Nigeria is planning a large clean cooking program that aims to distribute 80 million efficient cookstoves to households. Project backers say the rollout could help reduce smoke from cooking, cut pressure on forests, and create a new stream of carbon credits.

Recent reporting in Nigeria says the project is also tied to a revenue target. A senior finance executive at project developer GreenPlinth Africa said the Federal Government could earn up to $5 billion each year from “verified carbon credit revenues” when the program reaches full scale.

Lagos State has also described itself as an early “anchor” for the program. Lagos State Government announced it will lead the way in providing 6 million free cookstoves. Distribution in the state has started in June 2025, beginning in Makoko.

Mr. Tunde Lemo, former Deputy Governor of the Central Bank of Nigeria, commented:

“This is not a pilot. It is not a promise. It is a nationally endorsed, structured, and scalable intervention…This is one of the most ambitious clean cooking and household energy transition programmes ever undertaken globally.”

An 80 Million Stove Rollout With National Ambitions

Lagos State’s climate office describes the initiative as a nationwide effort to deploy 80 million efficient cookstoves free of charge. It says the goal is to sharply reduce traditional firewood use for women and low-income households.

Large stove programs usually try to replace or improve traditional cooking methods that produce heavy smoke indoors. In many households, cooking uses wood, charcoal, or other solid fuels. These fuels can release fine particles and other pollutants, especially in kitchens with poor airflow.

The Clean Cooking Alliance’s Nigeria dashboard uses official sources like the World Bank. It estimates that over 167 million people, or 73.8%, in Nigeria did not have access to clean cooking in 2023.

That gap is wider outside cities. The same dashboard reports that 26.2% of Nigeria’s population had access to clean fuels and technologies for cooking in 2023. It also reports 48.7% access in urban areas versus 9.7% in rural areas in 2023.

Cooking Smoke as a Public Health Crisis

Global health agencies link household smoke from cooking to major health harms. The World Health Organization (WHO) estimates that household air pollution led to around 2.9 million deaths in 2021. This includes more than 309,000 children under age 5.

WHO also estimates that household air pollution caused about 95 million DALYs in 2021. This measure combines years lost to early death and disability. The organization notes that the health burden is tied to diseases such as heart disease, stroke, and lung disease.

Moreover, a WHO technical page shows how household air pollution causes deaths. Here’s the breakdown:

- Ischaemic heart disease: 32%

- Stroke: 23%

- Lower respiratory infections: 21%

- COPD: 19%

- Lung cancer: 6%

Global energy data also shows the scale of the challenge. The International Energy Agency (IEA) estimates 2.3 billion people worldwide still cook using open fires or basic stoves that create harmful smoke.

In Nigeria, a large stove program could affect health most in communities that rely heavily on fuelwood or charcoal. It could also change how much time families spend collecting fuel. It could lower daily smoke exposure for cooks and nearby children when stoves are used correctly and consistently.

From Kitchen Emissions to Carbon Markets

The project narrative links emissions cuts from cleaner cooking to carbon markets. Carbon crediting usually relies on measuring and verifying how much a project cuts greenhouse gas emissions compared to a baseline.

International rules also matter if the project aims to generate credits for compliance uses under the Paris Agreement. Under Article 6, countries can cooperate to meet climate targets, including through carbon credits created from verified emission reductions.

Within Article 6, the Article 6.4 mechanism (also called the Paris Agreement Crediting Mechanism) has a UN-backed governance structure. UNFCCC explains that an Article 6.4 Supervisory Body develops and supervises requirements to run the mechanism. This includes approving methodologies, registering activities, accrediting verification bodies, and managing a registry.

This matters because cookstove projects often face scrutiny over real-world use. Carbon credit quality can depend on factors like whether households actually use the new stove, how long they keep using it, and whether old stoves stay in use at the same time. Credible monitoring and verification are central to project integrity under any crediting pathway.

The IEA predicts that clean cooking access will hit around 85% by 2030. This means over 350 million people, mainly in sub-Saharan Africa, will still lack safe cooking options. They will continue to rely on polluting open fires and basic stoves.

To achieve universal access by 2030, there’s a need to connect 160 million people each year. However, funding shortages and infrastructure issues make this unlikely. That requires about $2 billion a year just for Africa to make it happen.

The IEA believes full access by 2040 is more realistic. This will come from increased use of LPG, which will cover about 60% of new connections. It will also involve electric cooking, advanced biomass stoves, and various financing options such as carbon credits. And Nigeria is heading in that direction.

What a $5 Billion Carbon Claim Would Require

Nigeria already has experience with cookstove carbon projects on a smaller scale. The Clean Cooking Alliance’s Nigeria dashboard says the country has 18 registered cookstove projects that have generated 3.4 million carbon credits to date.

The credits from 9 developers are verified by Verra’s VCS and Gold Standard, as seen:

The proposed 80 million-stove rollout is far larger than typical programs. Supporters argue that scale could also mean large volumes of credited emission reductions, especially if adoption remains high over many years.

The $5 billion per year figure has drawn attention because it implies both a large credit volume and a strong credit price. The figure cited in Nigerian reporting was presented as a projection tied to “verified” carbon credit revenues once the project is fully deployed.

Still, projected revenue is not the same as guaranteed income. Real outcomes depend on several conditions, including:

- The number of stoves actually delivered and used,

- The verified emissions reductions per household,

- Approval under the chosen crediting pathway,

- Market demand, and

- The price and transaction costs for credits.

Lagos State’s official post highlights a key milestone: 6 million stoves in Lagos. However, it does not confirm future credit volumes or prices.

Delivery, Use, and Verification Will Decide the Outcome

Several signals will help observers judge the program’s progress and credibility.

First is delivery at scale. A plan for 80 million stoves requires large manufacturing or import capacity, distribution logistics, and after-sales support. Maintenance matters because stoves can fail or be abandoned if they do not meet cooking needs.

Second is sustained use. Clean cooking benefits and emissions cuts depend on households consistently using the new stove. Programs often track usage through surveys, sensors, or fuel consumption checks. Strong monitoring also supports more credible carbon claims.

Third is alignment with recognized rules. If the project aims to issue credits under Paris Agreement pathways, it must follow the requirements of Article 6.4 Supervisory Body. This includes using accepted methodologies and verification practices.

Finally, there is the public data baseline. Nigeria’s clean cooking access is still low overall. The Clean Cooking Alliance dashboard, using World Bank data, reported 26.2% access in 2023, with much lower access in rural areas. A well-run program could shift those numbers over time, but it will require steady funding and coordination across states.

For now, the story combines a large public health goal with a climate finance goal, and the scale is ambitious. The key question is whether implementation, monitoring, and market demand can match the size of the revenue promise.

The post Nigeria Aims for 80 Million Clean Cookstoves and a $5 Billion Carbon Credit Revenue appeared first on Carbon Credits.

Carbon Footprint

CATL & CHANGAN Make History with World’s First Mass-Production Sodium-Ion Passenger EV

China’s CHANGAN Automobile and battery giant CATL have unveiled the world’s first mass-production passenger vehicle powered by sodium-ion batteries. The launch event took place in Yakeshi, Inner Mongolia, and the vehicle is scheduled to reach the market by mid-2026.

The press release explains that this milestone marks a shift from laboratory research and pilot projects to real-world consumer electric vehicles. It also signals the start of a dual-chemistry battery era, where sodium-ion and lithium-ion technologies work together to meet diverse electric mobility needs.

Why Sodium-Ion Batteries Are Gaining Momentum

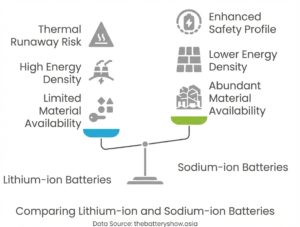

Lithium-ion batteries have dominated electric vehicles for more than a decade. However, concerns over lithium supply, cost volatility, and environmental impacts have pushed researchers to explore alternatives. Sodium-ion batteries emerged as one of the most promising contenders.

Sodium is abundant, widely distributed, and inexpensive. Unlike lithium, it can be extracted from seawater and common salt deposits, reducing geopolitical risks and environmental strain. This makes sodium-ion batteries attractive for countries seeking greater energy independence.

Cold-weather performance is another major advantage. Lithium-ion batteries lose significant capacity in freezing temperatures, which limits EV adoption in colder regions. Sodium-ion batteries, by contrast, maintain strong performance even in extreme cold, opening new markets for electric mobility.

Lithium-ion batteries vs Sodium-ion batteries

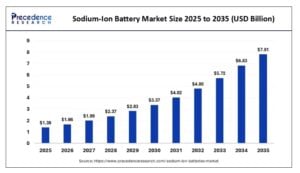

- According to Precedence Research, the global sodium-ion battery market could grow from $1.39 billion in 2025 to $6.83 billion by 2034.

Analysts see 2026 as a turning point, when sodium-ion technology begins large-scale commercialization in vehicles and energy storage.

CATL’s Naxtra Sets New Benchmarks for Sodium-Ion Performance

CATL began sodium-ion research in 2016 and invested nearly RMB 10 billion in the program. The company developed close to 300,000 test cells and assembled a dedicated team of more than 300 R&D engineers, including 20 PhDs.

Research focused on fast-ion transport pathways, composite low-temperature electrolytes, and high-safety electrolyte systems. CATL also leveraged its vast battery management data from millions of deployed units to improve range accuracy and reliability.

This long-term investment highlights how major battery breakthroughs require years of sustained research, testing, and industrial scaling.

Under the partnership, CATL will supply its Naxtra sodium-ion batteries across CHANGAN’s full brand lineup, including AVATR, Deepal, Qiyuan, and UNI. The collaboration positions both companies as early leaders in what could become one of the most disruptive battery technologies of the decade.

Urban and Suburban EVs Made Practical

CATL’s Naxtra sodium-ion battery achieves an energy density of up to 175 Wh/kg, which currently sets a benchmark for mass-produced sodium-ion cells. While this is still lower than leading lithium-ion batteries, it is high enough to support practical passenger vehicles.

Combined with CATL’s Cell-to-Pack (CTP) architecture and intelligent battery management system, the technology enables a pure-electric range exceeding 400 kilometers. As the supply chain matures and chemistry improves, CATL expects future sodium-ion EVs to reach 500–600 kilometers per charge. Range-extended and hybrid configurations could achieve 300–400 kilometers on electric power alone.

These figures cover more than half of the typical daily driving needs in the global new energy vehicle market. For many urban and suburban drivers, sodium-ion vehicles could provide sufficient range at a lower cost.

Cold-Climate Performance Could Transform EV Adoption

One of the biggest barriers to EV adoption is winter performance. Lithium-ion batteries often lose capacity and charging speed in cold conditions, which reduces driving range and convenience.

CATL claims:

- Its sodium-ion battery delivers nearly three times the discharge power of comparable LFP batteries at –30°C.

- Capacity retention remains above 90% at –40°C, and the system continues to provide stable power at –50°C.

This performance could make sodium-ion batteries particularly attractive in regions such as Northern Europe, Canada, Russia, and northern Japan. In these markets, winter range anxiety has slowed EV adoption despite strong policy support.

If sodium-ion batteries deliver on these claims, they could unlock electric mobility in some of the world’s most challenging climates.

Safety Advantages Strengthen Consumer Confidence

Battery safety remains a top concern for automakers and consumers. CATL subjected its Naxtra cells to extreme tests, including crushing, drilling, and sawing. The batteries reportedly showed no smoke, fire, or explosion and continued delivering power even after physical damage.

These results suggest sodium-ion batteries could offer inherent safety advantages over some lithium-ion chemistries. Reduced thermal runaway risk could lower insurance costs, simplify thermal management systems, and improve consumer confidence.

Safety improvements are also critical for regulatory approval and large-scale adoption, especially in densely populated cities.

A Dual-Chemistry Future for Electric Mobility

Both companies emphasized that sodium-ion batteries will not replace lithium-ion batteries. Instead, both chemistries will coexist and complement each other.

Lithium-ion batteries will remain dominant in high-energy applications such as long-range EVs, aviation, and premium vehicles. Sodium-ion batteries are likely to excel in cost-sensitive segments, cold-climate markets, entry-level EVs, and stationary energy storage.

This dual-chemistry ecosystem could accelerate electrification by offering tailored solutions for different use cases. It also diversifies supply chains and reduces reliance on critical minerals.

Choco-Swap Network Could Supercharge Sodium-Ion EV Growth

To support sodium-ion adoption, CATL plans to deploy more than 3,000 Choco-Swap battery swap stations across 140 Chinese cities by 2026. Over 600 of these stations will be located in colder northern regions.

Battery swapping could reduce charging times from hours to minutes, improving convenience for drivers and commercial fleets. It also allows centralized battery management, which can extend battery life and optimize grid integration.

If successful, this infrastructure could give China a major advantage in next-generation EV ecosystems.

Market Outlook: Rapid Growth Across Multiple Sectors

Gao Huan, CTO of CATL’s China E-car Business

“The arrival of sodium-ion technology marks the beginning of a dual-chemistry era.

CHANGAN’s vision shows both its responsibility for energy security and its strategic

foresight. Much as it embraced electric vehicles years ago, CHANGAN is once again

taking the lead with its sodium-ion roadmap. At CATL, we value the opportunity to

work alongside such an industry leader and fully support its strategy, combining our

expertise to bring safe, reliable, and high-performance sodium-ion technology to

market.”

According to data released by SPIR:

- Global sodium-ion battery shipments reached 9 GWh in 2025, representing a 150% year-on-year increase.

- Analysts expect strong growth in energy storage, light-duty vehicles, and passenger EVs starting in 2026.

- By 2030, sodium-ion batteries could reach 580 GWh in energy storage and over 410 GWh in automotive applications. This would be enough to support around 10 million new energy users.

Energy storage is expected to be the largest early market, followed by entry-level EVs and commercial vehicles. Passenger cars are now entering the commercialization phase, signaling broader industry confidence.

Supply Chain Security and Geopolitical Implications

One of the most strategic benefits of sodium-ion batteries is supply chain resilience. Sodium is around 1,000 times more abundant in the Earth’s crust and roughly 60,000 times more abundant in oceans than lithium.

This abundance reduces the risk of supply shortages, price spikes, and geopolitical conflicts associated with lithium, cobalt, and nickel. Countries without lithium resources could still build domestic battery industries using sodium.

For governments, sodium-ion technology offers a pathway to greater energy independence and localized manufacturing.

Environmental and Lifecycle Benefits

Sodium-ion batteries also offer environmental advantages across their lifecycle. Sodium extraction is less water-intensive than lithium brine mining, which has raised concerns in South America’s lithium triangle. Production often uses less hazardous materials, such as iron and carbon-based cathodes.

Research suggests sodium-ion battery production could reduce carbon emissions by up to 60% per kWh compared with some lithium-ion chemistries. Recycling processes may also be simpler and more energy-efficient.

However, sodium-ion batteries currently require more material per kWh due to lower energy density, which could offset some emissions benefits. Continued improvements in chemistry and manufacturing are expected to close this gap.

China’s Strategic First-Mover Advantage

China is taking a lead in next-generation battery technologies by moving sodium-ion batteries from lab research to large-scale commercialization.

Mordor Intelligence report shows that lithium-ion dominated with a 75.5% share in 2025, while sodium-ion is expected to register the fastest CAGR of 18% between 2026 and 2031. Through advanced R&D, robust manufacturing, and supporting infrastructure, Chinese companies are turning experimental technology into market-ready solutions.

The CHANGAN–CATL partnership illustrates this shift. Their sodium-ion passenger car, launching in 2026, marks one of the first instances of mass-produced vehicles powered by this chemistry. The technology promises lower costs, enhanced safety, strong cold-weather performance, and more secure supply chains, making it a practical complement to lithium-ion batteries.

As the dual-chemistry era unfolds, sodium-ion batteries are set to expand the possibilities for electric mobility and energy storage. By combining affordability, reliability, and environmental advantages, they could play a central role in the global transition to clean energy and reshape the future of electric vehicles.

- MUST READ: China Adds Power 8x More Than the US in 2025, with $500B Energy Build-Out in a Single Year

The post CATL & CHANGAN Make History with World’s First Mass-Production Sodium-Ion Passenger EV appeared first on Carbon Credits.

Carbon Footprint

ICVCM Adds New CCP-Approved Carbon Credit Methods for Isometric, Gold Standard and ACR

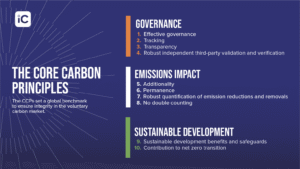

The Integrity Council for the Voluntary Carbon Market (ICVCM) published new decisions under its Core Carbon Principles (CCP) program. The update covers three carbon credit methodologies, also called “categories” in ICVCM’s system. One methodology received full approval, and two received conditional approval.

ICVCM’s CCP label is meant to help buyers spot carbon credits that meet a clear, minimum integrity bar. ICVCM uses an Assessment Framework to apply its label. This framework checks how programs and methods handle key issues, including quantification, additionality, monitoring, and verification.

According to Annette L. Nazareth, Chair of the Governing Board, ICVCM

“Demand for CCP-labelled credits has grown steadily, commanding price premiums that reflect buyers’ renewed trust. Policymakers, multilateral institutions, and standard-setters have incorporated the CCPs into their own frameworks, recognising the Integrity Council’s role in building coherence across voluntary and compliance markets.”

The three decisions were:

- Isometric: ISM Reforestation Protocol v1.1 — CCP Approved

- Gold Standard: Methane emission reduction by adjusted water management practice in rice cultivation v1.0 — CCP Approved (Conditional)

- American Carbon Registry (ACR): Improved Forest Management (IFM) on Non-Federal US Forestlands v2.0 — CCP Approved (Conditional)

How the CCP Label Works and When Conditions Apply

A CCP-approved method can earn credits for the CCP label. Projects need to follow the method and the program’s usual rules. In this ICVCM update, the Isometric reforestation method was approved without conditions. This means credits issued under it can get CCP labeling immediately.

A CCP-approved but conditional methodology can still earn the label, but only if specific conditions are met. These conditions can apply to how projects prove additionality. They can also apply to how projects account for risks. Finally, they may apply to how projects set baselines and leakage deductions.

ICVCM also published a market-level snapshot with its February 2026 decisions. It approved eight carbon-crediting programs as CCP-Eligible. It also approved 38 methodologies.

However, 22 methodologies did not meet the requirements. About 105 million credits were approved for the CCP label. Of these, 52 million are available, while 53 million have been retired or canceled. Globally, here’s ICVCM’s carbon credit achievement:

Isometric Sets a First for Nature-Based CCP Credits

ICVCM granted full CCP approval to Isometric’s ISM Reforestation Protocol v1.1, which Isometric published in October 2025. The protocol outlines rules for measuring carbon removals from reforestation. This refers to restoring forest cover on land that was once forested. ICVCM placed it under the broader Afforestation, Reforestation, and Revegetation (ARR) category.

ICVCM said the assessment found the protocol met all relevant criteria in the CCP Assessment Framework. Because the body approved it with no conditions, it stated that all credits issued under the methodology will be eligible for CCP labels.

The Integrity Council also shared early activity indicators for this protocol. It said no credits had been issued yet, but 20 project developers were already registered under the methodology. The organization added that Isometric expects to issue over 4 million credits annually by 2030 under this protocol.

Isometric announced this week that the approval makes its Reforestation Protocol the first nature-based protocol with the CCP label.

- RELATED: Verra Issues First CCP-Labeled IFM Credits Under VM0045: A New Era for Forest Carbon Accounting

Rice Methane Credits Get a Conditional Green Light

ICVCM gave conditional CCP approval to Gold Standard’s method for cutting methane emissions. This method focuses on adjusting water management in rice cultivation (version 1.0). The Integrity Council announced that it published the methodology in July 2023. It is the first approved method for avoiding methane in rice cultivation.

The basic idea behind adjusted water management is simple. Flooded rice fields can produce methane because organic matter breaks down without oxygen. Changing water levels during the growing season can reduce methane formation.

Gold Standard’s documentation states that methane forms in flooded fields with low oxygen. It also notes that the methodology helps water regime changes that reduce methane emissions.

ICVCM also pointed to recent research on the scale of rice methane. A Nature Research Highlight from May 2025 said that a new inventory found rice paddy methane emissions were over 39 million metric tonnes in 2022.

Why Some Credits Qualify, and Others Don’t

The Integrity Council said the rice methodology qualifies for CCP approval only when specific conditions are met. The conditions show how a project proves additionality in some cases. They also explain a rule update about soil organic carbon loss risk in the methodology.

ICVCM also gave credit volume and pipeline estimates. It said about 50,000 credits had been issued under this methodology so far. However, the body understood that none of those credits complied with the first condition. As a result, the organization said those already-issued credits will not be eligible for the CCP label.

ICVCM noted that Gold Standard plans to issue up to 3.2 million credits in the next five years. This is based on its current project pipeline projections. It also listed the main project locations as India, plus activities in Pakistan, Vietnam, Bangladesh, Cambodia, Ghana, Indonesia, Lao PDR, Nepal, and Thailand.

- SEE MORE: Shell’s Initiative to Cut Methane in Rice Farming in the Philippines and Create Carbon Credits

ACR’s Forest Credits Face Tighter Baseline Tests

Same with Gold Standard, ICVCM also granted conditional CCP approval to ACR’s Improved Forest Management (IFM) on Non-Federal US Forestlands v2.0. IFM projects aim to change forest management practices to increase stored carbon or avoid emissions compared with a baseline scenario.

ICVCM explained that v2.0 is an earlier version of an IFM methodology that its Governing Board had already approved in August 2025 (v2.1). For v2.1, ICVCM had set a condition tied to leakage.

- A leakage deduction is needed for projects that cut wood product output by less than 5%. This keeps treatment consistent with projects that exceed that threshold.

For v2.0, ICVCM set two additional conditions. The methodology can earn CCP labeling if:

- A dynamic evaluation of the baseline is verified in line with ACR’s tool for dynamic baseline evaluation (developed with v2.1), and/or

- Removal credits are generated using a specified equation in the methodology (ICVCM references Equation 30).

ICVCM also quantified the immediate impact. It said 2.7 million credits were expected to be immediately eligible for the CCP label out of 13.3 million issued credits under this methodology.

The Integrity Council also stated that past and future removal credits from this method can get CCP labels. Future emission reduction credits can qualify, too, if they use the dynamic baseline evaluation tool.

ACR said the CCP label will soon activate for 2.7 million eligible IFM 2.0 credits in the ACR registry. They linked eligibility to the same baseline evaluation tool.

What CCP Expansion Means for Buyers and Developers

These ICVCM decisions matter because they expand the set of methodologies that can produce credits with the CCP label. For buyers, the label can act as a quick screen when building procurement rules. CCP decisions can influence method evolution for project developers and standards bodies. Conditional approvals often need updates to methods or stricter project tests.

At the same time, the details show that CCP labeling is not automatic. For example, ICVCM’s conditions for the rice methodology mean that some already-issued credits will not qualify. In the IFM case, ICVCM tied eligibility to specific approaches for baselines and the type of credit (removals versus emission reductions).

The approvals expand high-integrity CCP-labeled credits. They also signal growing supply for buyers while enforcing strict standards on baselines, additionality, and verification—shaping voluntary carbon markets toward greater quality and scale.

The post ICVCM Adds New CCP-Approved Carbon Credit Methods for Isometric, Gold Standard and ACR appeared first on Carbon Credits.

Japan’s largest polluters are rushing to buy carbon credits ahead of the launch of the country’s mandatory emissions trading system. Trading activity on the Tokyo Stock Exchange (TSE) has surged as companies prepare for tighter climate rules and try to meet their corporate sustainability targets before the fiscal year ends.

According to Bloomberg, major Japanese companies are already purchasing credits on the TSE’s voluntary market in anticipation of the GX-ETS launch.

This buying spree highlights growing anxiety about future compliance costs. At the same time, it signals that Japan’s carbon market is shifting from a voluntary experiment to a central pillar of its climate strategy.

What Is the GX-ETS and Why Does It Matter

The Green Transformation Emissions Trading System (GX-ETS) is Japan’s national carbon trading program. The government launched it in 2023 under the GX League, a public-private platform designed to accelerate corporate decarbonization.

The GX-ETS mirrors the European Union’s emissions trading system. Companies receive or buy emissions allowances and can trade them. If they emit less than their cap, they can sell extra allowances. If they exceed limits, they must buy more or face penalties.

Timeline and Key Features

Japan is rolling out the GX-ETS in stages:

- Phase 1 (2023–2025): Voluntary participation and market testing

- Phase 2 (2026 onward): Mandatory participation for large emitters

- Future phases: Auctions, price bands, and fuel levies

Japan plans to introduce power sector auctions around 2033 and a fossil fuel importer levy by 2028. Policymakers are also considering price bands of ¥4,000 to ¥6,000 per tonne by 2027, with potential increases by 2030. Significantly, the compliance market will include a price ceiling and phased expansion with additional policy tools.

The system integrates voluntary credits into compliance trading. Companies can trade GX credits via call auctions on the TSE, with unmatched orders carried forward. This design aims to improve liquidity and price discovery.

Japan’s Path to Net-Zero by 2050

Japan made modest progress in reducing emissions in the first half of 2025. The Ministry of the Environment reported a 2.8% decline compared with the same period in 2024. For the full year, emissions are estimated at 1,070 million tonnes of CO₂ equivalent, down from about 1,272 million tonnes in 1990.

Much of this improvement came from energy efficiency gains in the industrial sector. However, Japan still relies heavily on fossil fuels, and transport emissions remain difficult to reduce. Consequently, current policies are projected to cut emissions by 31% to 37% below 2013 levels by 2030, which still falls short of the country’s 46% national climate target, excluding land-use emissions.

Heavy industries—such as steel, chemicals, cement, and power generation—account for more than 60% of national emissions, making them key GX-ETS targets. Therefore, the GX-ETS is expected to cover roughly 60% of Japan’s greenhouse gas emissions and support the country’s goal of achieving net zero by 2050.

Japan’s carbon tax remains low at about ¥289 per tonne (roughly $2.16), emphasizing the need for stronger market-based mechanisms. As a result, policymakers view the GX-ETS as a critical lever to accelerate emissions reductions and drive the nation toward net-zero.

Who Must Participate in the GX-ETS

Phase 1 of the GX-ETS was voluntary. However, Phase 2 will become mandatory in spring 2026. Companies emitting more than 100,000 tonnes of CO₂ per year must participate.

This rule affects roughly 300 to 400 companies. Together, they account for about 60% of Japan’s total emissions. Key sectors include steel, chemicals, cement, power generation, automotive manufacturing, and aviation.

Under current proposals, companies can use carbon credits to offset up to 10% of regulated emissions. Therefore, credits complement emissions cuts rather than replace them.

Pre-Compliance Buying Surge Among Big Polluters

Large Japanese companies are buying voluntary credits aggressively before the mandatory launch. TSE officials see strong demand driven by companies preparing for GX-ETS and rushing to retire credits before the fiscal year ends.

Reports also reveal that members of the GX League, such as Toshiba, Tokyo Gas, and Isuzu Motors, have already participated in voluntary trading. Analysts expect steelmakers, utilities, and other heavy industries to dominate future purchases.

This early buying strategy helps companies hedge against future allowance shortages. It also reduces the risk of penalties once compliance rules take effect.

Japan’s Carbon Credits: Demand Soars Ahead of Mandatory GX-ETS

Japan’s carbon credit market is expanding fast. It was valued at about $28.2 billion in fiscal 2023 and could reach more than $121 billion by 2031, growing at roughly 20% annually.

Trading on the TSE began in 2023 and focuses on GX credits, including:

- J-Credits from domestic renewable and efficiency projects

- JCM credits from international projects under Japan’s Joint Crediting Mechanism

However, demand already exceeds supply. J-Credit issuance averages around 1 million tonnes per year. Analysts expect demand to reach about 3 million tonnes annually once the mandatory phase begins.

Therefore, limited supply could push prices higher and increase compliance costs for heavy emitters.

Carbon Credit Prices and Market Dynamics

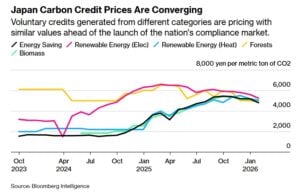

Bloomberg also highlighted that carbon credit prices on the TSE have fluctuated as the market matures. Renewable electricity credits peaked at about ¥6,600 per tonne in early 2025. Since then, prices have fallen by nearly 25%.

The Ministry of Economy, Trade and Industry has proposed a price ceiling of ¥4,300 per tonne for the compliance market. Renewable-linked credits still trade above that level, reflecting strong demand and limited supply. And the prices across voluntary credit categories are converging ahead of the mandatory phase. This trend suggests growing liquidity and market confidence.

Challenges Facing the GX-ETS

Despite strong momentum, several challenges remain. Limited credit supply could push prices higher if demand grows faster than new issuances. Credit quality also poses a risk, as regulators must ensure offsets deliver real and permanent emissions reductions to avoid greenwashing.

At the same time, Japan still depends heavily on coal, gas, and oil, meaning carbon trading alone cannot transform the energy system. Transport emissions also remain a major hurdle, especially in the road and aviation sectors, where decarbonization is progressing slowly.

Past regional trading systems, such as Tokyo’s cap-and-trade program, achieved emissions reductions of around 15% to 27%. However, scaling that success nationwide will require strict enforcement, transparent monitoring, and strong policy support.

Strategic Role of Carbon Credits in Japan’s Transition

For hard-to-abate sectors such as steel and power, carbon credits provide a temporary bridge while low-carbon technologies mature. Companies can offset a small share of emissions while investing in hydrogen, electrification, and carbon capture.

Early purchases also hedge against future price spikes. If allowance supply tightens, companies holding credits will face lower compliance costs.

Globally, Japan wants J-Credits to align with international carbon markets and potential EU carbon border rules. This strategy could strengthen Japan’s role in Article 6 carbon trading frameworks.

In conclusion, the surge in carbon credit buying shows Japanese companies are taking the GX-ETS seriously. The market is transitioning from a voluntary pilot to a compliance-driven system that will shape corporate strategies for decades.

As climate pressures mount, Japan must close the gap between current policies and its 2030 target. The GX-ETS could become one of the country’s most powerful tools to drive emissions cuts, attract investment, and accelerate clean energy deployment.

However, success depends on credit supply, price stability, and strong governance. Industry analysts and experts suggest early credit buying reflects corporate hedging strategies as Japan’s carbon market moves toward full compliance.

If Japan manages these challenges, the GX-ETS could transform its carbon market and set a model for other Asian economies.

The post Japan’s GX-ETS Sparks Carbon Credit Surge as Major Polluters Prep for Compliance appeared first on Carbon Credits.

Gas is Just Another Dirty Fossil Fuel

Choosing the Right Home Is Tough. Climate Change Is Making It Harder.

Murders Committed by ICE Are OK, According to What We See Here

Guest post: Why China is still building new coal – and when it might stop

Guest post: Why China is still building new coal – and when it might stop

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Greenhouse Gases6 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Climate Change6 months ago

Guest post: Why China is still building new coal – and when it might stop

-

Climate Change2 years ago

Bill Discounting Climate Change in Florida’s Energy Policy Awaits DeSantis’ Approval

-

Greenhouse Gases2 years ago

Greenhouse Gases2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change2 years ago

Spanish-language misinformation on renewable energy spreads online, report shows

-

Climate Change2 years ago

Climate Change2 years ago嘉宾来稿:满足中国增长的用电需求 光伏加储能“比新建煤电更实惠”

-

Climate Change Videos2 years ago

The toxic gas flares fuelling Nigeria’s climate change – BBC News

-

Renewable Energy2 years ago

GAF Energy Completes Construction of Second Manufacturing Facility