Amazon, alongside Meta, Netflix, Mastercard, PepsiCo, and others, are leading a shift in carbon credits by backing the early retirement of coal-fired power plants. They’ve joined the Kinetic Coalition, a global alliance of more than 20 major companies working to unlock investment in clean energy in emerging economies. This marks a big step in climate action—paying to close coal plants early instead of funding tree-planting or technology offsets.

What Are Early Retirement or “Transition” Credits?

Transition credits differ from traditional carbon credits. Transition credits pay plant owners to close coal units early. This approach differs from funding for projects like forests or renewable energy after emissions have occurred. Instead, it avoids future emissions and makes room for clean power.

Closing a coal plant early can cost hundreds of millions of dollars. For instance, research showed that winding down a 1-GW plant five years early would need about $310 million. Transition credits are a helpful financial tool. They cover closure costs, support displaced workers, and help build new clean energy projects.

This concept has already started in Southeast Asia. And Verra, a key player in carbon markets, has launched a method to certify early coal retirements. This method sets high standards for clean energy replacements and supports local jobs.

One pilot in the Philippines aims to close a coal plant a decade early—avoiding up to 19 million tonnes of CO₂. The new step is scaling this model with corporate backing, as what the Kinetic Coalition does.

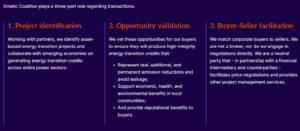

Amazon is part of the Kinetic Coalition, a buyers’ alliance organized by the Center for Climate and Energy Solutions (C2ES). The Coalition connects major buyers with coal-closure projects in emerging economies. Other major companies in the alliance include PepsiCo, McDonald’s, Meta, Nike, Salesforce, and Morgan Stanley.

Nat Keohane, President of C2ES, noted:

“Energy transition credits can accelerate the transition to clean energy systems for emerging economies, help companies reduce their supply chain emissions – and, most importantly, bring economic, health, and environmental gains to local communities. They offer an opportunity to achieve emission reductions at scale while benefiting companies and people – and Kinetic is excited to seize it.”

The Coalition wants to purchase reliable transition credits. These credits will help with early plant retirements, renewables, grid upgrades, and support local communities. It already explores pilots in the Dominican Republic, Chile, and the Philippines.

In the Philippines, where coal still powers close to 60% of the grid, the coalition plans to support the early retirement of a major coal-fired plant. The goal is to replace it with a mix of clean energy and storage, ensuring no gap in supply.

In Chile and the Dominican Republic, the projects aim to modernize electricity grids, not just shut down coal. These efforts seek to add more renewables, cut reliance on fossil fuels, and boost reliability for consumers.

The credits created from these projects may serve multiple purposes. For example, Schneider Electric, one of the coalition’s participants, is exploring several options. It may use the credits to offset its own emissions or sell them to clients through its sustainability consulting arm, EcoAct. This shows how credits can fit into both corporate climate plans and broader client services.

By pooling demand, the Kinetic Coalition can support large-scale impact. Members commit capital upfront—helping governments and power companies plan and fund the shift away from coal. The alliance could channel billions of dollars by 2035, driven by strong corporate climate goals.

Tackling Coal Power: Pathways to Clean Energy in Emerging Markets

Coal-fired power remains a major obstacle for climate progress, with emissions rising by 0.9% (135 Mt CO₂) in 2024 and coal making up about 36% of global electricity in 2023. Many emerging economies still rely on coal to meet growing energy demands.

Initiatives like the Kinetic Coalition aim to close coal plants early, replacing them with clean energy while supporting jobs and communities. BloombergNEF estimates that over $2.6 trillion in clean energy investment is needed in emerging markets by 2050, and innovative tools like transition credits can help unlock this vital capital.

The early pilots may shape how we manage energy transitions. They can also guide the responsible and fair use of carbon credits at scale.

The group is ensuring credibility by aligning with top standards like ICVCM and CORSIA. They are also working with the Advanced and Indirect Mitigation Platform. Projects can use Verra’s 2024 early coal retirement method. They may also follow new guidelines from the Gold Standard and the Environmental Resources Trust.

The Corporate Trailblazers

Amazon, Meta, Netflix, and Mastercard have been major buyers of voluntary carbon credits for years. Their shift to transition credits shows a new path. They now focus on real-world emissions reductions instead of offsets, such as forest protection.

They are also part of the Energy Transition Accelerator (ETA). This initiative was launched by the U.S. State Department, Bezos Earth Fund, and Rockefeller Foundation. Amazon, Mastercard, Meta, McDonald’s, PepsiCo, and others endorsed its approach at Climate Week 2024. The ETA wants to boost low-carbon energy in developing markets. It does this by using high-quality credits and fair transition plans.

If transition credits gain a firm foothold, they could channel hundreds of billions into clean energy systems. Estimates suggest the Kinetic Coalition alone could mobilize $72–207 billion by 2035.

Trends and Forecasts: How Billions Could Shift the Energy Mix

The carbon credit market is growing fast. The voluntary market reached around $2 billion in 2024 and may grow to $24 billion by 2030—around 35% annual growth. Add in compliance systems, and the total market neared $115 billion in 2024, growing at ~16% annually.

Transition credits are a newer segment, but momentum is building with these trends:

Regulatory support. Singapore is drafting rules for high-integrity carbon credits. Japan is building a carbon market framework. South Korea and China are also exploring credit systems.

Verra’s methodology. Its VM0052 method for coal-plant retirement was a major milestone. It sets strong guardrails for environmental impact and community protection.

Tech for confidence. Blockchain, satellite tracking, and AI are helping verify, trace, and audit credits—reducing fraud.

Investor demand. Net-zero commitments from thousands of companies mean growing demand for real-impact credits.

Public-private action. Groups like ETA, Kinetic Coalition, and CCCI demonstrate cross-sector momentum to scale these solutions.

By investing in transition credits, Amazon and other Kinetic Coalition partners are helping forge a new climate finance path. Instead of offsetting emissions, they are funding early closure of coal plants—cutting future carbon emissions before they happen.

With robust standards, growing tech tools, and strong corporate demand, transition credits could become a major asset in achieving global climate goals—while supporting clean energy in emerging economies.

“…Human subtlety… will never devise an invention more beautiful, more simple or more direct than does nature, because in her inventions nothing is lacking, and nothing is superfluous…”

Corporate climate strategy has decisively shifted from a specialized sustainability function to a central pillar of enterprise risk management. Today, boards of directors and executive teams face intensifying pressure from investors, regulators, and customers to deliver defensible, science-aligned decarbonization plans. In this environment, vague sustainability marketing and weak carbon claims are no longer just ineffective—they are significant reputational and compliance liabilities.

As you evaluate pathways to net zero, Nature Based Solutions are frequently presented as a crucial mechanism. But for executive decision-makers, navigating the noise around these solutions requires a clear, commercially grounded understanding of what they actually mean, how they mitigate risk, and how they fit into a rigorous corporate climate strategy.

Beyond the Hype: Defining Nature Based Solutions

The term “Nature Based Solutions” is often misused as a catch-all phrase for any environmental project, leading to justified skepticism among risk-aware leaders. According to the globally recognized framework established by the UN Environment Assembly and the International Union for Conservation of Nature (IUCN), true Nature Based Solutions are strictly defined. They are actions to protect, sustainably manage, and restore natural and modified ecosystems in ways that effectively address societal challenges, simultaneously providing human well-being and biodiversity benefits.

When properly designed, these solutions are a powerhouse for climate mitigation. Research indicates that agriculture, forestry, wetlands, and bioenergy could feasibly contribute about 30% of the global mitigation needed to limit warming to 1.5°C by 2050, and up to 37% of the emissions mitigation needed by 2030.

However, the commercial reality is that not all nature-focused projects meet this high standard. Poorly executed initiatives, such as planting monoculture non-native forests solely for rapid carbon sequestration, can actually increase a region’s exposure to hazards like wildfires, exacerbate biodiversity loss, and alienate local communities. For your organization, investing in low-quality projects translates directly into stranded assets and accusations of greenwashing. High-integrity Nature Based Solutions require a holistic approach that balances carbon sequestration with ecological stability, inclusive governance, and strict safeguards.

The Commercial Case: Risk Management and Enterprise Value

For CEOs, CFOs, and supply chain leaders, the value of Nature Based Solutions extends far beyond greenhouse gas accounting. These interventions serve as highly effective tools for managing acute and chronic business risks driven by climate change.

Consider physical risk and supply chain resilience. Companies highly dependent on natural capital can utilize Nature Based Solutions to secure their operations against environmental shocks. For example, a food and beverage company might invest in restoring degraded landscapes ecologically linked to its agricultural sourcing, thereby mitigating the risk of supply disruptions and price volatility caused by shifting precipitation and extreme weather. Similarly, restoring coastal ecosystems like mangroves can provide billions of dollars globally in avoided losses from coastal flooding, directly protecting adjacent manufacturing facilities and infrastructure.

Beyond physical risk, these solutions protect long-term enterprise value by addressing shifting market expectations. Demonstrating a tangible commitment to the climate and nature crises helps secure your organization’s social license to operate, avoiding costs linked to stakeholder backlash. It also serves as a powerful differentiator in talent acquisition and retention, particularly among younger demographics who increasingly prioritize corporate purpose when choosing employers.

Furthermore, financial markets are rapidly integrating nature-related risks into their capital allocation models. Integrating Nature Based Solutions into your transition planning signals to investors that you are proactively managing systemic risks and positioning your firm favorably within a nature-positive global economy. The Taskforce on Nature-related Financial Disclosures (TNFD) provides a structured LEAP approach—Locate, Evaluate, Assess, and Prepare—enabling businesses to rigorously quantify how ecosystem degradation threatens future cash flows and where strategic interventions can mitigate these financial risks.

Integrating Nature into a Defensible Net Zero Plan

Understanding the strategic value of Nature Based Solutions is only the first step. The critical challenge is integrating them into a credible corporate climate strategy without exposing your brand to claims of offsetting out of convenience.

Leading frameworks, including the Science Based Targets initiative (SBTi), establish a clear mitigation hierarchy: your primary imperative must be deep, rapid decarbonization within your own value chain. You cannot simply buy your way out of your direct emissions footprint. However, the science is equally clear that solving the climate crisis requires both internal abatement and external investment.

This is where the deployment strategy diverges based on your business model:

Insetting for Land-Intensive Sectors: If your company operates within the Forest, Land and Agriculture (FLAG) sector, you can deploy Nature Based Solutions directly within your own supply chain. This practice, known as “insetting,” involves working with suppliers to implement regenerative agriculture, agroforestry, or conservation practices that actively reduce your Scope 3 emissions while increasing the resilience of your raw materials.

Beyond Value Chain Mitigation (BVCM): For companies outside the FLAG sector, or for investments made above and beyond internal targets, Nature Based Solutions fall under Beyond Value Chain Mitigation. The SBTi emphasizes that the private sector must engage in BVCM to avert devastating climate impacts. By channeling finance into high-impact jurisdictional forest protection or wetland restoration, you help protect irrecoverable carbon sinks and scale up the carbon dioxide removal technologies needed to neutralize global residual emissions by 2050.

Navigating Carbon Markets with High Integrity

For organizations looking to execute these strategies, the voluntary carbon market offers a mechanism to finance Nature Based Solutions globally. Yet, the market’s historical lack of transparency has made many compliance leaders and Corporate Affairs teams hesitant to engage.

To safely utilize carbon credits, your organization must adopt a stringent, data-driven approach centered on high integrity. The Integrity Council for the Voluntary Carbon Market (ICVCM) has established the Core Carbon Principles (CCPs), setting a global benchmark to ensure credits create real, verifiable climate impact. High-quality carbon credits must be strictly additional—meaning the mitigation would not have occurred without the carbon finance—and they must ensure permanence while preventing emissions leakage to other areas.

On the demand side, how you communicate your investments matters just as much as the investments themselves. The Voluntary Carbon Markets Integrity Initiative (VCMI) Claims Code of Practice outlines clear rules for how companies can make credible claims about their use of carbon credits. Under these rules, Carbon Integrity Claims (Silver, Gold, or Platinum) are reserved for companies that maintain transparent emissions inventories, set science-aligned near-term reduction targets, and use high-quality credits to go above and beyond their internal decarbonization trajectory.

Following these guidelines ensures that your claims are transparent, traceable, true, and verifiable. It fundamentally separates your brand from competitors relying on weak “carbon neutral” marketing, transforming your climate strategy into a defensible demonstration of environmental leadership.

The Path Forward

Navigating the intersection of net-zero planning, climate finance, and environmental markets is undeniably complex. Distinguishing between a high-impact Nature Based Solution and a high-risk carbon project requires deep technical evaluation of greenhouse gas accounting methodologies, biodiversity co-benefits, and regulatory governance.

However, the risks of inaction—or poorly guided action—far outweigh the challenges of implementation. Nature Based Solutions offer a scientifically rigorous, commercially viable pathway to manage climate risk, secure supply chains, and prepare your organization for the impending wave of climate and nature disclosures.

At Carbon Credit Capital, we help organizations understand, evaluate, and confidently integrate high-integrity carbon credits and Nature Based Solutions into defensible net-zero strategies. We bring the domain expertise required to mitigate reputational risk, clarify complex market developments, and ensure your climate investments deliver measurable value to both the planet and your enterprise.

Schedule a consultation with carboncreditcapital.com today to learn how we can help you build a resilient, high-integrity corporate climate strategy.

Most businesses have a clear picture of what happens inside their own operations. They track energy consumption, manage waste, and monitor the emissions produced on-site. What they often cannot see is everything that happens before a product reaches their facility, and everything that happens after it leaves.

Energy Exploration Technologies, Inc. (EnergyX), led by CEO Teague Egan, has moved the United States closer to building a reliable domestic lithium supply chain. The company recently commissioned its Project Lonestar™ lithium demonstration facility in Texas, marking a key milestone in scaling direct lithium extraction (DLE) technologies.

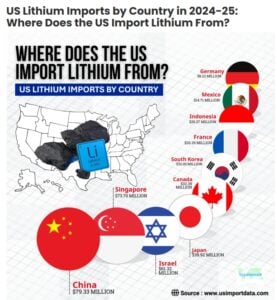

This development comes at a time when lithium demand is rising sharply due to electric vehicles and energy storage systems. At the same time, the U.S. remains heavily dependent on foreign processing, particularly from China.

The total value of US lithium imports (cells & batteries) accounted for $205.29 million in the first 6 months of 2025.

Against this backdrop, EnergyX’s progress offers both technological validation and strategic value.

From Concept to Reality: How Project Lonestar™ Works

Project Lonestar™ is EnergyX’s first major lithium project in the United States and its second globally. The demonstration plant, located in the Smackover region spanning Texas and Arkansas, is now operational and uses industrial-grade systems rather than small pilot equipment.

The facility produces around 250 metric tons per year of lithium carbonate equivalent (LCE).

While this output is modest compared to global supply, its importance lies in proving that EnergyX’s proprietary GET-Lit™ technology can efficiently extract lithium from brine. The plant processes locally sourced Smackover brine, a resource that has historically been underutilized despite its lithium potential.

Source: EnergyX

Unlike traditional lithium production, which often relies on hard-rock mining or evaporation ponds, DLE technology directly extracts lithium from brine using advanced filtration and chemical processes. This reduces production time and may lower environmental impact.

More importantly, the Lonestar™ plant can supply 5 to 25 tons of battery-grade lithium samples to customers.

This allows battery manufacturers to test and validate the material before committing to large-scale supply agreements.

Source: EnergyX

Scaling Up: From Demonstration to Commercial Production

The demonstration plant is only the first phase of a much larger plan. EnergyX aims to scale Project Lonestar™ into a full commercial operation capable of producing 50,000 tonnes of LCE annually across two phases.

The first phase alone targets 12,500 tonnes per year, which would already place it among the more significant lithium producers in the U.S.

Significantly, the company has invested approximately $30 million in the demonstration facility, supported in part by a $5 million grant from the U.S. Department of Energy.

For the full-scale project, EnergyX estimates total capital expenditure at around $1.05 billion.

Cost metrics suggest strong economic potential. The company estimates capital costs at roughly $21,000 per tonne of capacity and operating costs near $3,750 per tonne. If these figures hold at scale, the project could compete effectively with global lithium producers, particularly in a market where cost efficiency is becoming increasingly important.

Teague Egan, Founder & CEO of EnergyX, said,

“Bringing the biggest integrated DLE lithium demonstration plant online in the United States is a foundational milestone for EnergyX and for U.S. domestic lithium production in general. This facility not only validates the performance of our technology on an industrial scale under real-world conditions, but also establishes EnergyX as the lowest cost producer in the U.S. Ultimately this benefits all our customers who need large volumes of lithium for EV and ESS applications, as well as any lithium resource owners looking to implement best-in-class DLE technology whom we are happy to license to.”

Breaking the Bottleneck: Why U.S. Refining Matters

One of the biggest challenges facing the U.S. lithium sector is not resource availability but refining capacity. While lithium deposits exist across the country, most battery-grade lithium chemicals are processed overseas.

China dominates this segment, controlling roughly 70 to 75 percent of global lithium chemical conversion capacity. This concentration creates a structural dependency. Even when lithium is mined in the U.S. or allied countries, it is often shipped abroad for processing before returning as battery materials.

Project Lonestar™ directly addresses this gap. By integrating extraction and refining into a single domestic operation, EnergyX is working to build a complete “brine-to-battery” value chain within the United States. This approach could reduce reliance on foreign processing and improve supply chain resilience.

U.S. Senator Ted Cruz highlighted the project’s importance, noting that domestic lithium production supports both energy security and defense readiness, particularly for applications in advanced battery systems.

The Current Landscape: Limited Supply, Big Ambitions

How Much Lithium Does the U.S. Have?

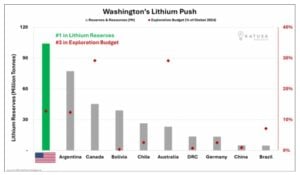

The United States has a strong lithium resource base, but it still struggles to produce it at scale. Data from the United States Geological Survey shows that the country held about 14 million tonnes of lithium reserves in 2023, ranking it third globally.

Despite this, U.S. production remains very low. The country produced only 615 metric tonnes of lithium in 2023, according to USGS. This is tiny compared to global leaders. Australia produced around 86,000 tonnes, while Chile reached about 56,530 tonnes in the same year.

Lithium Reserves by Country 2026

Source: World Population Review

In simple terms, the U.S. has plenty of lithium underground. But it still needs time, investment, and better infrastructure to turn those resources into a real supply.

Investment is flowing into regions such as Nevada, North Carolina, and Arkansas. If even a portion of these reserves is converted into production, the U.S. could significantly reduce its reliance on imported lithium.

Active Resources and Future Potential

At present, U.S. lithium production remains relatively small. The only active large-scale operation is the Silver Peak Mine in Nevada, which produces between 5,000 and 10,000 tonnes of LCE annually, depending on market conditions.

However, several projects are in development that could significantly expand capacity. The Thacker Pass project, for example, is expected to produce around 40,000 tonnes per year in its first phase once operational later in the decade.

In addition, brine-based developments in the Smackover region aim to produce tens of thousands of tonnes annually, with long-term plans exceeding 100,000 tonnes across multiple sites.

These projects indicate a shift from a niche domestic industry to a more substantial production base. Still, timelines remain uncertain due to regulatory and financial challenges.

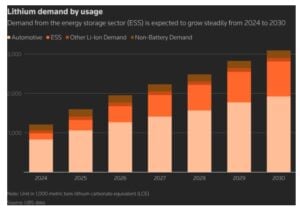

Demand Surge: Batteries Drive the Lithium Boom

The urgency to expand lithium production is driven by rapid growth in battery demand. Electric vehicles, renewable energy storage, and grid modernization are all increasing lithium consumption.

According to S&P Global, U.S. lithium demand is expected to grow at an average rate of 40 percent annually between 2024 and 2029. Canada is projected to see even faster growth, albeit from a smaller base, with demand rising by around 74 percent per year over the same period.

Globally, battery capacity is forecast to approach 4 terawatt-hours by 2030. This expansion highlights lithium’s central role in the clean energy transition. Without sufficient supply, battery production—and by extension, EV adoption—could face constraints.

Why Progress Takes Time

Turning lithium reserves into operational mines and processing facilities is not straightforward. Projects often face long permitting timelines, environmental scrutiny, and legal challenges. Financing can also be difficult, especially in a volatile commodity market.

Local opposition can further complicate development, particularly in areas with high environmental concerns. These factors can delay projects by several years, slowing the pace of expansion.

To address these barriers, the U.S. government is increasing its involvement through funding, policy support, and efforts to streamline permitting. The Department of Energy’s backing of EnergyX reflects a broader strategy to accelerate domestic critical mineral development.

Conclusion: A Strategic Shift in Motion

Project Lonestar™ represents a meaningful step toward reshaping the U.S. lithium landscape. By proving the viability of direct lithium extraction at an industrial scale, EnergyX has laid the groundwork for larger, commercially viable operations.

The project also aligns with national priorities around energy security, supply chain resilience, and clean energy transition. While challenges remain, the combination of technological innovation, government support, and rising demand creates a strong foundation for growth.

As the world moves toward electrification, lithium will remain at the center of the transition. Projects like Lonestar™ show that the United States is beginning to close the gap between resource potential and real-world production—one facility at a time.