatsoever of future stock prices for that issuer and are of no predictive value.

Our stock profiles are intended to highlight certain companies for your further investigation; they are not stock recommendations or an offer or sale of the referenced securities. The securities issued by the companies we profile should be considered high-risk; if you do invest despite these warnings, you may lose your entire investment. Please do your own research before investing, including reviewing the companies’ SEDAR+ and SEC filings, press releases, and risk disclosures.

It is our policy that information contained in this profile was provided by the company, extracted from SEDAR+ and SEC filings, company websites, and other publicly available sources. We believe the sources and information are accurate and reliable but we cannot guarantee them.

CAUTIONARY STATEMENT AND FORWARD-LOOKING INFORMATION

Certain statements contained in this news release may constitute “forward-looking information” within the meaning of applicable securities laws. Forward-looking information generally can be identified by words such as “anticipate,” “expect,” “estimate,” “forecast,” “plan,” and similar expressions suggesting future outcomes or events. Forward-looking information is based on current expectations of management; however, it is subject to known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those anticipated.

These factors include, without limitation, statements relating to the Company’s exploration and development plans, the potential of its mineral projects, financing activities, regulatory approvals, market conditions, and future objectives. Forward-looking information involves numerous risks and uncertainties and actual results might differ materially from results suggested in any forward-looking information. These risks and uncertainties include, among other things, market volatility, the state of financial markets for the Company’s securities, fluctuations in commodity prices, operational challenges, and changes in business plans.

Forward-looking information is based on several key expectations and assumptions, including, without limitation, that the Company will continue with its stated business objectives and will be able to raise additional capital as required. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated, or intended.

There can be no assurance that such forward-looking information will prove to be accurate, as actual results and future events could differ materially. Accordingly, readers should not place undue reliance on forward-looking information. Additional information about risks and uncertainties is contained in the Company’s management’s discussion and analysis and annual information form for the year ended December 31, 2025, copies of which are available on SEDAR+ at www.sedarplus.ca.

The forward-looking information contained herein is expressly qualified in its entirety by this cautionary statement. Forward-looking information reflects management’s current beliefs and is based on information currently available to the Company. The forward-looking information is made as of the date of this news release, and the Company assumes no obligation to update or revise such information to reflect new events or circumstances except as may be required by applicable law.

The post History Repeating Itself: Why Middle East Conflict at the Pump Should Be a Wake-Up Call for North America appeared first on Carbon Credits.

Most businesses have a clear picture of what happens inside their own operations. They track energy consumption, manage waste, and monitor the emissions produced on-site. What they often cannot see is everything that happens before a product reaches their facility, and everything that happens after it leaves.

![]()

History Repeating Itself: Why Middle East Conflict at the Pump Should Be a Wake-Up Call for North America

Analysis: Record wind and solar saved UK from gas imports worth £1bn in March 2026

China Briefing 2 April 2026: EV profits rise | Ming Yang rejected | Iran war

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Renewable Energy5 months ago

Renewable Energy5 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits