Ford Motor Company (NYSE: F) is on a major mission to electrify its future. Once known for iconic gas-powered vehicles like the Mustang and F-150, the automaker is now aiming to become a global leader in electric mobility. This shift comes with a long-term environmental pledge—Ford plans to reach carbon neutrality by 2050, aligning with the Paris Climate Agreement and science-based targets.

Ford Shifts Gears Toward an Electric Future

To kickstart this transition, Ford invested over $11.5 billion in EV development till 2022 and has since significantly increased its commitment. The company’s strategy targets a complete overhaul of how vehicles are designed, built, and powered, paving the road for a cleaner, more sustainable auto industry.

The top car maker boosted its electric vehicle investment to $29 billion through 2025, reinforcing its commitment to an electric future. Rather than starting from scratch like some EV startups, Ford is electrifying its most popular existing models—vehicles that consumers already trust and love.

Key investments include electric versions of the Mustang Mach-E and the F-150 Lightning. These vehicles symbolize Ford’s approach: innovate within tradition and meet customer expectations while reducing emissions.

Mustang Mach-E and F-150 Lightning Lead the Charge

Ford’s strategy is paying off in real numbers. In 2024, the Mustang Mach-E outsold the traditional gas-powered Mustang, with over 51,000 electric units sold compared to 44,000 gas models. This is a clear sign that consumers are embracing electrification when it comes in familiar packages.

The F-150 Lightning, Ford’s all-electric pickup, has also made waves. With over 200,000 reservations by late 2021, demand exceeded early production capacity, leading to a multi-year waitlist. The Lightning’s ability to tow heavy loads and even power homes during outages has made it a standout in the EV truck segment.

However, the road hasn’t been entirely smooth. In April 2025, Ford’s EV sales dropped 39.4% compared to the same month in 2024, showing the competitive and evolving nature of the EV market.

Inside Ford’s Science-Based Carbon Neutral Roadmap

Ford’s climate plan targets the full lifecycle of its vehicles, focusing on the three biggest sources of emissions:

- Vehicle use (Scope 3)

- Supplier manufacturing

- Ford’s global operations

Combined, these areas represent around 95% of the company’s carbon footprint. Ford’s roadmap includes switching all its manufacturing to 100% renewable electricity by 2035, and as of 2023, over 70% of its global operations already run on carbon-free energy.

From 2010 to 2017, Ford cut more than 3.4 million metric tons of manufacturing emissions, equal to taking over 728,000 cars off the road for a year. The company achieved this through efficiency upgrades like LED lighting and streamlined paint systems.

Green Bonds and Clean Financing

To fund its EV and climate goals, Ford issued $4.25 billion in green bonds since 2021, the largest green bond offering by a U.S. non-financial company. These funds are being used to support EV production, battery development, and clean transportation infrastructure.

The company also ties its credit facilities to specific environmental targets, including renewable energy use and vehicle emissions.

Tackling Legacy and Supply Chain Hurdles

As a traditional automaker, Ford must revamp decades of operations, from factories to supplier networks. CEO Farley emphasizes that success in this era isn’t just about electric motors; it’s also about mastering software, digital services, and new customer experiences.

Ford has separated its EV and gas vehicle businesses to compete more efficiently with EV-first companies.

Ford is also working with suppliers to cut emissions. In 2024, 377 suppliers reported their carbon data, up 20% from 2022. The company aims to purchase 10% low-carbon aluminum and near-zero steel by 2030 and is part of the First Movers Coalition pushing for cleaner materials across industries.

Solving Charging Challenges with a Strong Network

Charging remains one of the biggest hurdles for EV adoption, and Ford is tackling it head-on. The company created the Blue Oval Charge Network, which now includes over 106,000 chargers across North America.

In a major move, Ford partnered with Tesla, giving Ford EV owners access to 15,000+ Tesla Superchargers. This expanded network helps eliminate range anxiety and makes long-distance travel easier for Ford drivers.

The FordPass app offers real-time access to charging station locations, availability, and payment, streamlining the entire process for users.

Taking On Tesla and New Global Rivals

Tesla still leads the U.S. EV market with a 43.4% share in Q1 2025, although that’s down from 51% the previous year. Ford is trying to close the gap by offering electrified versions of its most recognized vehicles—a contrast to Tesla’s approach of creating entirely new models.

Ford CEO Jim Farley has pointed out that Chinese automakers like BYD and Geely are emerging as the most serious competition globally. These companies are flooding markets with affordable, high-tech EVs and are gaining traction in multiple regions.

Read Farley’s comments on EV rivals

Ford’s Stock (F) Watch: Solid Dividends Amid EV Losses

Ford stock (NYSE: F) closed at $10.48 on June 25, 2025, up 16% from the start of 2024. While this shows investor optimism, the company’s EV division, Model E, is still in the red.

In 2024, Model E reported a $5.1 billion loss and is on track to lose another $5 to $5.5 billion in 2025, translating to around $132,000 lost per EV sold in Q1.

Despite this, Ford offers a dividend yield of 4.44%, providing value to shareholders as the company navigates its EV transformation, something Tesla currently doesn’t offer.

Why Ford Is on ESG Investors’ Radar

Ford’s plan to become carbon neutral by 2050 and its steady progress toward that goal make it a compelling option for climate-conscious investors. With proven manufacturing capacity, strong vehicle branding, and green financing in place, Ford offers a way to participate in the clean transport boom without the risks tied to early-stage startups.

Its path won’t be without bumps, but for investors seeking long-term value in sustainability, Ford remains a stock to watch.

The post Ford’s (F Stock) EV Transformation: A Carbon-Neutral Drive by 2050 Boosts Investor Interest appeared first on Carbon Credits.

Most businesses have a clear picture of what happens inside their own operations. They track energy consumption, manage waste, and monitor the emissions produced on-site. What they often cannot see is everything that happens before a product reaches their facility, and everything that happens after it leaves.

![]()

Carbon Footprint

Texas-Based EnergyX’s Project Lonestar™ Signals a Turning Point for U.S. Lithium Supply

Energy Exploration Technologies, Inc. (EnergyX), led by CEO Teague Egan, has moved the United States closer to building a reliable domestic lithium supply chain. The company recently commissioned its Project Lonestar™ lithium demonstration facility in Texas, marking a key milestone in scaling direct lithium extraction (DLE) technologies.

This development comes at a time when lithium demand is rising sharply due to electric vehicles and energy storage systems. At the same time, the U.S. remains heavily dependent on foreign processing, particularly from China.

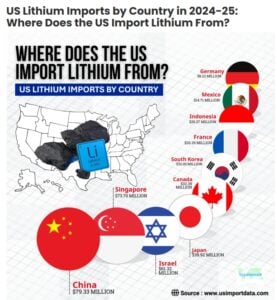

- According to the US import data and Lithium import data of the USA, the total value of US lithium imports reached $432.36 million in 2024, a 9% decline from the previous year.

- The total value of US lithium imports (cells & batteries) accounted for $205.29 million in the first 6 months of 2025.

Against this backdrop, EnergyX’s progress offers both technological validation and strategic value.

From Concept to Reality: How Project Lonestar™ Works

Project Lonestar™ is EnergyX’s first major lithium project in the United States and its second globally. The demonstration plant, located in the Smackover region spanning Texas and Arkansas, is now operational and uses industrial-grade systems rather than small pilot equipment.

- The facility produces around 250 metric tons per year of lithium carbonate equivalent (LCE).

While this output is modest compared to global supply, its importance lies in proving that EnergyX’s proprietary GET-Lit™ technology can efficiently extract lithium from brine. The plant processes locally sourced Smackover brine, a resource that has historically been underutilized despite its lithium potential.

Unlike traditional lithium production, which often relies on hard-rock mining or evaporation ponds, DLE technology directly extracts lithium from brine using advanced filtration and chemical processes. This reduces production time and may lower environmental impact.

- More importantly, the Lonestar™ plant can supply 5 to 25 tons of battery-grade lithium samples to customers.

This allows battery manufacturers to test and validate the material before committing to large-scale supply agreements.

Scaling Up: From Demonstration to Commercial Production

The demonstration plant is only the first phase of a much larger plan. EnergyX aims to scale Project Lonestar™ into a full commercial operation capable of producing 50,000 tonnes of LCE annually across two phases.

- The first phase alone targets 12,500 tonnes per year, which would already place it among the more significant lithium producers in the U.S.

- Significantly, the company has invested approximately $30 million in the demonstration facility, supported in part by a $5 million grant from the U.S. Department of Energy.

- For the full-scale project, EnergyX estimates total capital expenditure at around $1.05 billion.

Cost metrics suggest strong economic potential. The company estimates capital costs at roughly $21,000 per tonne of capacity and operating costs near $3,750 per tonne. If these figures hold at scale, the project could compete effectively with global lithium producers, particularly in a market where cost efficiency is becoming increasingly important.

Teague Egan, Founder & CEO of EnergyX, said,

“Bringing the biggest integrated DLE lithium demonstration plant online in the United States is a foundational milestone for EnergyX and for U.S. domestic lithium production in general. This facility not only validates the performance of our technology on an industrial scale under real-world conditions, but also establishes EnergyX as the lowest cost producer in the U.S. Ultimately this benefits all our customers who need large volumes of lithium for EV and ESS applications, as well as any lithium resource owners looking to implement best-in-class DLE technology whom we are happy to license to.”

Breaking the Bottleneck: Why U.S. Refining Matters

One of the biggest challenges facing the U.S. lithium sector is not resource availability but refining capacity. While lithium deposits exist across the country, most battery-grade lithium chemicals are processed overseas.

China dominates this segment, controlling roughly 70 to 75 percent of global lithium chemical conversion capacity. This concentration creates a structural dependency. Even when lithium is mined in the U.S. or allied countries, it is often shipped abroad for processing before returning as battery materials.

Project Lonestar™ directly addresses this gap. By integrating extraction and refining into a single domestic operation, EnergyX is working to build a complete “brine-to-battery” value chain within the United States. This approach could reduce reliance on foreign processing and improve supply chain resilience.

U.S. Senator Ted Cruz highlighted the project’s importance, noting that domestic lithium production supports both energy security and defense readiness, particularly for applications in advanced battery systems.

- CHECK: LIVE LITHIUM PRICES

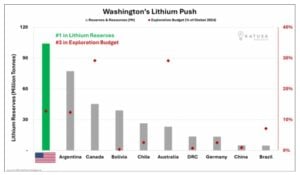

The Current Landscape: Limited Supply, Big Ambitions

Investment is flowing into regions such as Nevada, North Carolina, and Arkansas. If even a portion of these reserves is converted into production, the U.S. could significantly reduce its reliance on imported lithium.

Active Resources and Future Potential

At present, U.S. lithium production remains relatively small. The only active large-scale operation is the Silver Peak Mine in Nevada, which produces between 5,000 and 10,000 tonnes of LCE annually, depending on market conditions.

However, several projects are in development that could significantly expand capacity. The Thacker Pass project, for example, is expected to produce around 40,000 tonnes per year in its first phase once operational later in the decade.

In addition, brine-based developments in the Smackover region aim to produce tens of thousands of tonnes annually, with long-term plans exceeding 100,000 tonnes across multiple sites.

These projects indicate a shift from a niche domestic industry to a more substantial production base. Still, timelines remain uncertain due to regulatory and financial challenges.

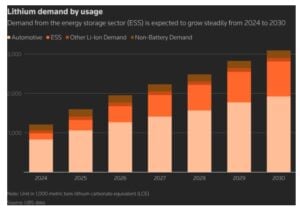

Demand Surge: Batteries Drive the Lithium Boom

The urgency to expand lithium production is driven by rapid growth in battery demand. Electric vehicles, renewable energy storage, and grid modernization are all increasing lithium consumption.

According to S&P Global, U.S. lithium demand is expected to grow at an average rate of 40 percent annually between 2024 and 2029. Canada is projected to see even faster growth, albeit from a smaller base, with demand rising by around 74 percent per year over the same period.

Globally, battery capacity is forecast to approach 4 terawatt-hours by 2030. This expansion highlights lithium’s central role in the clean energy transition. Without sufficient supply, battery production—and by extension, EV adoption—could face constraints.

Why Progress Takes Time

Turning lithium reserves into operational mines and processing facilities is not straightforward. Projects often face long permitting timelines, environmental scrutiny, and legal challenges. Financing can also be difficult, especially in a volatile commodity market.

Local opposition can further complicate development, particularly in areas with high environmental concerns. These factors can delay projects by several years, slowing the pace of expansion.

To address these barriers, the U.S. government is increasing its involvement through funding, policy support, and efforts to streamline permitting. The Department of Energy’s backing of EnergyX reflects a broader strategy to accelerate domestic critical mineral development.

Conclusion: A Strategic Shift in Motion

Project Lonestar™ represents a meaningful step toward reshaping the U.S. lithium landscape. By proving the viability of direct lithium extraction at an industrial scale, EnergyX has laid the groundwork for larger, commercially viable operations.

The project also aligns with national priorities around energy security, supply chain resilience, and clean energy transition. While challenges remain, the combination of technological innovation, government support, and rising demand creates a strong foundation for growth.

As the world moves toward electrification, lithium will remain at the center of the transition. Projects like Lonestar™ show that the United States is beginning to close the gap between resource potential and real-world production—one facility at a time.

The post Texas-Based EnergyX’s Project Lonestar™ Signals a Turning Point for U.S. Lithium Supply appeared first on Carbon Credits.

Analysis: How ‘plug-in solar’ can save UK homes £1,100 on energy bills

Georgia’s New Public Service Commissioner Says She Will Put Affordability and Transparency First

What Nature Based Solutions Actually Mean for Corporate Climate Strategy

-

Climate Change8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases8 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Renewable Energy5 months ago

Renewable Energy5 months agoSending Progressive Philanthropist George Soros to Prison?

-

Carbon Footprint2 years ago

Carbon Footprint2 years agoUS SEC’s Climate Disclosure Rules Spur Renewed Interest in Carbon Credits