Carbon Footprint

U.S. Biofuel Market 2026: Can EPA Policies Offset War-Driven Volatility?

The U.S. biofuel industry stepped into 2026 with strong policy backing and rising demand. However, global events quickly changed the tone. A sharp escalation in the US–Israel–Iran conflict in late February sent shockwaves through energy markets. Oil prices jumped, supply chains tightened, and uncertainty spread across fuel markets.

At the same time, the U.S. Environmental Protection Agency (EPA) introduced its most ambitious biofuel policy yet under the Renewable Fuel Standard (RFS). This created a powerful but complicated mix—long-term policy certainty collided with short-term geopolitical chaos.

As a result, the U.S. biofuel sector now faces a defining moment. Growth looks strong on paper, but rising costs and market volatility are testing how sustainable that growth really is.

EPA Administrator Lee Zeldin said:

“President Trump promised a Golden Age of American agriculture. Once again, his administration is delivering. Overall, ‘Set 2’ creates a larger, more stable, and more reliable domestic market for U.S. crops, strengthening farm income and rural economies.

For 20 years, this program has diversified our nation’s energy supply and advanced American energy independence. EPA is proud to deliver on this mission and to do so at historic levels.”

EPA’s RFS ‘Set 2’ Rule Changes the Game

Amid this volatility, U.S. policy took a decisive turn. On March 26, 2026, the EPA finalized the Renewable Fuel Standard (RFS) “Set 2” rule, setting new blending targets for 2026 and 2027.

- The new requirements are the highest in the program’s history. The EPA set total renewable volume obligations at 26.81 billion RINs for 2026 and 27.02 billion RINs for 2027.

These targets reflect a major increase compared to previous years and signal a strong push toward domestic biofuel production.

- The policy focuses heavily on expanding the use of biomass-based diesel, including biodiesel and renewable diesel. This includes a 70 percent reallocation of small refinery exemptions granted for 2023–2025

- At the same time, ethanol blending levels remain stable at 15 billion gallons annually, providing consistency for corn producers.

Additionally, the rule puts back 70% of the biofuel volumes that small refineries didn’t have to blend from 2023 to 2025. This effectively increases the burden on refiners while ensuring that biofuel demand remains strong.

Policy Pivot Favors U.S. Biofuel Producers

Beyond volume targets, the EPA introduced structural changes. The agency removed renewable electricity from the RFS program, narrowing its focus to liquid and gaseous fuels. It also introduced measures to limit the role of foreign feedstocks in the future.

Starting in 2028, imported biofuels will receive a lower compliance value compared to domestic products. In addition, incentives such as the 45Z tax credit are designed to favor U.S.-based production.

The broader goal is clear. The policy aims to strengthen energy independence, support farmers, and reduce reliance on foreign oil. Estimates suggest that these measures could cut oil imports by hundreds of thousands of barrels per day over the next two years.

At the same time, the EPA expects significant economic benefits. The rule could generate billions of dollars for rural economies and create thousands of new jobs across agriculture and manufacturing sectors.

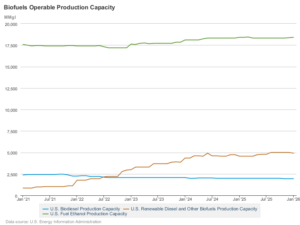

The U.S. Energy Information Administration (EIA) recently published updated data on the country’s biofuel production capacity, shown below.

Demand Surges but Supply Faces Pressure

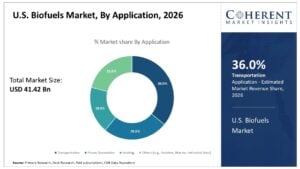

While policy is driving demand higher, supply conditions remain tight. The U.S. biofuel market is projected to exceed $41 billion in 2026, supported by transportation demand and decarbonization goals.

Ethanol continues to dominate the market, especially through E10 fuel blends. However, advanced biofuels such as renewable diesel and SAF are growing faster due to stronger policy incentives and rising interest in low-carbon fuels.

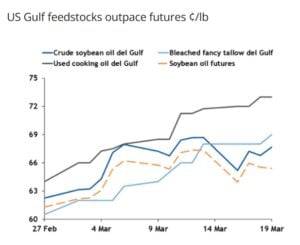

Despite this growth, feedstock availability is becoming a major concern. Domestic sources such as soybean oil, used cooking oil, and tallow are under pressure. Prices have risen sharply due to limited supply and increased competition from both the fuel and food industries.

At the same time, import restrictions have reduced access to cheaper global feedstocks. Tariffs and lower compliance values for foreign inputs are shifting the market toward domestic sourcing. While this supports local producers, it also reduces flexibility during supply shortages.

New processing capacity is helping to ease some of the pressure. Agribusiness companies are expanding oilseed crushing operations, and renewable diesel plants are increasing output. However, these efforts may take time to fully balance supply and demand.

War-Driven Oil Shock Makes Biofuels More Valuable

The U.S. biofuel market is gaining momentum as rising oil prices and global conflict reshape energy choices. The ongoing U.S.-Israel-Iran war has disrupted key oil infrastructure and shipping lanes near the Strait of Hormuz, sending crude prices sharply higher.

As conventional fuels become more expensive, alternatives like ethanol, renewable diesel, and sustainable aviation fuel (SAF) are increasingly attractive, driving demand across the sector. This surge has pushed feedstock costs to multi-year highs, with soybean oil, used cooking oil, and animal fats climbing steadily.

At the same time, renewable fuel credits, or RINs, have reached levels not seen in years, boosting margins for biofuel producers but raising compliance costs for refiners. Reports from Argus Media show that U.S. renewable diesel feedstocks hit their highest prices in over two years this month, highlighting the market’s sensitivity to war-driven disruptions.

While industry groups argue that strong domestic production stabilizes supply and reduces reliance on imported oil, refiners warn that these rising costs could eventually reach consumers, especially in regions with less competition. The combination of strong demand, tight supply, and geopolitical risk is redefining U.S. biofuel market dynamics.

Opportunities for Farmers, Challenges for Refiners

The current landscape is creating both opportunities and challenges.

Biofuel producers and farmers are seeing strong benefits. Higher demand for crops like corn and soybeans is supporting agricultural incomes. Investment in renewable fuel projects is also increasing, driven by policy certainty and market growth.

However, refiners and fuel distributors are facing tighter margins. The cost of compliance, combined with volatile feedstock prices, is making operations more difficult. Smaller players may struggle to compete in this environment.

Consumers could also feel the impact through higher fuel prices, especially if cost pressures continue. To manage these risks, many companies are turning to hedging strategies. Storage, long-term contracts, and flexible sourcing are becoming essential tools in navigating market uncertainty.

Supporting this announcement, U.S. Secretary of Agriculture Brooke L. Rollins, said:

“Today’s announcement is truly historic for our nation’s farmers and energy producers. These numbers represent the highest levels of biofuels ever required to be blended into our fuel supply. With President Trump and Administrator Zeldin’s leadership, these historically high volumes are expected to create a $3 to $4 billion dollar increase in net farm income. The Renewable Fuel Standard Set 2 Rule will create a $31 billion dollar value for American corn and soybean oil for biofuel production in 2026, which is $2 billion more than in 2025. Our farmers are stepping up to grow American energy dominance.”

Strong Growth, But Uncertain Path

Looking ahead, the U.S. biofuel market is expected to grow steadily, with projections showing annual growth of up to 10% through the next decade. Strong EPA mandates and supportive policies will continue to drive demand.

However, the path forward is far from stable.

The mismatch between long-term policy goals and short-term geopolitical disruptions will remain a key challenge. Events like the ongoing Middle East conflict can quickly shift market dynamics, creating sudden price swings and supply risks.

The rest of 2026 will depend on several key factors, including potential EPA waivers, movements in RIN markets, and developments in global energy supply. In the end, the success of U.S. biofuels will depend on balance. Policy support provides a strong foundation, but flexibility will be critical in managing real-world challenges.

Despite the industry growing fast, the question remains—can it handle the pressure of both policy ambition and global uncertainty at the same time?

The post U.S. Biofuel Market 2026: Can EPA Policies Offset War-Driven Volatility? appeared first on Carbon Credits.