Carbon Footprint

U.S. Residential Solar in 2025: Market Slowdown Now, but 2050 Forecast is Massive

The U.S. residential solar market is uncertain. Its long-term potential is huge, exceeding current U.S. power generation capacity. However, recent policy changes threaten short-term growth.

Wood Mackenzie’s analysis, “Near-term challenges but long-term potential: evaluating the US residential solar addressable market,” shows how the One Big Beautiful Bill Act (OBBBA) affects homeowners and solar developers. The main concern is the removal of the Section 25D Investment Tax Credit (ITC) for customer-owned systems starting in 2026.

The U.S. Residential Solar Stumbles in Tough Climate

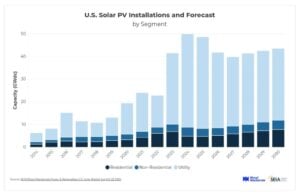

According to the SEIA Q2 solar report, residential solar installations fell sharply in Q1 2025. Homeowners installed 1,106 MWdc of capacity. This is a 13% drop from Q1 2024 and 4% lower than Q4 2024.

High interest rates, economic uncertainty, and upcoming changes to federal tax credits are slowing demand. California remains the top solar state with 255 MWdc installed, but this is its weakest performance since Q3 2020.

More than 20 states saw installation declines. Puerto Rico and Florida follow California, but nationwide momentum has stalled.

OBBBA Shakes Up an Already Fragile Solar Policy

The OBBBA introduces significant policy uncertainty. The removal of the Section 25D credit has made solar less affordable for homeowners. While third-party-owned (TPO) systems can still qualify for credits under Section 48, they now face new restrictions like compliance with “foreign entity of concern” (FEOC) rules.

An executive order issued on July 7 adds to the confusion and may limit TPO system eligibility for incentives.

Additionally, the House passed a budget reconciliation bill on May 22. This bill could eliminate tax credits for both customer-owned and leased solar systems starting in 2026. Though it passed narrowly, it faces Senate negotiations, where amendments could change its impact.

Sunny Horizon Yet Cloudy Now

Due to rising policy and economic challenges, the five-year outlook for residential solar has been cut by 9%. Installers report significant disruption, and consumer demand is softening amid uncertainty around tariffs and future tax incentives.

Despite these challenges, the market’s potential is enormous. By the end of 2024, only 7.5% of suitable U.S. homes had solar installed. Wood Mackenzie forecasts that, barring setbacks, the residential solar segment could grow 9% annually through 2030 and reach a 13% penetration rate.

However, these figures do not account for OBBBA’s full impacts. In a worst-case scenario, assuming the loss of all tax credits and high interest rates, adoption could drop 46% below baseline projections by 2030.

- READ MORE: US Solar Market Slows in 2025 – Here’s How SolarBank (NASDAQ: SUUN) Is Still Gaining Ground

Can the Solar Market Recover Without Tax Credits?

Looking ahead, the key question is how solar companies will adapt without the Section 25D ITC. Many smaller players may not survive the transition, especially if TPO options become less viable.

Industry veterans expect surviving companies to change. Homeowners might find solar appealing due to lower system costs, new financing options, and rising electricity bills. Concerns about resilience and energy independence may also increase adoption.

Even in the most pessimistic forecast, the U.S. residential solar market is expected to rebound after 2028 and add at least 150 GWdc by 2050.

Looking Ahead to 2050: Residential Solar’s Next Frontier

The solar industry’s long-term outlook is promising. With electricity demand expected to rise and the push for energy independence growing, solar remains a top solution for decarbonizing the residential sector.

By 2050, solar will play a vital role in how Americans power their homes. While only 7.5% of suitable homes had solar by the end of 2024, that number could increase significantly if conditions align.

Key growth drivers toward 2050 include:

-

Retail electricity rate hikes: Rising utility rates may lead more homeowners to adopt solar.

-

Battery storage adoption: Pairing solar energy with affordable home batteries can help solve intermittency issues and unlock significant savings.

-

State policy momentum: Even if federal support wanes, state-level incentives and renewable mandates could keep driving adoption.

-

Technological advances: More efficient panels, easier installations, and longer warranties will boost solar’s appeal.

Business Models Will Evolve

If traditional customer-owned systems lose their tax advantages, solar companies may pivot to new business models. Community solar, subscription-based plans, and solar-as-a-service may gain traction. These models allow broader participation, especially among renters and low-income households.

Digital platforms that streamline financing, permitting, and installation could cut costs, making solar feasible even without generous tax credits.

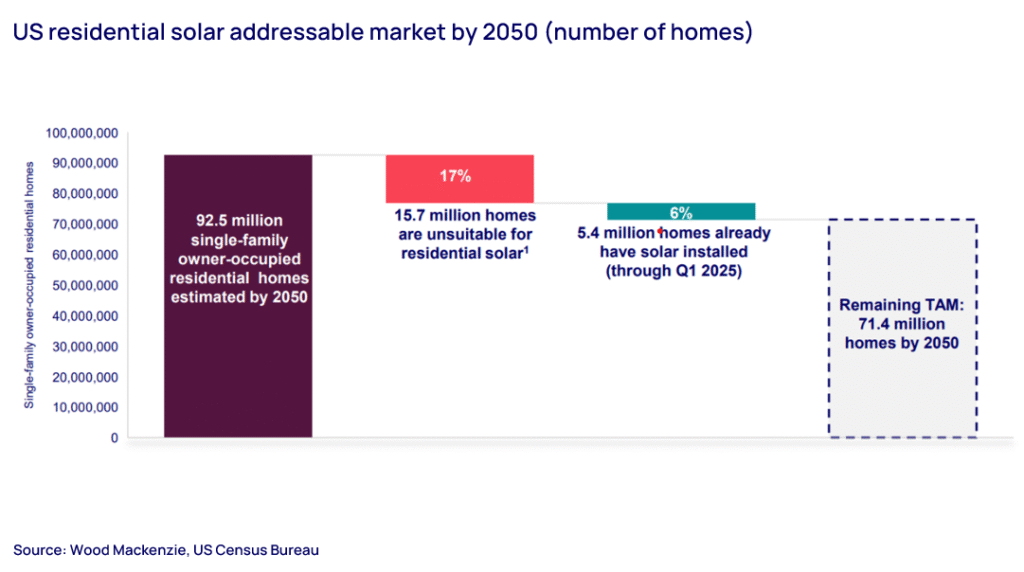

1,494 GWdc: A Market Bigger Than the Grid

Despite current challenges, the long-term market size is impressive. Wood Mac says, by 2050, there will be about 92 million owner-occupied single-family homes in the U.S. Excluding homes with solar already and those not suitable for installation, around 70 million homes could still get solar upgrades.

If average system sizes continue to increase, this leads to a total addressable market (TAM) of roughly 1,494 GWdc, exceeding the current U.S. electricity generation fleet of around 1,300 GW.

Will Solar Reach Its Full Potential?

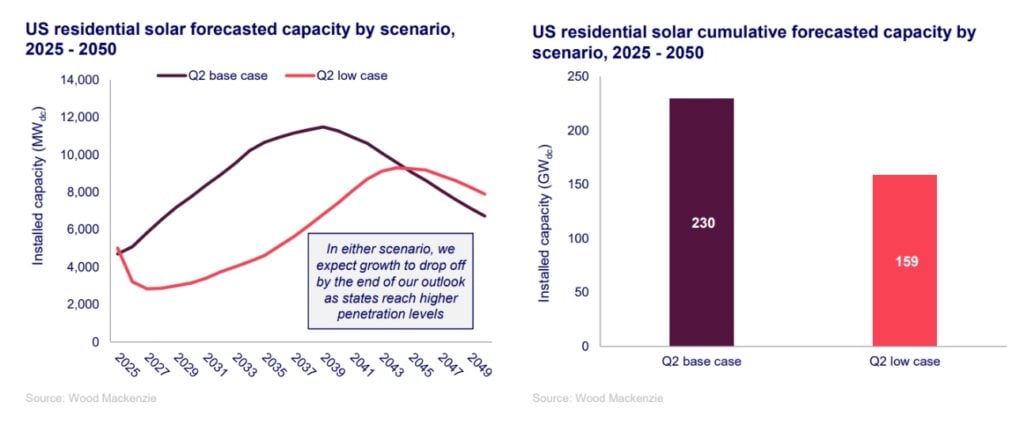

Wood Mackenzie’s “low case” scenario suggests only 12% of the total addressable market may be reached by 2050. However, this might be too cautious. Over the next 25 years, innovation, lower costs, and new business models could greatly increase market penetration.

Under favorable conditions, the market might reach a penetration of 30–40%. If the average system size grows as expected and costs drop below grid parity, growth could speed up.

In summary, the 1,494 GWdc TAM won’t be fully captured, but even partial adoption could add hundreds of gigawatts of clean capacity.

Overall, the long-term picture is compelling. With a TAM that exceeds the U.S. power generation fleet, the opportunity is immense. Even modest adoption could reshape the residential energy landscape by 2050.

The next few years will test the resilience and agility of solar companies. Those that survive will likely power a cleaner, more self-sufficient future for millions of American homes.

The post U.S. Residential Solar in 2025: Market Slowdown Now, but 2050 Forecast is Massive appeared first on Carbon Credits.